In our last Power Market Review, we categorised the energy transition as an “undiscovered country” of change for the energy industry1. For the power industry, the form of this transition is now clearer than last year and represents a significant opportunity for growth as we electrify more of our industrial, transport and industrial infrastructure, moving from fossil fuels to zero-carbon power sources. It is also full of opportunities for those bold enough to start mapping out that landscape and stake a claim.

In 2018, the Intergovernmental Panel on Climate Change2 demonstrated what it is at risk: “global warming must not exceed 1.5°C to avoid irreversible loss of the most fragile ecosystems, and crisis after crisis for the most vulnerable people and societies.”

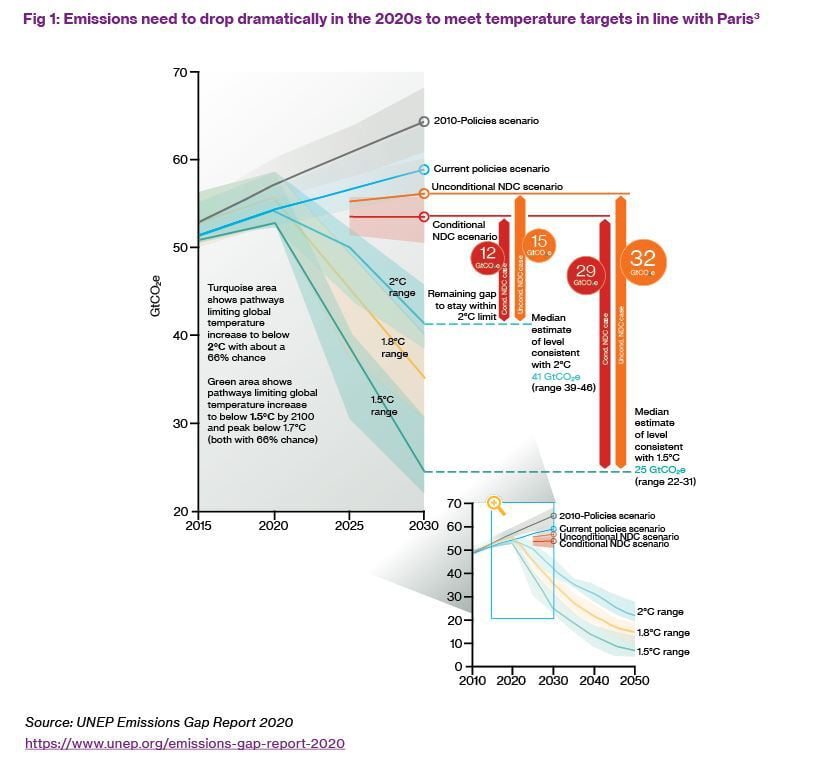

The scale of the emissions cuts needed may seem daunting to meet the 1.5°C limit challenge. Greenhouse gas (GHG) emissions must more than halve by 2030 (roughly equivalent to 7% per annum reduction over the next decade) – and drop to net zero by 2050. The economic disruption in 2020 from the COVID-19 pandemic resulted in an approximate 7-8% drop - the largest ever post-war reduction in GHG emissions4 5. They also weren’t permanent; 2021 is seeing these already rebounding significantly as economic activity has picked up, with energy emissions expected to rise by 4.8%6. Clearly, despite much progress, scaling this transformation is going to be a key objective for the next decade.

As yet, there is no common or scientifically based definition of what “net zero” will mean. It’s not just about the end goal definition and what constitutes reasonable residual emissions – e.g. as little as 0.4GT p.a. globally by 2050 or less than 1% of 2019 emissions7. The trajectory is also important; deep cuts in emissions are needed this and every year towards 2050, across all industries, for the world to meet the Paris Agreement goals.

