Series (or Serial) Loss Clauses, are often heard mentioned with bated breath in the public houses and barista shops in and around Lime Street and the square mile. London has historically been a technical centre for insurance and engineering classes and the decisions made here frequently reverberate around the world. The recent soft insurance market supported the advent of many bespoke wording forms, within which serial or series loss clauses were tweaked, amended or removed entirely without requisite consideration and so were often widely misunderstood when applied.

Whilst such exclusion clauses are not widely applied in the Oil & Gas, Conventional Power or Property markets, the correct understanding/interpretation of the risks and application of the clauses relative to global deployment of these assets have remained the privileged jurisdiction of a few dedicated individuals in the Renewable Energy insurance market and their claims teams.

In the heady days of cheap and widely available capacity, the Facultative Property market was falling over itself to offer extremely competitive capacity for operational solar and wind projects, often without any due concern or consideration to series loss clauses: surely an operational solar farm is just a static property risk?

The conventional Power market is familiar with the concept of serial losses. However, in delivering many renewable projects to the market under conventional Power wordings, it had failed to recognise any modular technology risk. This has mainly been because of the steadily reducing flow of single site coal and gas projects; as a result, they have been keen to maintain premium income levels and have often fallen foul of influential brokers pleading to treat renewables like any other power generation technology, or at least to support their clients’ diversification into new renewable technologies.

In the soft market, series losses remained a ghostly memory for those with dedicated green capacity, with mandatory application of a Series Loss Clause remaining part of their reinsurance treaty arrangements. Taking into account the history and the lessons learned during the evolution of the renewable energy industry, Series Loss Clauses remained one of the “dark art” secrets or defences of the Renewable Energy market. Whilst treaties often required the application of a Series Exclusion Clause, there remained considerable flexibility as to language, application and interpretation in a market seeking contract certainty.

The modular nature and rapid evolution of technology, particularly in the wind and solar sectors, means that the Renewable Energy market is increasingly exposed to project risks involving nascent or emerging technologies, which through their novelty can make them prone to claims arising out of the defects in design, plan, specification, workmanship or materials. It’s this modular nature, inherent in wind and solar technologies, where multiple claims can arise if identical products contain identical defects that caused a series of Serial Defects Clauses to increasingly become a mandatory requirement in persuading underwriters to deploy their capacity.

