Two new Concentrated Solar Power (CSP) plants located in Israel reached a critical phase of their lifecycle last year –the start of their testing and commissioning phases and consequent transitions into full-time operation. This crucial stage in the projects’ lifecycle, when the CSP plants were fired up to full power, had insurers of the construction phases on the edge of their seats. Those who had agreed to cover the operational phases also watched with full attention, eager to find out whether their commitment to underwrite the first year of operations was a wise decision.

Geographically, these plants - Ashalim A, a 121 MW Parabolic Trough (PT), and Ashalim B (also known as Megalim), a 121 MW Solar Tower (ST) – are situated across the road from each other. And whilst both are classified as CSP projects, their risk profiles are very different.

Parabolic Trough (PT) leads the way Globally, PT is leading the race as the dominant technology choice in the market. Out of the top ten CSP projects by size, nine are PT and only one is a Solar Tower (ST) – the 377 MW Ivanpah Facility in the Mojave Desert, which is further made up of three individual ST’s1. This installation had the first-ever utility scale direct steam ST’s . This dominant theme continues through the top 25 CSP projects worldwide, with just two out of this group being STs2.

In this article we will examine the tale of these two technologies: the different risk issues, how the insurance market has responded, and critically, what a project owner can do to derive optimal terms from the global renewable energy insurance market.

Large scale PTs have been in operation since the 1970s. This rich history has given many years of proven operational experience globally; subsequent operational issues, failure modes and long-term performance have become better understood as the decades have unfolded. Accordingly, this has established a strong supply chain of both developers and contractors (EPC & O&M etc.) with in-depth knowledge of the technology.

In fact, the technology was designated as being fully mature by the National Renewable Energy Laboratory (NREL)3 in 2003. Subsequent advancements in the technology are focused on technical nuances to increase performance and efficiency rather than large leaps, in as will be evidential in the ST type.

Moreover, PT losses, such as broken concave mirrors or natural peril related losses, have given the insurance market, contractors and designers a greater understanding of the risk issues faced by this technology, given that this loss data has been fed back into improving the technology over the years.

This track record, together with the insurance market’s increased understanding of these risks, has released increased capacity to underwrite such projects. PT Plants regularly leverage this increased supply to obtain broader and relatively cheaper insurance cover than is currently available to plants featuring the ST technology.

Being a relatively newer technology, with the first projects developed in the late 2000s, STs face greater unknown financial, technology and technical risks than PTs. Both the tower and the Solar Receiver Generator (SRSG), the standout components of a ST plant, are generally labelled as large risk by the insurance market and are notably less proven at scale.

