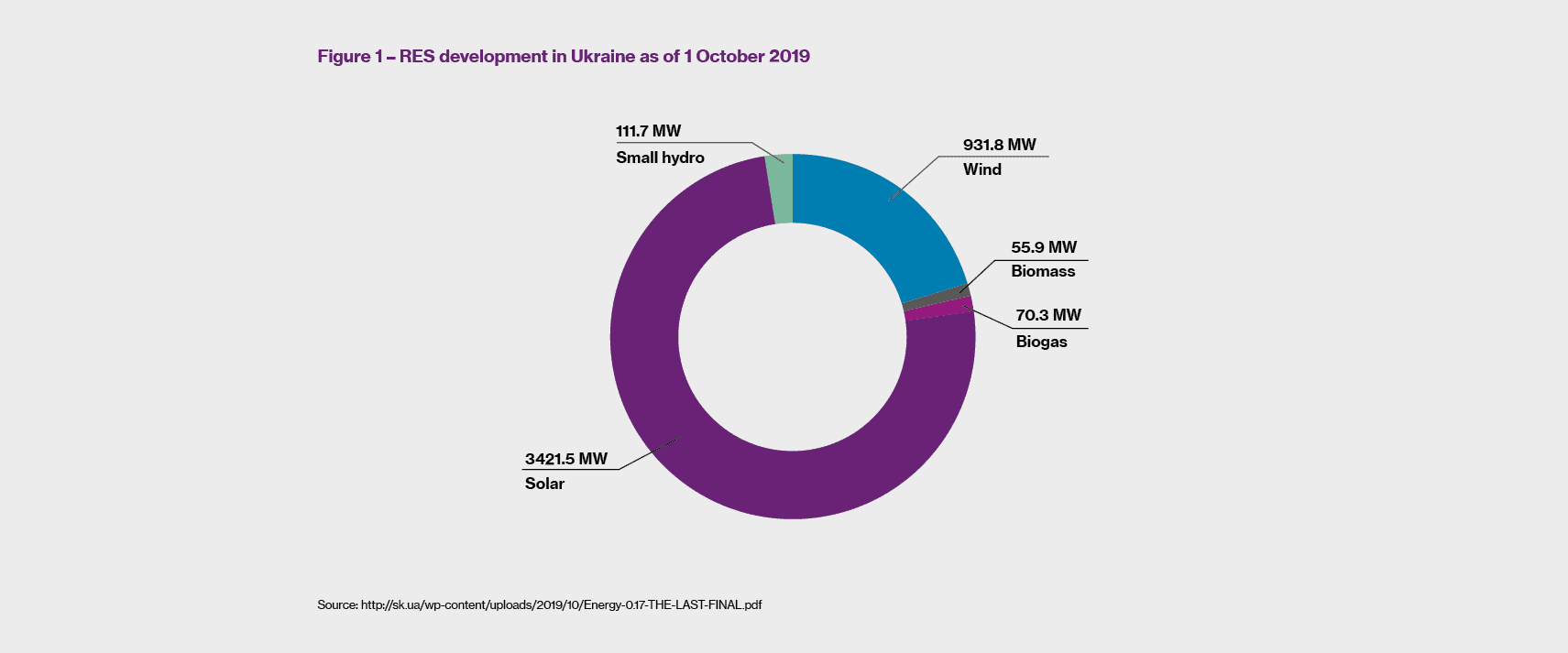

Ukraine has made clear statements about its commitment to develop a large percentage of renewables into their energy mix. According to the nation’s energy strategy, the intention is to have 25% of power generated from renewable sources by 20351. Whilst such lofty ambitions are often merely political rhetoric in many countries, Ukraine has seen a real push towards Solar PV, onshore Wind and other renewable energy facilities, particularly over the last year or so. Indeed, by October 1 2019 the country had an installed capacity of 4.6 GW (excluding large scale hydro) and generated 4% of the nation’s power from renewable sources2.