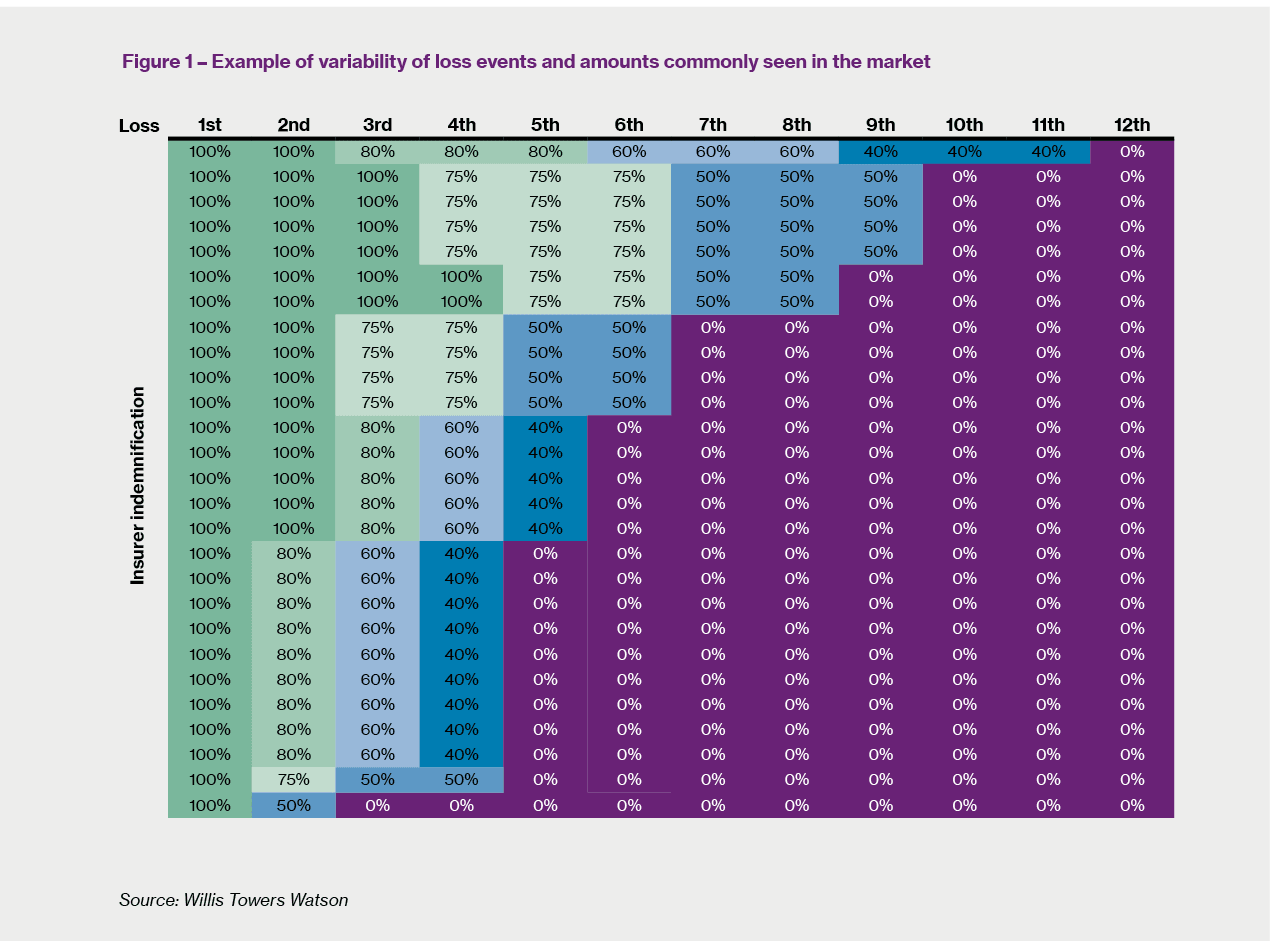

Through the application of this exclusion, the All Risks of sudden or unforeseen Physical Loss or Damage policy is moderated to indemnify only a percentage of a loss, often reducing on a sliding scale for each loss after the first known loss.

It’s common to see a sliding scale as shown in Figure 1 above. After application of the deductible specified in the schedule, the insurer shall indemnify the insured for:

Then the insurer shall not indemnify the insured for the sixth and following cases of loss or damage resulting from causes of the same nature.

This condition is intended to prevent the same design defect from causing multiple claims under the same insurance policy. It is also designed to ensure that this type of claim is being more properly directed to the manufacturer under the original equipment or supplier warranty.

It should also be noted that whilst a traditional Property & Casualty insurance policy is intended to pay only in the event of damage, it is possible that a series loss (or serial event) may be identified prior to actual damage being sustained. In such instances the only recourse available is usually through the supply and installation contracts, potentially underpinned by any original equipment manufacturer or supplier warranties, or professional indemnity insurance.

The general premise is that if the development of or discovery of a defect shall indicate or suggest that similar defects exist elsewhere in the insured property, the contractor shall forthwith investigate and, if necessary, rectify the defects in such insured property at its own expense or alternatively bear all losses arising out of such defects.

As we have seen, following the first loss the above position is moderated by affording a reduced level of insurance cover to the project, if the serial defect has resulted in damage.

Soft market In the soft market, it was common to see sliding scale multipliers being applied for up to 12 or perhaps 15 losses where some insurers had close relationships with the original equipment manufacturers resulting in increased comfort, or oversight of the quality of the manufacturing process.

Hard market However, in the current hardening insurance market where capacity is more restricted, insurers are seeking to “throttle” open ended terms and conditions. The balance of power has swung from a buyer to a sellers’ market; it is now common to see Renewable Energy insurers seeking to push the pendulum further in their favour by restricting the number of serial claims or percentage of loss for which they will be responsible under the insurance policy. Their ultimate aim is to move back to the somewhat utopian position whereby after an identified loss, and 100% indemnity for the first Physical Damage sustained, the contractor should investigate and take the necessary remedial action at its own expense or bear all further losses arising out of such defects.

Underwriting factors How far the pendulum swings - between a single loss and perhaps up to 15 losses - will depend on the specific underwriting/broking dynamics. These are likely to include:

Even traditional Property insurers are responding to clients’ broad and disparate composite asset portfolios by considering the potential risks and challenges inherent with modular engineering risks, as well of course as traditional conventional single site Power underwriters.

Increasing uncertainty? Whilst applying a total or increasing exclusion after the first loss might be insurers’ preferred position, the simple exclusion of defects resulting in serial losses where there is physical loss or damage is in stark contradiction to the accepted market position; if there is physical loss or damage, the policy will respond. It is the comfort placed in the knowledge that an insurer’s primary response in the event of physical loss or damage in which many contractors, sponsors, developers, financiers and their advisors rely on when completing their risk assessment. Relying on insurers’ prima facie duty if there has been physical loss or damage, the insurance policy will respond as primary to reinstate the loss, reducing volatility of unknown risk and increasing bankability.

Where claims settlements for physical loss or damage have been moderated by the application of a Series Loss Clause, there should be an acknowledgment, for owner procured project policies, that if there is a failure of the owner procured insurance to respond, the contractor will contractually retain the risk of further physical loss or damage through to substantial completion, or expiry of the defects liability period, although this may be mitigated by their potential contractual recourse to any manufacturer or supplier warranties.

