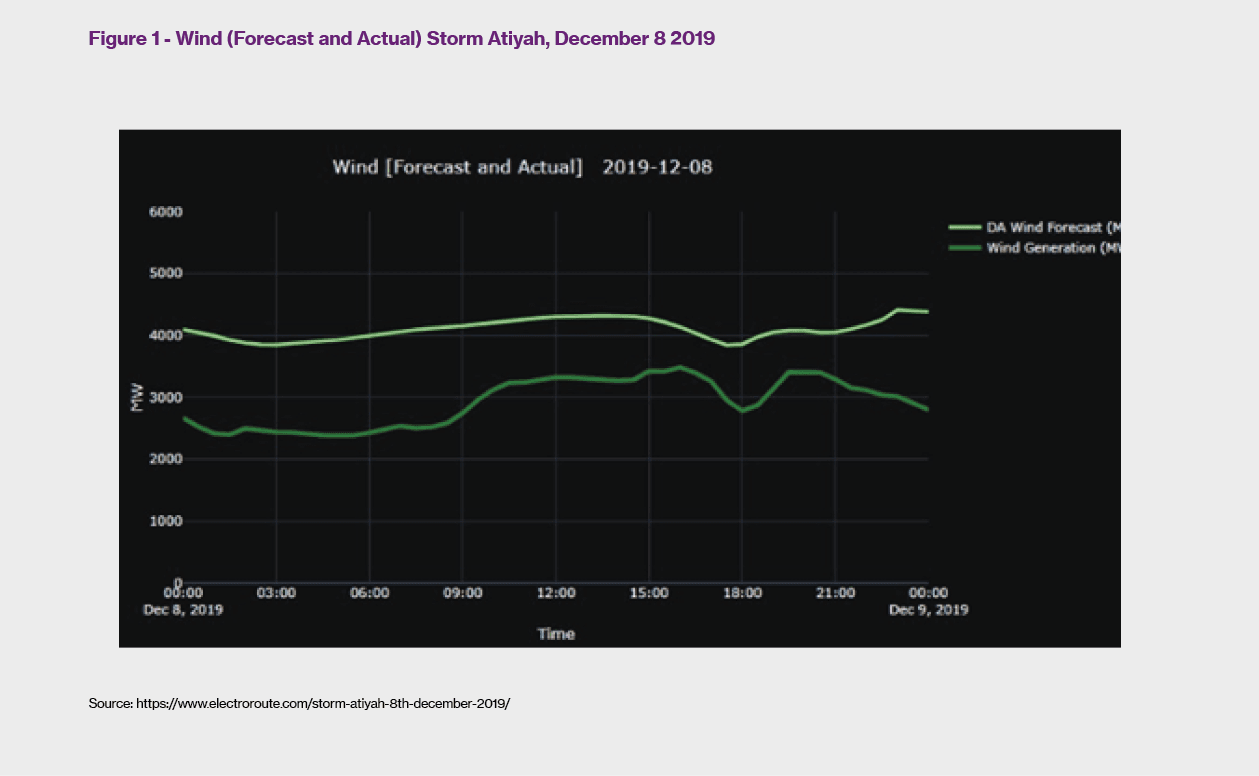

December 8 2019 was a landmark day for the Irish renewable energy sector - and more specifically the onshore wind energy industry. Storm Atiyah was tracking from the north-west of Ireland, with varying levels of wind warnings in place. As the day progressed and against a backdrop of pricing volatility, the permissible limit of 70% renewables penetration on the system was reached for the first time as the Irish system became the first in the world to achieve these levels - levels which are critical to achieving a decarbonised energy system.

This milestone came just six days after the Minister for Communications, Climate Action and Environment, Richard Bruton TD announced long awaited details of the first Renewable Electricity Support Scheme (RESS) auction. The Government has approved key features of the scheme which will give investors and developers some sense of clarity; however. a process of consultation is now underway to iron out the finer details of the new scheme. Subject to state aid approval by the EU, the first auction1 is potentially set to open in June 2020. The announcement of a new RESS scheme came after the government had published its climate action plan which sets out its ambitious plan to tackle climate change. Wind energy is central to the plan, with a target of 3.5 GW of offshore wind energy by 2030 to more than double onshore wind capacity to 8.2 GW and to achieve the overall target of 70% of Irish electricity from renewables by 20302.

The RESS scheme will be open to a range of technologies, including wind and solar, which is intended to help Ireland broaden its renewables mix. It will include a category for community–led projects, subject to state aid approval of up to 30 GWH, and developers will contribute to a fund to support communities.

