In 2018 wind power installed in the countries of the European Union amounted to some 189 GW, second only to natural gas which it is likely to have exceeded in 2019. Wind power represents 18.8% of the EU’s total installed generation capacity with five countries (Germany, Spain, UK, France and Italy) representing in excess of two-thirds of this production1

On the evening of Sunday December 8 2019 wind farms in the UK generated more than 16 GW for the first time representing 44% of the electricity produced that day2. The growth of wind power in the overall mix of power production in UK and the EU has been remarkable and now firmly established in a myriad of global territories.

Wind, as we all know, is a free resource and entirely without emission but it is not entirely predictable: it is both intermittent and subject to diurnal and seasonal fluctuation. Yet the investment required to exploit this free resource brings with it the altogether more predictable strictures of finance: debt service, dividend payments and capital repayment, over 20-25 years.

On average, a wind farm tends to produce the average amount of power that it is designed to generate yet from hour to hour, day to day, month to month the amount of wind is seldom ‘the average’. So while it is entirely obvious, the challenge arises from managing the volatility around this average. When wind is abundant, such as on that evening of Sunday December 8 2019 in the UK, there is more power in the system than it can handle - such that consumers may even be paid to help balance the system. Conversely of course, during periods of low wind production is less than planned; it further confirms that the current energy mix is still critical.

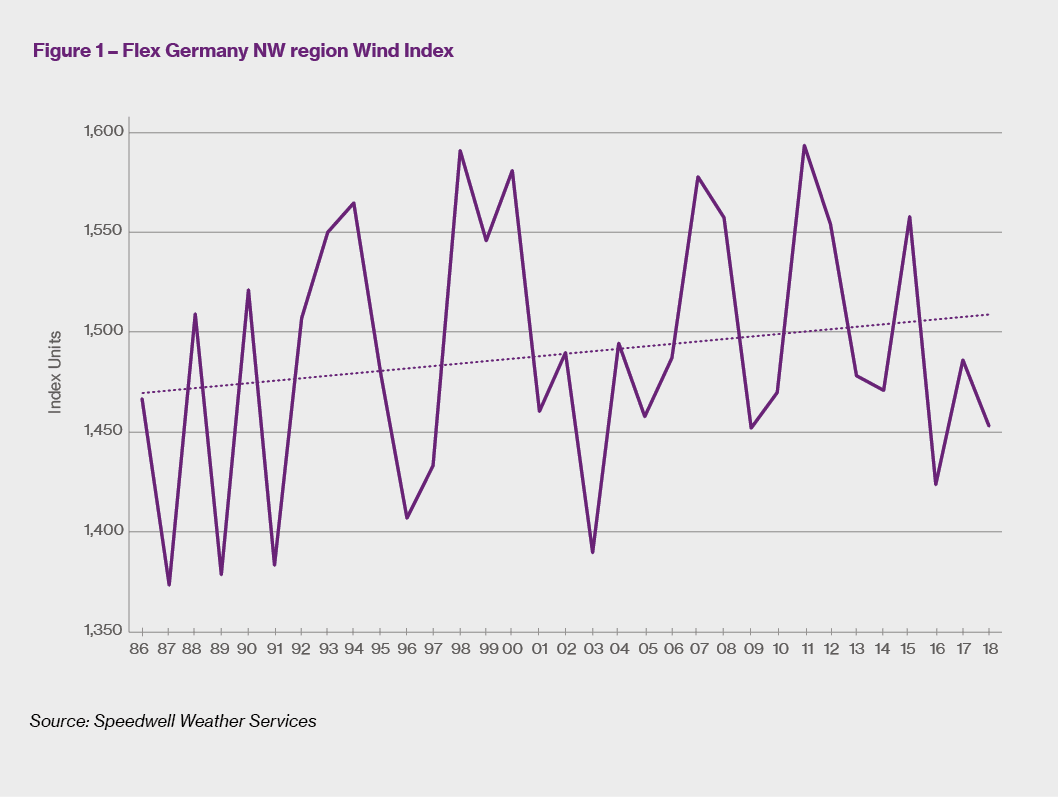

An example from Germany Figure 1 above shows a wind index for north-west Germany for the period 1985-20173. During this period the Production Index fluctuated between 1,192 to 1,594, a range of almost 30% around the long-term average; 20% on the downside. Simply put, this represents a production (and therefore revenue) shortfall which is foregone in that production period.