Whilst the primary risk of not having insurance funds to reinstate such additional modular losses during the construction phase falls on the contractor, whilst this would be outside the assigned securitisation of the regulated insurance package, a more onerous series loss clause may be considered an increased credit risk to some project financiers, relative to the financial stability of the contractor party and manufacturer warranties.

Many insurers’ initial positioning is that the contractor, as the delivering party, is responsible for the manufacture or provision of materials to be free from defects and would be responsible under contract in the absence of damage for such defects. As such, they consider that it is right and proper that manufacturers, suppliers and contractors should not indefinitely devolve their responsibility for the consequences of such defects to insurers when there is indemnifiable loss or damage. With new and developing technology, the market rhetoric is that it should not be used to bankroll risk which would otherwise be considered a commercial research and development risk to the technology provider.

The application of a Serial Loss Exclusion Clause is often open to subtle interpretation. The incident frequency and percentage indemnity can be applied to losses, incidents, claims and other designations which all have their own interpretation.

It is also often unclear to clients (and insurance professionals) as to whether the applications are - or should be - per loss incident, per site or project insured, per umbrella or portfolio insurance policy, or should instead be moderated by wider industry experience, i.e. known market technology issues being called to regulate the response on individual projects which have not previously experienced the technology issue in question.

Concept of knowledge The concept of knowledge is also open to interpretation. If there is a known insured loss, then identical subsequent losses would then be considered known. However, if there was a known manufacturer issue with a component, some clauses will respond to known losses (i.e. where a technical bulletin has been issued by the manufacturer to the insured client). However, if it had not yet been possible to replace the known defect (perhaps delayed so as to be addressed during a planned outage), others will apply a subjective position of known, or should have reasonably known - which implies an element of negligence on behalf of the owner or operator.

It is now more common to see the application of a Series Loss Clause to the modular element over which insurers have concern (i.e. panels or inverters for solar projects or towers, nacelles & blades for wind projects) thereby leaving the other traditional civil and steelwork constructional risks unabated by a Serial Defect Clause. However, following some recent negative experiences with balance of plant contractors where workmanship and defects issues have been discovered in multiple foundations, insurers’ opinions remain divided.

Position under construction contracts When considering serial losses, it’s also necessary to consider the position under the construction contracts which will often contractually determine at which point responsibility is assumed. For a turbine supply and installation contract, this might be when more than 25% of the supplied equipment exhibits identical defects. As such point, the contractor will take responsibility for the financial loss incurred by replacing the faulty or defective equipment at their cost. This percentage is open for commercial discussion and could range between 10% and 40%. As the project moves into full commercial operations and is subject to the operations and maintenance contract, similar provisions, responsibility and recourse may be available under the supplier or manufacturer warranty.

Financial loss following delay When there is contractual acceptance by the contractor or manufacturer for the defect in design, plan, specification, materials or workmanship issue identified, such acceptance is normally limited to the replacement, repair or rectification of the defective physical equipment itself - whether damage has been occasioned or not. However, it will not indemnify the owner or operator for this full financial loss of revenue resulting from the identified loss or damage, or potential future interruption which might be incurred whilst remedial works are performed to the equipment where a serial defect has been identified but damage has not yet been occasioned.

In these circumstances, the insurance policy might be expected to respond for the loss of revenue. The physical loss or damage trigger would have been met to create a valid claim under the insurance policy (i.e. would have responded in any case but for the acceptance of the identified serial defect under the construction contract or warranty). Should the scheduled commercial operations be delayed. It is likely that for a construction policy any available liquidated delay damages would be utilised to partially offset such reduction in lost revenue. Additionally, during commercial operations any financial damages from an availability warranty would be applied for the lost performance.

These serial losses are often the result of defective manufacturing or design flaws that lead to early and repeated failures. For example, in the past few years some Original Equipment Manufacturers (OEMs) have experienced serial failures in blades and drive trains, resulting in hundreds of blade sets needing replacement and remediation required on drive trains. Where these cases are well documented such risks are unlikely to be covered by insurance as they would not be considered fortuitous.

A case study from 2019 Most insurance companies have a serial loss clause in their policy, and one leading insurer (let’s call them Insurer A) is no exception. Insurer A’s Serial Loss Clause covers faulty equipment on a sliding scale, so the first blade or gearbox is covered by 100%, the second by 75% and so on, until no coverage is paid. Insurer A’s view, as stated to us recently, is that any further losses incurred after that point are no longer fortuitous, which goes against the point of insurance; after that point, insists Insurer A, the insurer would be just paying for something that’s defective.

