The market for Floating Offshore Wind (FOW) is beginning to gather momentum following a cautious beginning. Between 2008 and 2018, global installed capacity increased from near zero to 57 MW. Forecasts suggest that growth during the next ten years will be exponential in comparison, with industry experts estimating that installed capacity could increase to anywhere between 5 and 30 GW by 20301. Of the 57 MW installed, 30 MW is accounted for by Equinor’s five-turbine Hywind Scotland farm. It is currently the only floating farm of any significant scale but has provided optimism for the future of floating platforms, having operated at 65% of its maximum theoretical capacity since its commissioning in 20172.

The commitment to the development of this market can be seen through the prism of government targets and investment:

The primary advantage of FOW projects is the fact that the technology allows farms to be located in deeper water sites than is currently economically viable with fixed platforms. At present, it is generally accepted that fixed-bottom foundations are not appropriate past 60m in depth, whereas these deeper site locations offer stronger, more stable wind speeds, which can help to reduce the overall cost of energy for offshore wind. Furthermore, it may become a necessity for farms to be moved further offshore, as the availability of suitable near-shore sites decreases following a surge in developer demand. Secondly, installation costs may be reduced due to a greater proportion of the assembly taking place onshore. With floating platforms, turbines can be mounted onto their foundations and floated to the site of the farm, provided that there is a port with suitable facilities in close enough proximity to the site. As a result, costs can be dramatically reduced as there is no need for specialised assembly vessels.

The issue of poor offshore weather conditions may also be mitigated, which can often limit the window in which developers can install fixed foundations due to the considerable amount of offshore assembly7. The designs also allow for electrical and mooring systems to be unplugged, allowing the structure to be taken back to shore for maintenance or repair works, decreasing both the cost of the repairs; this is not only because there is no need to use specialised vessels, but also because the risk of performing the repairs decreases8. Finally, the fact that the sites can be located in deeper, more remote waters means that the risk of bird strikes, and the subsequent damage caused, may also be reduced9.

The major disadvantage for developers currently is that FOW project costs are higher than the fixed-bottom alternatives, and there are still sites that provide good conditions for wind farms at less than 60m in depth. However, this may only be the case in the short-term as FOW costs fall and shallow-water site availability decreases. Whilst strong and stable winds may be considered an advantage of deep-water sites, this factor also brings with it the risk of harsher wave action and other adverse weather conditions.

Furthermore, greater distances from the shore will inevitably affect the design, construction and installation of the power cables. In addition to the added consideration of distance, complications may also arise with connecting cables to a moving foundation10. Finally, the advantage of onshore assembly can only be realised if a suitable port is in close enough proximity to the site. In reality this may not be likely, due to the width and depth that would be required for the port to facilitate assembly; this will only become more relevant with the continuous growth in turbine size.

Monopile foundations are currently the most common fixed-bottom design, due to its cost-effectiveness and adaptability to a variety of seabed conditions. However, they begin to lose their economic viability past depths of 35m, where jacket foundations adapted from offshore oil and gas rigs are typically preferred. The jacket foundation is considered to be cost-ineffective in depths of over 50m, which is a major limitation on the development of large-scale offshore wind farm, with high potential markets such as Japan and the US having relatively few suitable shallow water sites11.