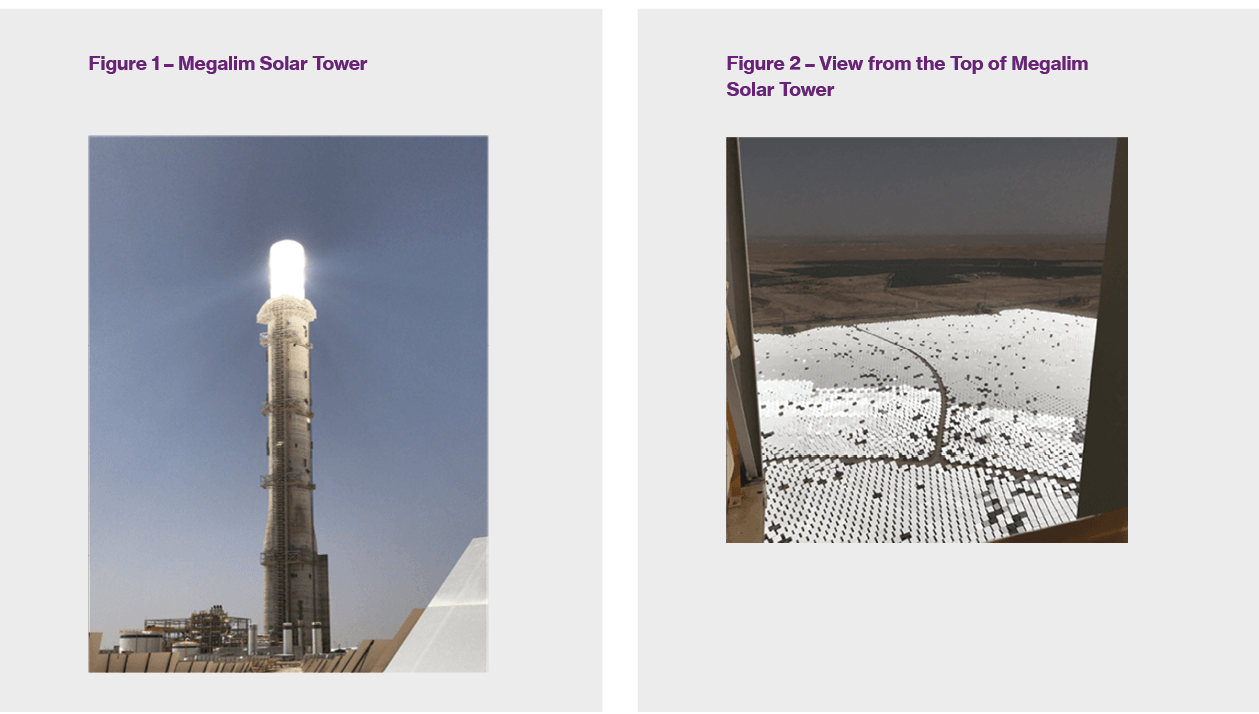

At 250 metres, the Megalim CSP plant in Israel (Figure 1 above) boasts the highest solar tower in the world4. It also has the largest heliostats (reflective mirrors) by surface area, technology considerations for many underwriters – where positive risk engineering, understanding and collaboration between such projects and their insurers about these evolutions can help, in part, to understand and such developmental concerns.

The supply chain is also limited; there are only a small group of companies with the knowledge and expertise to make the unique components of the technology, such as the heliostats and the SRSG. Projects built using the same contractors continue to implement lessons learnt from their predecessors; this gives the market greater comfort, but there are still many unknowns with the uplift in project scale and advancement of technology.

ST complexities and concentrations The SRSG is a very complex structure which is custom made for a ST project. The tower and SRSG in unison represent a single point of failure for the plant. If any of these units fail, then the entire plant is taken offline, which creates a significant DSU (Delay in Start-Up) exposure during the construction phase, or BI (Business Interruption) exposure during the operation phase. The lead replacement times for these items are generally quite long; sourcing spares to keep on site is often uneconomical.

Natural risk is also a concern. The tower itself must be built to survive the local atmospheric weather and earth conditions, as well as natural phenomenon such as earthquakes. Moreover, the SRSG is of considerable mass; the significant load at the top of the tower, with large volumes of high-pressure fluid flowing and quantities of energy fluxing through, add to the technical challenge. One underwriter recently described this technology type as having a “very heavy boiler on a stick” (in Megalim’s case, 2,500 tons). The SRSG is a significant cost of the technology, generally around 10% of total capital expenditure5; should this be damaged, the cost of repair is high. Allied with this is the likely long lead time to repair or replace, which can cause a significant drop of production and financial loss to a project. All this will be factored in by a technical engineering underwriter before even considering the other single point of failure, the conventional steam turbine that is situated at the base of the tower (this is also an issue for the PT).

Given the limited number of STs in operation, most of the losses to date have occurred during the erection of the plants. History has shown contractor negligence, and the failure of auxiliary boilers and booster heaters in STs. Natural events have also led to losses; there has been flooding at a project as a result of a thunderstorm, and high winds damaging heliostats.

Common mechanical, electrical breakdown and fire risks must be addressed within the solar tower. If the focal point of the mirrors or a subset of these (and there are many) is marginally off the intended target, then the sun’s rays may be focused on a section of the SRSG not designed to handle the large influx of solar energy. One fire at the Ivanpah facility6 was the result of just this scenario7; the situation was only made worse by the fact that the fire occurred some 200 metres up in the air - an issue which a Parabolic Trough power plant would never have to contend with. Besides the Physical Damage element, projects can be plagued by lower than expected production; for example, the Ivanpah facility took a few years for performance to reach 97.5% of its contractual power output8. Prudent insurers would look to ensure that these issues are taken into consideration on future projects.

We are already seeing more of this power tower technology being planned globally9, particularly in the United States where projects generating as much as 2 GW are now being planned10. If they come to fruition, these will comprise ten individual 200 MW power towers in the Nevada Desert, with the additional of molten salt energy storage for 24/7 operation; a similar largest scale project is being considered in Saudi Arabia11.