How do subsidies help manage risk? Since renewable energy production has received some element of price support, it has been the case that wind and other renewable energy producers have benefitted from a degree of protection against low production by virtue of receiving a ‘premium’ price for delivery.

As wind power production operates in an unsupported, auction-based regime, no such in-built protection against the downside exists. This confers new levels of production and performance risks on new projects and those that are no longer the beneficiary of such support pricing.

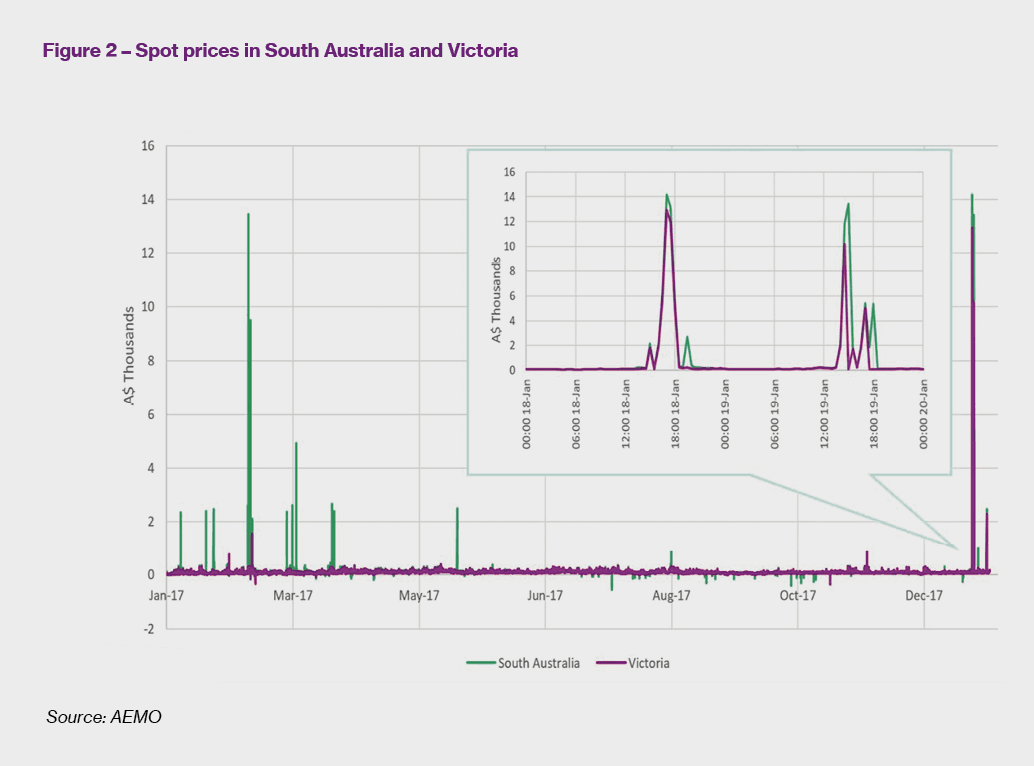

The wholesale price of electricity that a renewable producer receives may be fixed under the terms of a bilateral agreement with an off-taker, typically under the terms of a Power Purchase Agreement (PPA) or may be sold as ‘merchant’ power and subject to the vagaries of the market. The price on the day (even hour) will be dictated by the normal rules of supply and demand. For example in Australia the whole price of electricity can spike from its normal operating range of AU$50-100 to spike levels of AU$500-12,500+4, as per Figure 2 above.