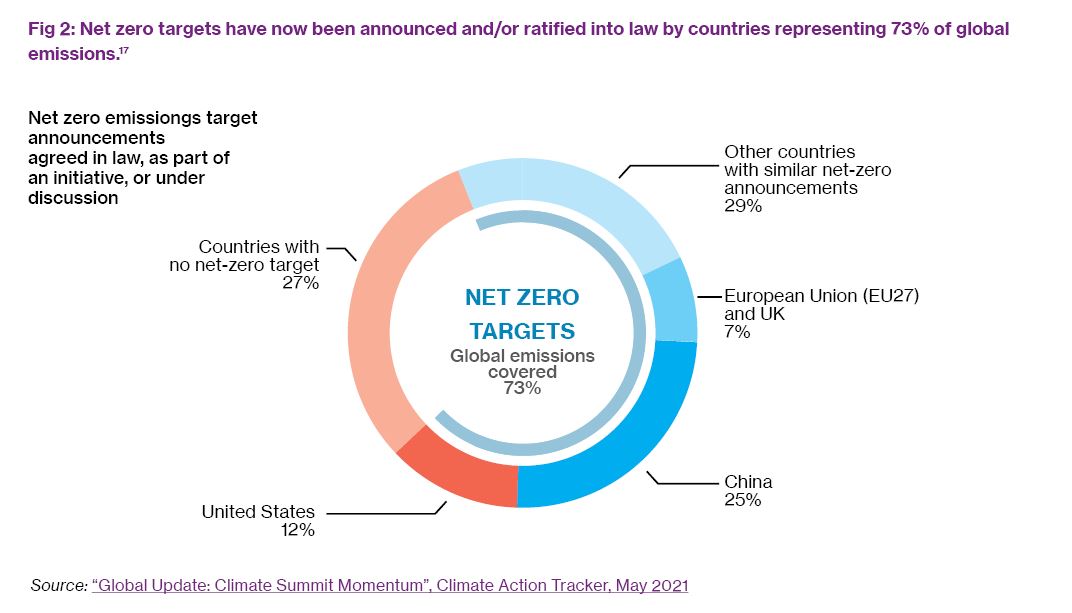

Industry and Finance are accelerating their plans to meet these goals, albeit not quickly enough yet. The period of June 2020 to May 2021 saw a greater than 100% increase in the commitments to, and setting of, Science-Based Targets by power sector companies in the year, compared to the combined total from the previous five years.8 Similarly, long term pledges to net zero doubled in 20209, with organisations representing nearly 25% of global CO2 emissions and over 50% of GDP committed to achieving net zero by 2050 at the latest.10

As BlackRock Chairman and CEO Larry Fink wrote in his 2021 letter to CEOs: “there is no company whose business model won’t be profoundly affected by the transition to a net zero economy”11; understanding the various drivers, risks and opportunities from this change will be essential to building understanding. Many of the current solutions across industry and government rely on the power sector to lead the way in decarbonisation and achieving zero-carbon power.

Scenarios and risk analysis provide risk managers in the power sector with tools and data to support boards with strategic decision making. Leveraging this thinking into explicit transition plans that map the route ahead will help articulate this vision and extend confidence to investors and wider stakeholders that organisations understand the risks and have a map so they can navigate towards a more resilient future. Mapping the risks and opportunities will involve being able to assess your business and value chain against the following types of climate risk:

As highlighted in our previous Review12, the energy system transition is gaining momentum, driven in part by:

Key updates over the last few months include the following:

1. Shareholders are raising their voices and litigation is increasing in western economies

These are no longer niche issues. In the last month, AGM votes at major oil & gas firms in the US calling for targets including use of sold products13 and the election of new climate-focussed board members14. On the legal side, in May a Dutch court has given a landmark ruling to force a major European oil & gas major to raise its emissions reductions targets to be in line with the Paris agreement15. At the time of writing, there were over 1,800 open climate litigation cases globally, predominantly in the US16.

2. Policy makers are also responding

The disruption to the economy from COVID-19, plus increasing vocalisation from society, has demonstrated tangibly that policy makers can intervene at the scale needed to keep emissions within the budget. This has been exemplified by low carbon COVID-19 recovery packages such as the European Green Deal18, with 25% of all funding going to climate change mitigation. The last month has seen a rise in policymaker activity:

In the run up to the COP26 Climate Conference, we would expect this activity to grow globally in both the public policy domain as well as in private enterprise.

3. Financial services are responding as well

COP26 is also accelerating activities in the financial services industry, with similar commitments and partnerships emerging, such as the Climate Transition Pathways initiative that is described later in this article. This is because the energy transition is a strategic risk to the financial services industry.

Following the 2015 Paris Agreement, the number and size of financial services climate initiatives has snowballed, with perhaps the single biggest accelerator being the recommendations of the Task Force on Climate-Related Financial Disclosures21. The financial services industry has also come together, with societal bodies such as the UN, to form many initiatives and solutions focussed on helping to achieve climate resilient transformation in the finance and investment industry.

