The long period of soft market conditions, characterised by an excess of (re)insurance capital and an emphasis on meeting premium income targets, has finally come to an end. Instead, faced with deteriorating loss ratios and increasing costs, the Renewable Energy insurance market seems to have come to a tipping point as truly hard market conditions have emerged during the course of the last year.

This means that state of the art analytics more than ever needs to play a centric role to underpin proactive, strategic and optimized risk management/financing, such as the use non-recourse debt financing and, in this context, the position of raising and securing senior debt to finance the generation asset.

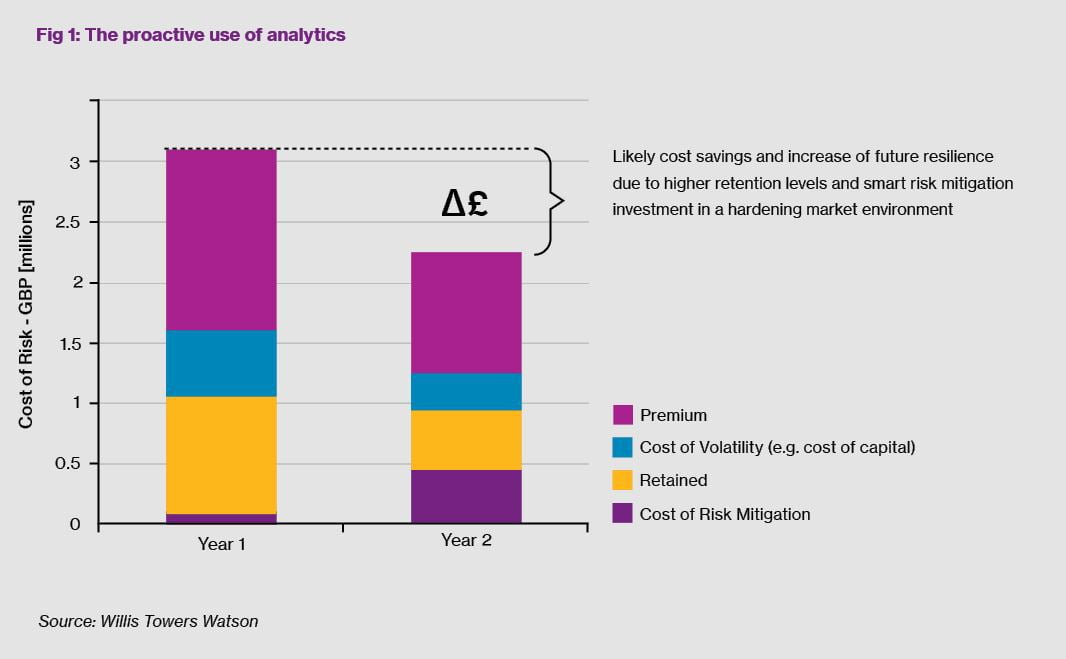

We already are seeing risk managers using state of the art analytics and engineering to position their respective organisations strongly in their conversations with the insurance markets. Others, who have not yet taken this step, may already have found themselves in a position where the markets have dictated the pricing, resulting in significant premium increases. This means that in order to achieve a future resilient risk management strategy and successful renewal, it should be now more than ever prerequisite to have an analytically empowered view of the organisation’s risk profile; “what doesn’t get measured, doesn’t get done”. Figure 1 on the next page illustrates how risk managers are proactively using analytics to evaluate the total cost of their risk financing strategy by analytically optimizing risk transfer (insurance versus higher retention levels) as well as the measurement of return on investment for physical risk mitigation as an alternative to risk transfer in a hardening market environment.

Let’s take a closer look on how the above figure could be realised using a plausible case study by drawing from experiences and key lessons learnt in working closely with corporate risk managers.

However, on the plus side:

Based on this understanding, the risk manager decides to engage the broker for a deeper analytical dive and assessment to consider if an adjustment to the risk management strategy response to the hardening market environment is required and can be accommodated within internal budget constraints.

The risk manager is also aware that focus of this assessment needs to be on higher retention levels and a cost benefit assessment of physical mitigation in the retained portion of the risk management strategy in order to achieve cost savings. The assessment therefore focusses initially on the risk tolerance for key performance indicators on the renewable’s company’s balance sheet.

The risk manager, with the help of the broker’s analytical team, now firstly engages with the CFO of the organisation and demonstrates, with a similar figure to the one outlined in Figure 1 above, the potential cost savings that could be made over the coming years by retaining more risk as well as investment into targeted risk mitigation measures. Based on this successful discussion, the green light has been given by the CFO to engage with the markets in changing the current risk management and financing strategy, as well as exploring retention vehicles such as captives going forward.

Despite challenges from the markets in the follow-on renewal discussions, which are also heavily influenced by the recent claim, the broker supporting this risk manager is able to demonstrate, with this proactive analytical approach, that the claim related to a 1 in 20 type event. The broker is therefore able to secure an insurance premium that is still within the modelled ‘technical premium range’ for the new risk financing strategy of this company by including higher retention levels. The risk manager should think that this is good value for money in a hardening insurance market environment. The insurance manager has been also given a mandate by the CFO to use some of the capital that will be freed up by the higher retention levels into retrofitting the design of key exposed assets against flood and earthquake risks, thereby also demonstrating proactive risk control to both the CFO and the insurance markets. The risk manager has since been in communication with the organisation’s sustainability function, who is trying to identify the impact of climate change to their organisation and has rightly made the connection that the assessment of physical catastrophe and climate risk exposures could be beneficial a first stepping stone for a climate change impact assessment and has managed to play a strategic role in this topic too.

Having analyse this case study, what can we conclude are the top five benefits of using analytics from a risk management perspective?

This case study has highlighted that proactive risk management, utilizing analytics and risk engineering, can position an organisation robustly in a hardening market situation. Difficult choices on risk retention can be underpinned and justified by analytics to internal senior stakeholders; ultimately, this can result into more proactive risk control and cost savings, despite the impact of a hardening insurance market.

The next steps for any risk manager reading this article to should therefore be to:

Torolf Hamm is Head of Natural Catastrophe and Climate Risk Management, Willis Towers Watson. Torolf.Hamm@WillisTowersWatson.com