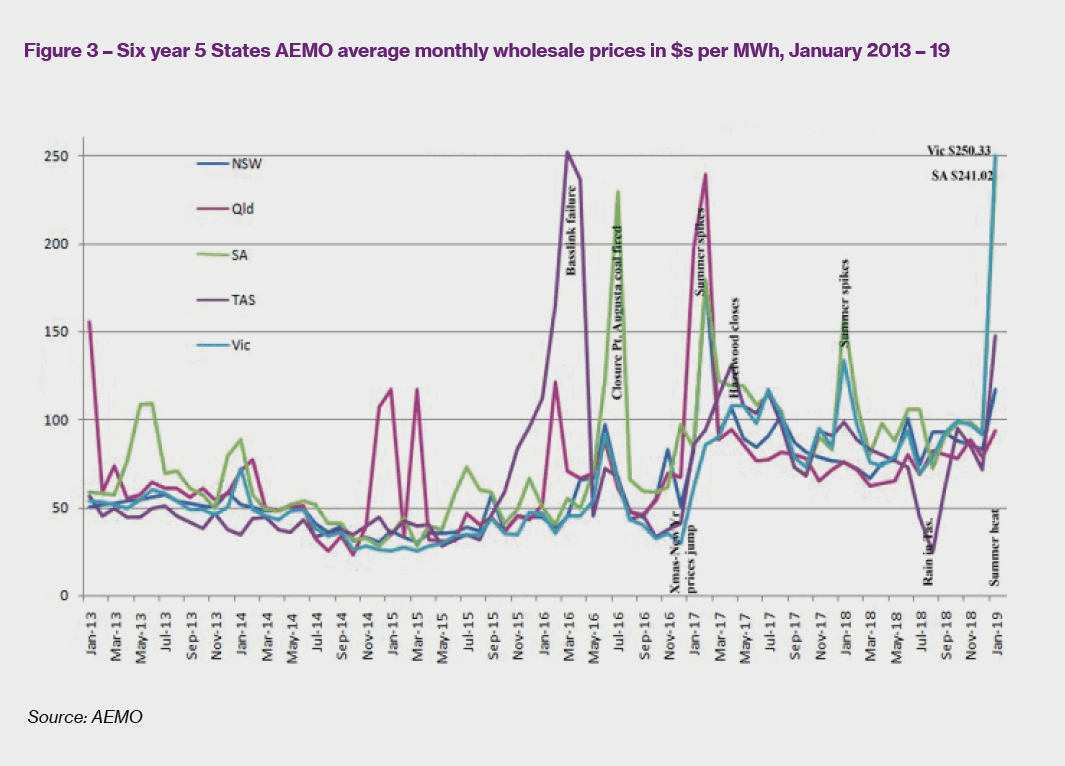

And while spot prices may spike by more than 12 times during the course of a single day, even the average monthly wholesale prices can vary by 5 times or more, as shown in Figure 3 overleaf.

Clearly such volatility in electricity price – often the result of demand spikes during the summer – makes price (and hence revenue) management extremely hard to achieve. Servicing fixed commitments of supply or delivery in such a volatile price environment can leave either buyer or seller with a major shortfall or penalty.

Protection against low wind volume is available in a form known as parametric (or index-based) cover. This form of insurance provides an alternative way of transferring the revenue or cost impact of natural and man-made catastrophe perils, such as earthquake, windstorm, terrorism, adverse weather and pandemic. These solutions differ from traditional insurance policies in that loss payments respond solely to movement of a pre-agreed reference index rather than the normal principles of indemnity based on measured losses.