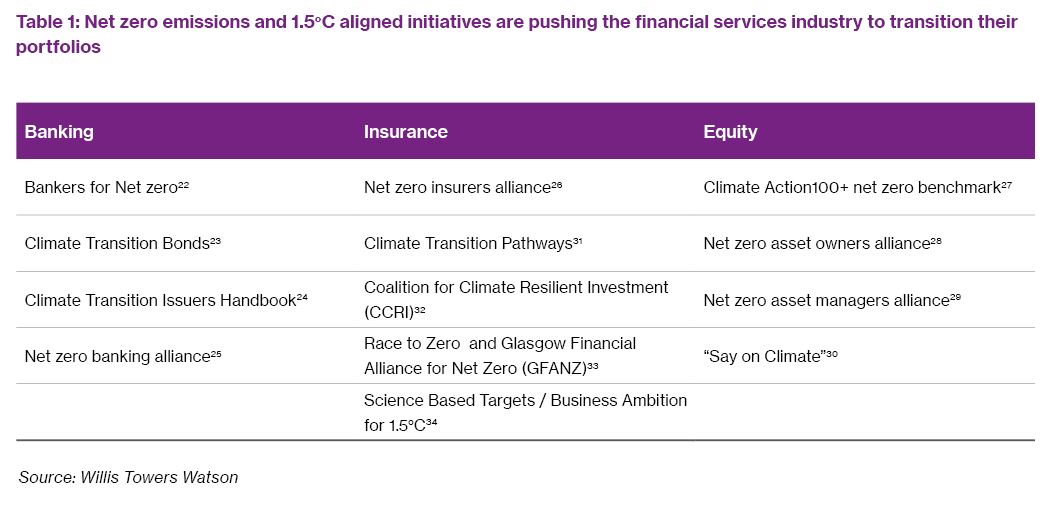

Some of the key initiatives currently underway are outlined in Table 1 above.

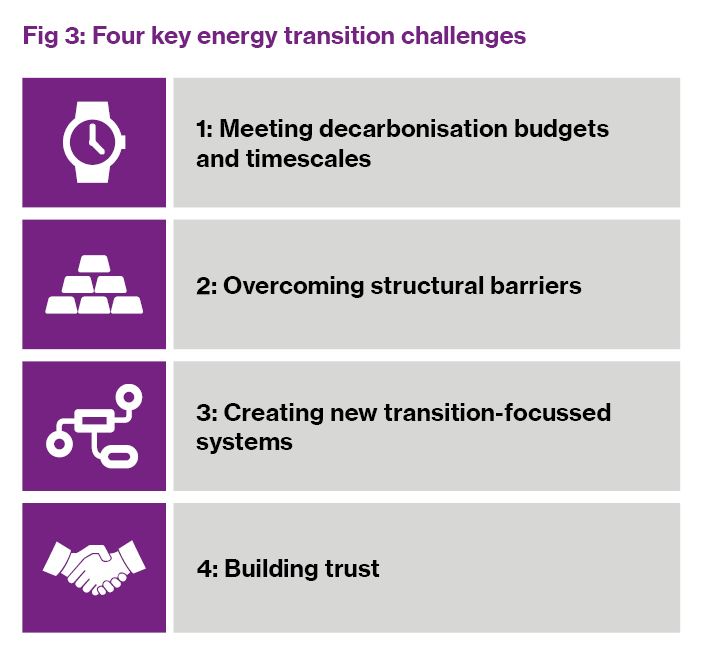

The challenge to transitioning our energy systems is akin to trying to change the design of an aeroplane (body, engines, fuel and equipment) in mid-flight. The transition needs to be managed in an orderly and just manner, as livelihoods and wellbeing also depend upon energy availability. There are four key challenges to be aware of.

Power firms need to set short, medium and long-term emission reductions targets that keep within science-based and apportioned carbon budgets. The energy sector as a whole needs to decarbonise more rapidly as other sectors face significant technological barriers and will increase their reliance on the energy industry to supply zero carbon power; these include steel, cement, shipping and aviation.