Despite having abundant wind and solar resources, it is the geopolitical landscape which has really pushed Ukraine towards renewable energy. Since Ukraine’s independence from the Soviet Union, the country has relied heavily on natural gas imports from Russia, as it has limited fossil fuel reserves of its own. The more recent tensions with Russia have forced the country to reduce its reliance on imports from its neighbour and look further afield, a policy which comes with obvious increased costs. In order to help mitigate these issues, energy produced within the country (of which renewable energy is an obvious contributor, given the plentiful resources) will help increase energy security and independence.

In a bid to drive investment in the renewable sector, the state introduced an extremely attractive Feed-in Tariff (Green Tariff) with guaranteed Euro-denominated rates until 2029. With the green tariff being one of the highest in Europe, there has been no shortage of interest and investment by both international and domestic developers who have noted the excellent return on capital available. Importantly, these developers have been backed by major western development banks including, but not limited to, EBRD, OPIC, IFC and EIB3.

However, times are changing; the country has decided to move to an auction system, reflecting a well-trodden global trend by developing nations. The auction system will replace the Green Tariff with full effect from 1 January 2020. Not wishing to miss out on the favourable Green Tariff, investors have been hesitant to change and there has been a major rush of investment in order to remain eligible for the Green Tariff in the years to come.

The requirements are that projects must have obtained land use rights, have agreements for grid connection and construction, a Power Purchase Agreement (PPA) by 31 December 2019 and are constructed within two years for Solar PV projects and three years for Wind projects. The dash to benefit from this tariff has been evident as seen by the fact that “during the third quarter of 2019, 956 MW of capacity was commissioned which is almost 6 times more than the capacity commissioned during the third quarter of 20184.”

However recent events, combined with the change to an auction system, have created a mood of real caution amongst investors and developers. The Green Tariff, whilst hugely beneficial for electricity producers and for the development push of renewable energy infrastructure, has created a heavy burden on state coffers. Under the tariff, the state-owned company ‘Guaranteed Buyer’ is obliged to purchase the electricity produced from renewable facilities at artificially high prices, which is now squeezing the state purse strings. With the tariff so high, the state is experiencing difficulties in purchasing the electricity at such generous rates and is attempting to reduce the tariff.

Furthermore, and of grave concern for developers and investors alike, is that the state is now defaulting on payments for electricity already produced and sold. This now represents a far cry from the financially advantageous as well as stable and transparent conditions anticipated by investors and reflects the concerns of the political risk insurance market when looking at non-payment perils. The presence of the major development banks mentioned earlier will undoubtedly add substantial leverage to the situation as the country can’t afford to see them turn their backs on renewable projects and move their investments elsewhere. However, a worrying situation remains.

The auction system, though an understandable next step for the country in terms of reducing the end cost of electricity and the ability to tailor the auctions to country specific objectives, will still cause concern for investors and developers. Investors require confidence in the system, the state rules and regulation and the off-taker. Such confidence may not be on display in the early auctions as they prefer to take watching briefs to see how the first auctions are realised before deciding whether to put their money back in. This would lead to under-subscription, meaning that there would be an insufficient number of bids to meet the volume demand, creating less competition and consequently a less than expected reduction in electricity pricing.

Amongst the prevailing uncertainty, developers and investors benefit from risk advisors and brokers who have had similar experience with their global clients in developing territories and know how to navigate such situations. Ukraine is not the first country to have transitioned to a renewable energy auction system, with Mexico, Argentina and India already having done so. The appointment of a risk intermediary with both global renewable energy expertise and domestic knowledge, combined with the trust and ability to work with the major development finance institutions, will enable the best chance of success.

Freddie Cox is an Associate, Renewable Energy, GB, Willis Towers Watson London.

1 https://cms.law/en/ukr/news-information/ukraine-launches-renewable-auction-system 2 https://balkangreenenergynews.com/ukraine-launches-renewable-auction-system/ 3 https://assets.kpmg/content/dam/kpmg/ua/pdf/2019/07/Renewables-in-Ukraine-2019.pdf 4 http://sk.ua/wp-content/uploads/2019/10/Energy-0.17-THE-LAST-FINAL.pdf