However, the new scheme will come with a caution for investors, given the experience of similar regimes in territories such as the UK, Germany and India where there have been problems with profitability and low bid volumes. Investors and lenders will need to evaluate their risk transfer appetite, while the new regime presents an opportunity for the insurance market to further develop more innovative index-based solutions to offset uncertainty risk. It will also require developers and investors alike to give further thought to projected revenue figures for Business Interruption coverage (for example) and fully understand policy responses to fluctuations in pricing.

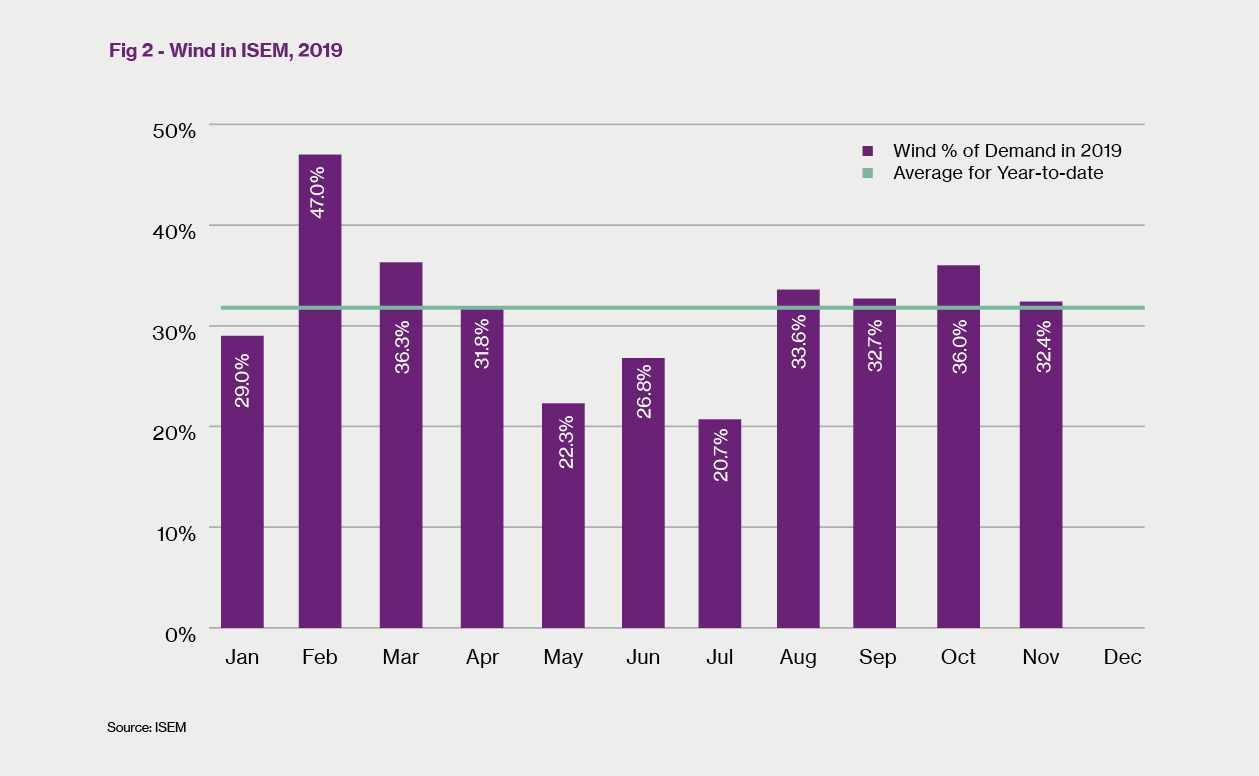

It is now over 12 months since Integrated Single Electricity Market (ISEM) Ireland’s wholesale power market commenced in October 2018. In its first year of trading, ISEM has had issues with pricing disputes as well as significant volatility, as the new format has multiple two-sided markets with the onus of balance responsibility within a capacity auction. The fuel mix has seen a steady growth of wind on the ISEM, with an average of 34% of demand in 20193. Despite this growth, the challenges caused by the volatility of balancing ISEM prices has led to less value in the capacity market for many generators in ISEM compared to SEM.

The Government’s Climate Action plan 2019 provided a very ambitious target for Corporate Power Purchase Agreements (CPPAs) in Ireland by 2030, with a target to ensure 15% of electricity demand is met by renewable sources contracted under CPPAs; it is estimated that this equates to approximately 2.5 MW of installed onshore wind generation capacity supported through CPPAs4.

Considering the EU Directive 2014/95 and the current climate change momentum, the challenge will be to make this a viable effective route to market. However, there seems to be an appetite to make this happen as Ireland is home to more than 60% of the RE100 signatories5, a climate group imitative under which the world’s most influential companies commit to achieving 100% renewable power by a target date.