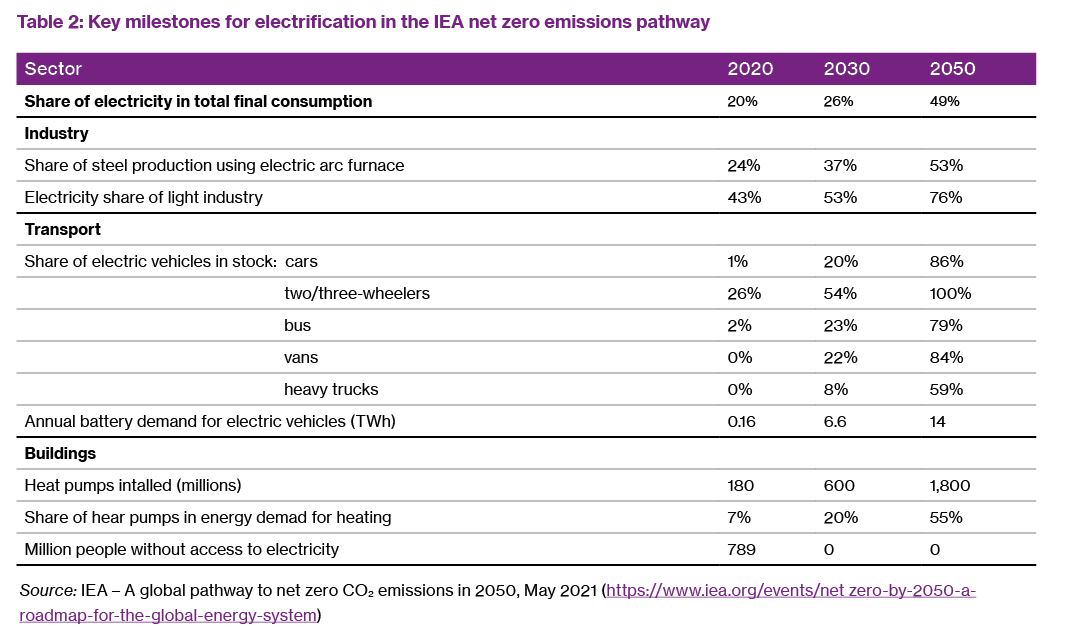

For the power sector, emissions reductions need to 76% by 2030 to achieve 1.5°C, with near zero reach by 2040-204536 - all of this while also growing supply significantly, by nearly 2.5 times by 205037. It should also be noted that:

Before 2030, we are likely to see some major climatic events which will accelerate the sense of urgency with which policy makers feel they need to change the ways in which we make energy available for power, transport, industry, agriculture and domestic use. Rewiring business models to respond to these dynamics will require many structural barriers to be overcome, especially as the past will not necessarily be the best guide for the future – a future which will require new financial tools.

This is where risk managers have an important role to educate Boards on the wave of change on the horizon across a range of issues. At a macro level, this might include shifting geopolitics, as we move from world economic powers of petro-states to electro-states. This could see a drop of 51% in government revenues from oil and gas over the next two decades39, and an opportunity for power companies to attract new investment. Geo-political power40 in the energy transition will derive from:

Economies will also need to deliver against the Sustainable Development Goals, particularly the just transition in providing affordable energy and decent jobs. Power businesses will need to improve their knowledge of these changes, retraining and reapplying their workforces to deliver the new infrastructure build rapidly and attracting talent from other high-skilled sectors to meet growing power needs. They will also need to ensure that corporate culture, values and compensation packages are aligned to ensure successful delivery of their transition strategy.

The energy transition is not going to be just a like for like replacement – systems thinking will be needed to create hubs of interlinked industries and to scale the new energy infrastructure rapidly, including carbon capture and storage, hydrogen and renewables. It is likely to change the dynamic of how we do business both at industrial scale and at retail.

Electrification will offer different business models as generation patterns change42. Power grids will need to be expanded to cope with the increased electrification of our energy systems, be adaptable to more extremes in weather and long-term changes in climate and be able to cope with the two-way push-pull of supply and demand.