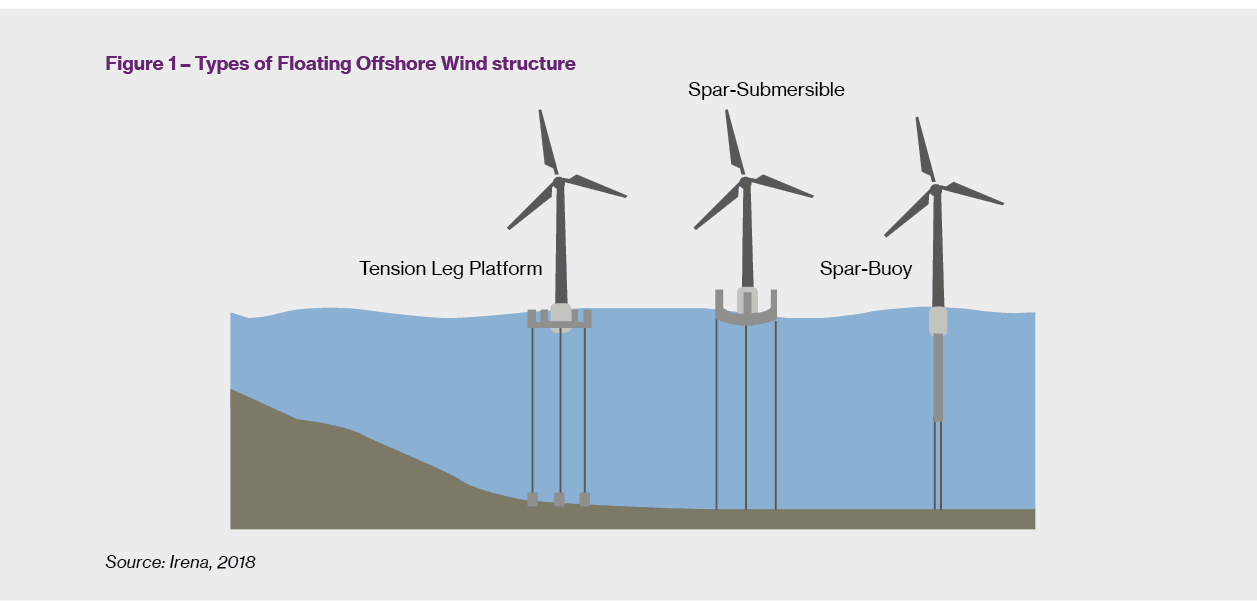

Figure 1 above illustrates the three main design variations for floating platforms:

It can be seen that each design offers its own benefits and costs, and developers are likely to choose designs on a case-by-case basis with factors such as water depth, infrastructure/port availability and the physical characteristics of the site playing a deciding role.

Market share for installed capacity in 2025 is expected to be split into 65%, 24% and 10% for Semi-Submersible, Spar and Tension Leg Platform respectively14, so it is not expected that any single design will become market-standard. As a result, it is paramount that insurers continue to familiarise themselves with the nuances in the technologies, in the same way that the market approaches prototypical onshore turbines. There is also a responsibility on the behalf of the insured to conduct due diligence on which design is the most appropriate for their chosen site, which should be facilitated through risk management services provided by their broker.

Alex Morris is a Graduate Account Executive Renewable Energy GB, Willis Towers Watson in London.

1 GlobalData (2019a), Floating foundations: The future of deeper offshore wind, GlobalData, London. 2 https://www.power-technology.com/comment/floating-offshore-wind-2019/ 3 https://www.power-technology.com/comment/floating-offshore-wind-2019/ 4 https://www.power-technology.com/comment/floating-offshore-wind-2019/ 5 Quest Floating Wind Energy (2019). 2020 Global Floating Wind Energy Market & Forecast [online]. Available at: https://questfwe.com/executive-summary/ [Accessed 30 Dec. 2019] 6 https://www.power-technology.com/comment/floating-offshore-wind-2019/ 7 Hannon, M. et al., (2019) Offshore wind, ready to float? Global and UK trends in the floating offshore wind market. University of Strathclyde, Glasgow, https://doi.org/10.17868/69501 8 Carbon Trust (2015) Floating Offshore Wind: Market and Technology Review. Available at: http://www.carbontrust.com/media/670664/floating-offshore-wind-market-technology-review.pdf.

9 RSPB (2016) Floating offshore wind farm given the green light from RSPB Scotland following consultation response. Available at: https://www.rspb.org.uk/our-work/rspbnews/news/stories/rspb-scotland-supports-offshore-floating-wind-project/ (Accessed: 16 January 2019). 10 Hannon, M. et al., (2019) Offshore wind, ready to float? Global and UK trends in the floating offshore wind market. University of Strathclyde, Glasgow, https://doi.org/10.17868/69501 11 IRENA (2018) Renewable Energy Benefits: Leveraging Local Capacity for Offshore Wind. Abu Dahbi. Available at: www.irena.org. 12 Carbon Trust (2015) Floating Offshore Wind: Market and Technology Review. Available at: http://www.carbontrust.com/media/670664/floating-offshore- wind-market-technology-review.pdf. 13 Hannon, M. et al.,(2019) Offshore wind, ready to float? Global and UK trends in the floating offshore wind market. University of Strathclyde, Glasgow, https://doi.org/10.17868/69501 14 Hannon, M. et al.,(2019) Offshore wind, ready to float? Global and UK trends in the floating offshore wind market. University of Strathclyde, Glasgow, https://doi.org/10.17868/69501