In parallel, the emerging trends of climate change, geopolitical concerns and cyber risks are new considerations for developers. The insurance industry is offering new and alternative solutions in this sphere and it will be interesting to see how both existing and future projects approach these risks.

The insurance programme placement process for CSPs is complex. Capacity in the market is limited, as historic claims have led several insurers to remove CSPs from their strategic plans; only a few now possess the technical understanding to effectively underwrite these projects. However, in the case of PT technology there are decades of precedent on which insurers can base their understanding of the risk and subsequently guide their underwriting. In contrast, ST technology suffers from a limited number of predecessors; as such, delivering optimal insurance programmes can be particularly challenging.

Some segments of the wider insurance market, particularly smaller players who are comparatively “risk seeking”, are keen to get closer to this technology. However, they are not positioning themselves to lead such a technical programme and overall risk appetite and line sizes remain relatively low.

“Safety first” approach The general market approach to any novel technological development, such as the advancements to the ST type, is to constrain cover and/or charge a higher premium for the heightened risk until an operational track record is established. For some insurers, if a technology appears in their opinion to be “unproven”, then even the prospect of charging additional premium is generally not enough for them to deploy their capacity. Instead, they would look to further constrain cover and/or reduce line size – and sometimes to decline the risk all together or limit to external perils only. It is often said that insurance is not an appropriate solution for prototypical technology risks, which should remain instead with the developer or the manufactures; indeed, the low carbon sector is coming to terms with this at present on several clean energy technologies.

A project owner also needs to be aware that the market views operational risks as a different risk profile to that of construction. Specialist insurers who write the construction are often not interested or able to underwrite the operational phase – it’s not in their risk appetite or treaty permissions. Losses during construction will further impact underwriter interest as operational underwriters consider their position. Recently the market has seen the withdrawal of key construction markets due to losses faced across many different types of risks – sadly this has also meant many job losses; this has added uncertainty into the mix. A project owner should be aware of how the ever-changing insurance market dynamics can impact their project.

As with any power project, the underlying maintenance period provided by the construction insurers is crucial, as any issue during the initial years of the operation can be latent from the construction activities. If there is a loss event, and there is not a seamless panel of insurers on both placements, and furthermore it is unclear from the root cause analysis whether the loss is resulting from construction defects or operational issues, disputes may arise. History has shown us that those who write the construction policy - even the incumbent lead - are not necessarily going to write the new stage of the project’s life.

As with any placement, a knowledgeable lead insurer is a crucial part of the process. An inexperienced lead market underwriting the technology may discourage follow markets by under-pricing and/or agreeing cover and terms which are simply unsupportable.

The “long walk” For the largest and most complex of this class such as STs, the placement process is considered in the market as “a long walk”; this relates to the days of brokers walking around the market and negotiating fiercely to obtain capacity at the desired terms. Where large values must be covered, many insurers will be required to complete a placement.

Firstly, this scenario does require a reputable lead to set the terms. In special instances, the use of a lead and a co-lead underwriter to collectively pool market knowledge can help refine terms and provide greater confidence to other participants in the marketing process. Positioning both a lead and a co-lead insurer also gives a project greater insurance security should the lead decide not to renew after their policy period has expired. This can happen, in today’s market, as projects transition from construction to operation and underwriting strategies change including that of the Decile 10 Lloyd’s initiative. The hard market and scarcity of knowledgeable leading markets has also seen the resurgence of lead underwriter engineering fees, payment for their time and expertise in often extensive assessments of the complex risks. These also have to be factored into the ultimate risk premium to the client.

The effect of Decile 10 Equally important is the state of the insurance market which is facing significant hardship. In London the “Decile 10” initiative at Lloyd’s - a historic home for unique and difficult risks, and where much of the expertise for underwriting these risks exists - has resulted in increased scrutiny of loss-making syndicates and power risks. Power in general has faced significant underwriting losses as of late, and all eyes at Lloyd’s are on profitable growth.

As a result of the hardening market and apprehension to this technology, it is expected that concessions will have to be made by all by project owners, lenders, contractors and insurers to get to a point where a bankable and 100% support insurance programme is delivered - a process that typically involves significant negotiation and mediation by the placement broker.