This is a new phenomenon in recent years and certainly one for which insurers have yet to bring innovative risk transfer solutions to market, except for a couple of US-based specialist providers. However, this is certainly an opportunity and they are keeping a close eye on working to change this position.

It is more than 14 years since an offshore wind project was built in Irish waters; however, there is an offshore wind energy “pipeline” of more than 12 GW at various stages of development around Ireland’s coastline. It is a very exciting opportunity and presents the next step for the sector in Ireland.

The lessons learned from the onshore community in terms of planning challenges, community responsibility, regulation and environmental impact are important milestones and the industry is presented with an enormous potential from its surrounding waters. Offshore brings with it a different technology, but the associated costs have fallen significantly in recent years; as a result, the resources required to bring these projects to fruition will see new opportunities for many stakeholders.

It is very encouraging for the industry to see an indigenous Irish developer such as Saorgus Energy partner with the German energy giant Innogy to bring its Dublin Array project before the department of planning 2019. This project will potentially include 60 to 100 turbines and the capacity to generate up to 600 MW of electricity6. Thankfully the global insurance market has significant experience with these projects and has a track record of delivering effective risk transfer solutions for these projects in many territories; Ireland is not expected to be any different in this regard.

The global Property & Casualty insurance market regained some stability in the early part of 2019, driven by strict underwriting and increased rating strength, following a period of significant natural catastrophe losses sustained since 2017. Lloyd’s reported over £3 billion of losses in the past two years 2017 & 20187 and as a result undertook a remediation plan to maintain capacity levels.

As a result, the reduction in capacity has resulted in a hard market of near post 9/11 levels and the outlook for the UK insurance market remains very volatile. It is hoped that the recent general election result in the UK and the clarity it brings in terms of Brexit will allow both the reinsurance and insurance markets to have more certainty in their planning and potentially settle capacity challenges in the coming months.

Whilst the broader insurance market continues to battle these challenges, as a sub-set the Renewable Energy insurance market has faced a very difficult 24 months and is currently in the eye of the storm. The sector has suffered a series of heavy losses globally, primarily due to more frequent natural catastrophes along with construction and associated loss of revenue losses.

The pool of insurers who provide cover for renewable energy projects was already limited and has further deteriorated in 2019, most notably with the announcement by CNA Hardy to exit Renewable Energy business due to poor market conditions and under-profitability. Their footprint in the market is estimated at US$20m-25m and they were a leading provider in the sector, with experienced underwriting teams in Copenhagen, London and Paris. In recent years, CNA had provided capacity to several Irish projects.

Other providers such as Axis Capital and GCube continue to provide capacity for Irish projects, albeit at increased rates and in most cases with significantly higher deductibles on both property and, more significantly, associated downtime losses. There have been moves by other insurers such as Travelers and Allianz Global Speciality to dip their toes in the Irish market and they are doing so on a selective basis, following a considered underwriting approach with rating strength applied. RSA’s Irish operation continue to provide significant capacity for Irish projects, but they have had their own well-documented challenges in recent years; in terms of Renewable Energy underwriting, it is vital they balance a well-established portfolio with new technology projects to ensure its continuing profitability.

The challenges faced by the market come at a time when the industry is embracing innovation in project technology. Battery storage, increasing hub heights, design optimisation, modular components and increasing outputs are all becoming features of Irish projects; whilst much of this is welcomed by the insurance sector, it is prone to adopting a very conservative approach towards other elements until it brings itself up to speed with its capabilities.

Brian O’Dwyer is Renewable Energy Specialist Corporate Risk & Broking Account Executive at Willis Towers Watson Cork.

1 https://merrionstreet.ie/en/News-Room/News/Government_approves_key_design_features_of_first_Renewable_Electricity_Support_Scheme_RESS_auction_30_Increase_in_Renewables_Expected_in_Round_One.html 2 https://blogs.dnvgl.com/energy/the-irish-wind-industry-looks-forward-to-2030 3 http://www.energycork.ie/wp-content/uploads/2019/12/S.pdf 4 https://www.lexology.com/library/detail.aspx?g=e7675995-0314-4f0a-9b1d-85312f9bad35 5 https://www.eolasmagazine.ie/can-corporate-ppas-play-a-role-in-irelands-renewables-revolution/ 6 https://www.irishtimes.com/business/energy-and-resources/joint-venture-to-build-1-5bn-wind-farm-off-dublin-coast-1.4051797 7 https://uk.reuters.com/article/uk-lloyd-s-of-london-results/lloyds-of-london-suffers-storm-filled-losses-sees-profit-in-2019-idUKKCN1R80IF