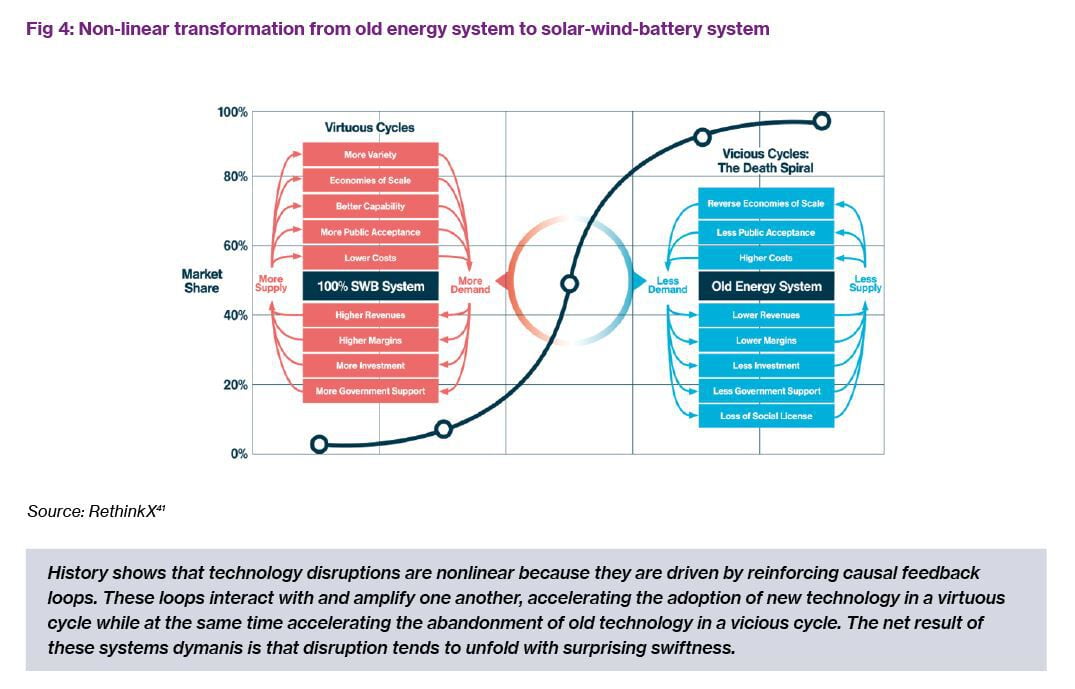

These systems will not only have to engineer the GHG emissions reductions needed to meet tough Paris-aligned targets; they will also have to take into account the rapidly changing pricing of solutions such as solar, wind and battery storage.

The energy transition is a 30-year+ global industrial and societal revolution. Three key things will be needed for this: political will, public support and capital. The energy industry must rebuild trust, as many initiatives to rebrand as green have failed in the past; this also makes it unlikely that claims without evidence of action will be labelled greenwashing this time. Transition plans will need to be robust and that performance is aligned to these plans to insurers, credit providers43 and shareholders44 45.

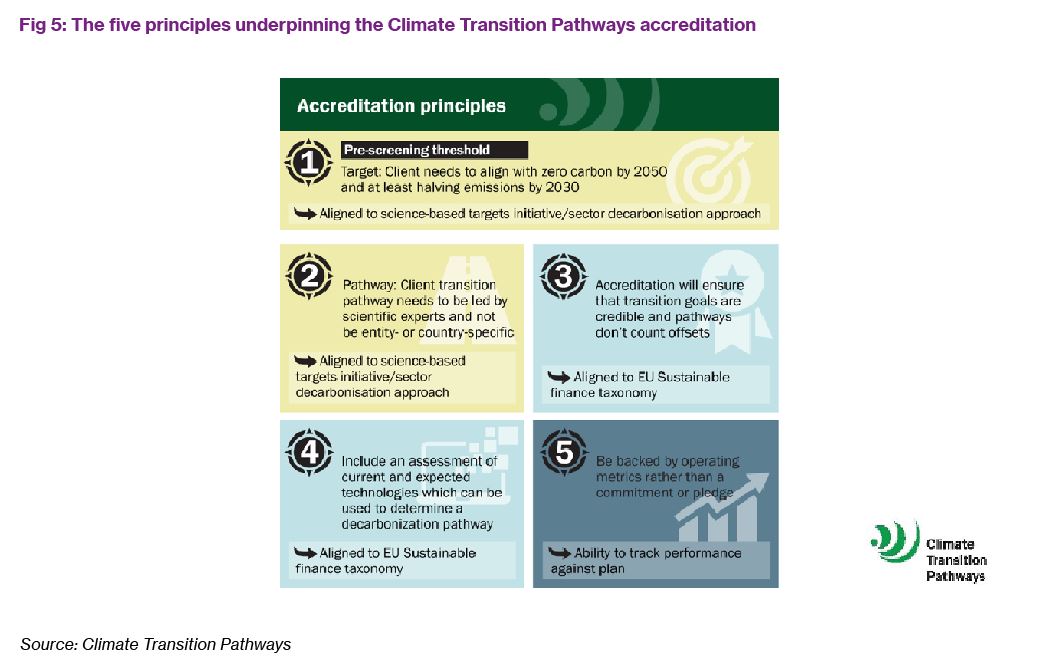

One of the challenges for many stakeholders is being able to understand whether an organisation’s transition plan really is aligned to delivering the Paris agreement. Climate Transition Pathways attempts to resolve this issue by providing an accreditation of the transition plan; it is underpinned by five principles (see Fig 4) to bring rigour to this accreditation that are aligned to the major transition and net zero financial initiatives listed in Table 1.