In fact, the power sector has been the dominant buyer of weather-index programmes since the origination of these products in the late 1990s. Typically power companies use these solutions to hedge their energy demand risk, which has been shown to correlate well with temperatures. Indices based on population-weighted temperature provide a good proxy for the demand for power in certain regions. Derivatives of the indices provide an efficient hedging mechanism for companies whose revenues depend upon high power demand. Since the outset of the weather-index market, the available solutions have become more sophisticated and, in today’s Alternative Risk Transfer (ART) market, index-based solutions are used to address power generation risks wind and low solar as well as power price volatility and power outages not linked to physical damage.

The availability of weather data from satellites along with synthetic and reanalysis data sets now allows weather-index solutions to be developed in territories with a limited network of ground stations as well as for offshore locations,

which in the past were no-go area for these products.

Parametric solutions are driven by data. The data is needed both to:

Given that the index payment is published in real time, two weeks would not be an unrealistic timeframe for settlement.

There are various sources of wind data – they may be obtained from an anemometer reading from a wind mast or turbine. Operational wind farms have Supervisory Control and Data Acquisition (SCADA) systems which record all aspects of the actual wind regime at turbine hub height which is clearly most representative of the site itself. For projects which are not yet operational and therefore do not have history of recorded wind data, then various proxies or modelled (so-called re-analysis) datasets may be applicable.

Of particular concern is that data, analysis and contract performance are achieved on a like-for-like basis. In this way the buyer and seller can each have confidence that the contract will perform as anticipated and, critically, that low wind events will be faithfully captured by the process.

Prerequisites for good programme design should include the following:

In order to structure low wind protection, the wind history most appropriate for that site is analysed and modelled to establish a distribution of expected power generation for the project. This modelling will also take into consideration the type(s) of turbines that have or will be commissioned, their associated power curve(s), numbers.

Such modelling cannot explicitly take into account non-availability of the turbines due, for example, to mechanical breakdown or failure, miniatous or other heterogeneous outage. A general availability coefficient may be applied as appropriate.

The flipside of the parametric trigger is the concept of ‘basis risk’, that is the risk that the payments under the parametric contract do not precisely match the loss of revenue or increase in costs sustained by the insured. This arises as a result of the parametric solution responding to the occurrence of an event or movements in an index, as opposed to the losses actually sustained by the insured. It is important that this basis risk is properly considered in the design of any index-based contract. It must, wherever possible, be estimated and discussed between buyer and seller to ensure absolute transparency.

However, this potential for mismatch between actual loss and contract pay-out is certainly not confined to parametric structures. Conventional contracts of insurance and reinsurance also contain terms and conditions (exclusions, warranties, deductibles, waiting periods and the like) which can significantly limit the insurer’s payment obligations. Some would argue that

these conditions of non-payment are far more penal and prone to subjective interpretation than the relatively simple operation of an index.

Although basis risk is a potential disadvantage of parametric contracts, this structural approach remains a more suitable basis for the efficient participation of alternative risk investors, particularly in respect of the risks of corporate buyers. The participation of the capital markets in such structures expands the pool of capital available to support such programmes and the policy limits that can be negotiated.

Put simply, any party that is carrying low wind risk should manage it. This could be any one or more entities in project life cycle and the parties may indeed change during the life cycle from design and conception, funding to build, operation and maintenance. Portfolios of wind projects have increasingly been reviewing their risks for low wind.

Our weather index solutions team advises global clients in the power sector and is uniquely positioned to provide both insurance and derivative solutions for the low wind risks. For any party with interest in researching the options available to them to manage the risk associated with low wind, we would be pleased to assist and provide advice on the possibilities and solutions provided by today’s expert insurers.

Julian Roberts is Managing Director, Alternative Risk Transfer Solutions, GB, Willis Towers Watson.

Claire Wilkinson is Managing Director, Structured Risk Transfer Solutions, GB, Willis Towers Watson.

1 Source: WindEurope 2 https://www.dailymail.co.uk/sciencetech/article-7772499/Windy-weather-sets-new-renewable-power-record-Britain.html 3 Source: Speedwell Weather Services 4 Source: Australia Energy Market Operator