Any major placement of risk for a CSP facility requires a collective, globally coordinated marketing approach. Gone are the days of underwriters deploying plentiful capacity in the power sector; insurers are unlikely to put down large lines, even when the limits are generally quite low. The type of technology configuration, down to the finest details, will have a further bearing on their approach.

From a cost perspective, the price of insurance for CSP programmes can be twice as high as compared to conventional power classes. Moreover, ST risks are considered comparatively more expensive than PT programmes, both for the reasons already discussed but also due to the existence of the power tower and equipment at height, which further raises the risk profile (and Probable Maximum Loss) during both construction and operation phases.

When taking a CSP risk to market, brokers are finding that underwriters who previously would have written these types of risk are now much more cautious. Close collaboration between the project and insurers, augmented by brokers in market roadshows, are an invaluable and often overlooked part of the placement process, even for a renewal. Insights into the technology types and experiences of the past are crucial, certainly for novice STs. Although underwriting capacity is relatively limited in today’s underwriting climate, there is still enough available to deliver a comprehensive programme for even the largest plants out there; London, as the home of insurance, has all the connections and routes into other global markets to make it happen.

A constant and clear flow of key information from project team to insurers helps the latter to better understand the risk and will lead to the best possible results. It is a given that insurers will request a significant amount of project detail. This will include technical information, risk management plans and protocols, replacement times, financial models, plant layouts and, where possible, detailed independent risk engineering surveys. Making such documents available and responding to follow up questions in ample time is crucial to aiding the markets underwriting process.

Following the underwriters’ understanding of the technical aspects of the projects, the next element to consider is the coverage that has been requested. An insurance advisor, that has as strong understanding as the underwriters of both the technical and commercial aspects of the project, is crucial to delivering a fit for purpose and cost-efficient solution. They should be engaged in the process as early as possible.

Finally, it should be noted that if lenders are involved there must also be open communication between both project and lenders insurance advisors so that the insurance requirements are not set too wide, but in a form that allows for such a streamlined solution.

Future insurability of CSP On the whole, insurability of the PT technology has its grounding on the numerous projects already built and operating. There may be minor adaptations to the technology, improvements to some Steam Turbine Generators here and there, larger fields and some changes to the designs, but this technology is mature and insurability comes down more to the posturing of the insurance market rather than technical issues.

However, future insurability for ST is more uncertain. The technology is going to be advanced over time; the power towers may get taller, the mirrors larger and fields more extensive. As the design evolves, the price of the technology will fall, interest from developers will increase and the role of insurance to make them bankable will be even more crucial to the continued growth of this technology. Effective risk management and transfer are necessary to protect all parties’ interest, which will act as a feedback loop. And as bankability grows, greater investment will go into Research & Development to further drive down the price.

The success or failure of the latest projects as they move into the operation phase will be a significant test of the insurance market’s appetite to take on these risks. However, it is important to consider the difficulties that the insurance market is facing, especially in the traditional construction markets, and now we have a situation which could go either way for the insurability of this technology. If it goes well, capacity will increase, driving competition for such risks and reducing the cost of insurance. And further innovative insurance structures can be designed, or capacity accessed from non-traditional means, in order to provide these projects with the required protection.

Myles Milner is an Account Director, Renewable Energy GB, Willis Towers Watson.

1 https://cleantechnica.com/2016/04/27/ivanpah-raised-performance-second-year/ 2 https://en.wikipedia.org/wiki/List_of_solar_thermal_power_stations 3 Executive Summary: Assessment of Parabolic Trough and Power Tower Solar Technology Cost and Performance Forecasts 4 https://www.powerengineeringint.com/2017/01/10/israel-building-world-s-tallest-solar-power-tower/ 5 IMIA Working Group Paper GW 84 (14) – Solar Thermal Power 6 Source: San Bernadino County Fire Department 7 https://riskandinsurance.com/solars-risk-challenges/ 8 https://www.technologyreview.com/s/601083/ivanpahs-problems-could-signal-the-end-of-concentrated-solar-in-the-us/ 9 http://analysis.newenergyupdate.com/csp-today/siemens-supply-turbines-giant-dubai-csp-plant-saudi-arabia-targets-27-gw-csp 10 https://www.solarreserve.com/en/ 11 http://analysis.newenergyupdate.com/csp-today/siemens-supply-turbines-giant-dubai-csp-plant-saudi-arabia-targets-27-gw-csp