It’s perhaps not so surprising that there can be some very sensitive and high-stakes conversations when things go wrong. In February 2019, a storm passed through southern California and damaged the majority of blades at a 50 MW wind plant owned by an Australian energy company. A disagreement followed between the energy company and the turbine provider over whether the blade cracking was caused by deficient blades (defective equipment) or by the pitch control systems being improperly set by the operator (defective workmanship).

The insurer (Insurer A above) was closely involved because it might have had to pay out on a claim, depending on the results of the negotiations. None of the parties involved would disclose the outcome, but Insurer A suggests that the example highlights the complexities around damage claims. The insurer believes that these conversations can be sensitive, because eventually somebody has to assume responsibility. The loss may be considered a serial loss, but some may disagree – so it is vital, as the insurer who is going to pay for the loss, that the issue is decided once and for all.

Insurance is not the same as an extension of a warranty! A risk for operators of wind farms shopping for insurance is to assume that all their risk will be covered in the policies. One operator suggested to us recently that it was a myth among wind farm managers that, when their warranty runs out, all they need to do is buy property insurance and just give future losses to the insurance company.

Extended warranty coverage from an OEM for a wind turbine varies from US$30,000 to US$100,000 per year, depending on makes, models and other factors and OEMs have been making brisk sales as warranties run out.

Applicable to both physical damage and loss of revenue sections? When considering the above, it is a concern that the insurance market, as it hardens, will move to apply a serial loss clause sliding scale response to all sections as a general condition - not just to the physical damage sections, where loss of revenue would apply in full, until the exhaustion of the number of identifiable physical damage losses. Such a strict application could have the dire effect of applying the sliding scale of indemnity to loss of revenue losses, leaving sponsors and developers short of insurance indemnity from which to service their debt - thereby undermining some of the fundamental principles in non-recourse or project finance insurance.

It’s often overlooked that the Serial Loss Clauses are inextricably linked with the Defects in Design Exclusion Clauses, commonly London Engineering Group (LEG) LEG1, LEG2 and LEG3.

LEG2 If the cover benefits from a LEG2/96 defect in design exclusion, for simplicity in the event the defect was associated with a specific item (e.g. an inverter junction box – the component part), the insurance policy should only respond to indemnify the physical damage losses consequent upon the defect which damaged the inverter box - not the defect and damage to inverter junction box itself . As such, the serial loss clause would only be applied to the indemnifiable consequential physical loss or damage.

However, there may not be a sufficient quantity of similar defects for the contractor or technology provider to contractually accept that a serial defect has occurred. Alternatively, their response may be limited to the sole replacement of their supplied equipment, rather than the consequential physical loss or damage; in which case, the insurance policy may respond for physical damage in addition to loss of revenue without recourse to or acceptance by the technology provider.

LEG3 Let us turn now to a scenario where the cover benefited from a LEG3/96 Defect in Design Exclusion Clause. In the event the defect was associated with a specific item (e.g. the inverter junction box (being the component part) the insurance policy should respond to indemnify the physical damage losses consequent upon the defect which damaged the inverter box, and the defect if resulting in damage to inverter junction box. As such, the serial loss clause should apply to all physical loss or damage, the inverter junction box and consequential physical damage.

Again, there may not be a sufficient quality of similar defects for the contractor or technology provider to contractually accept that a serial defect has occurred. Alternatively, their response may be limited to the sole replacement of their supplied equipment, not the consequential physical damage - in which case the insurance policy may respond for physical damage in addition to loss of revenue. However, if there is a sufficiently high LEG3/96 deductible, say US$100,000 for component parts (particularly for solar projects), this is likely to remove the increased physical damage risk to insurers providing a broader Defects in Design clause, leaving only an increased exposure to loss of revenue.

The insurance sector has been growing more comfortable with renewable technologies and the soft market had removed a degree of focus from series loss incidents.

However, serial losses are often the result of defective manufacturing or design flaws that lead to early and repeated failures. In the past few years, some original equipment manufacturers (OEMs) have experienced serial failures in blades and drive trains on windfarms, resulting in hundreds of blade sets needing replacement and remediation needed on drive trains.

Where these cases are well documented, they are not a risk that can be covered by insurance, not being considered fortuitous. Insurance policies are not a replacement for a warranty and will not protect an owner against recurring or multiple losses.

The positioning of the level of indemnity and amount is subjective, depending on the insurer perception and understanding of fortuity. As the hard market continues, there will be a greater pressure to reduce the number of incidents and loss amounts for which an indemnity is provided under the sliding scale, increasing the exposure to contractor and technology providers’ balance sheets. It is also a concern to see the movement of the series loss clause from the property damage section of covers to be applied equally to moderate loss of revenue claims before the maximum number of physical damage losses have been exceeded.

Steve Munday is Head of Renewables, GB at Willis Towers Watson, London.