It uses a public source assessment methodology (ACT) that has been developed in conjunction with industry46 to provide sector specific assessments of companies transition plans. This allows insurers, providers of capital and other stakeholders to have confidence that each transition plan has been consistently and rigorously assessed, and thus be able to manage their risk exposure in their own portfolios.

Companies from the power sector and other industries can gain valuable insight from the assessment process as to where they could improve their transition plans, and benefit from an independent assessment to help them in seeking finance and insurance for their businesses.

The accreditation is renewed on a yearly basis.

Increasing public concern and activism is driving the political will to find an orderly energy transition. Transparency will also be demanded by the financial institutions that provide the capital for the transformation. There is a growing call for regulators and the financial services sectors to act as stewards of the climate risk and hence to the energy transition47 48. These financial institutions are already under pressure to decarbonise their portfolios and support an orderly transition49.

Disclosure using the recommendations of the Task Force on Climate Related Financial Disclosures (TCFD) can provide transparency in this area to investors, providers of capital and insurance and society as a whole. Increasingly, the TCFD is being seen as a framework by regulators for climate disclosure: UK and New Zealand are explicitly bringing in the TCFD as mandatory, but it is also being considered by the EU, Japan, USA, Canada, Australia, Switzerland, France, Hong Kong and Singapore.

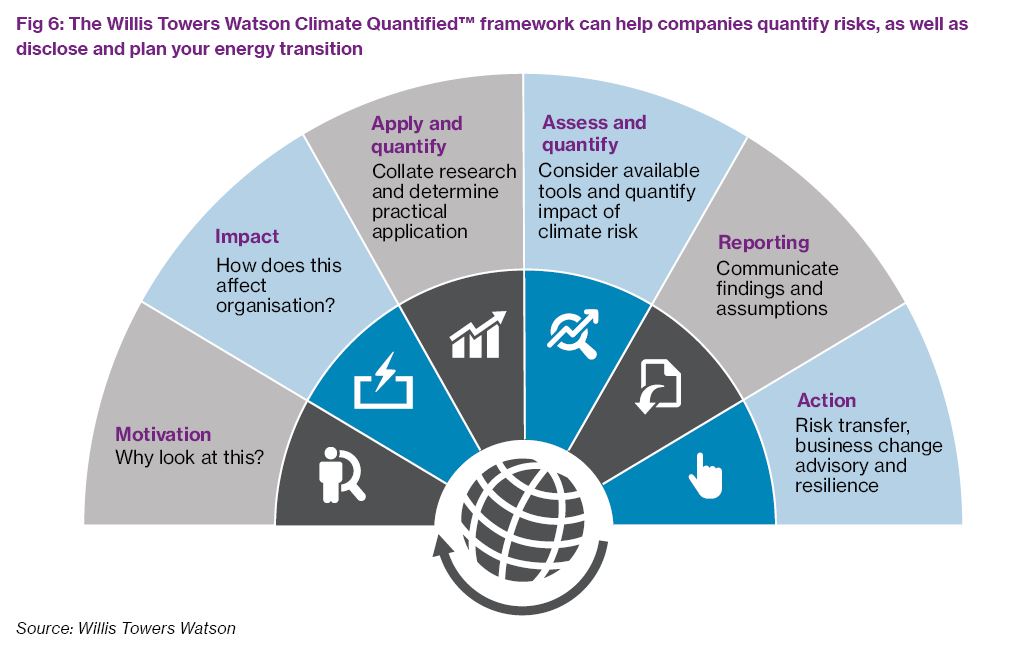

Power businesses, and the governments that rely and support them, will need to adopt a systematic approach to the energy transition challenge. At Willis Towers Watson, we take the following approach with our clients:

In order to plot a course through the transition, a map is needed. While none of us can profess to having a crystal ball, scenarios can be used to help navigate the risks and opportunities to each organisation in the new territory ahead. A range of publicly available scenarios have been completed for the energy and other extractive sectors that give an industry view, and these can form the basis of more tailored, site specific analysis.

These forward-looking assessments will be fundamental, as the past may not be reflective of what is to come; indeed, the pace of change over the last year has shown that there are some surprises ahead. The rate of net zero targets, the rapid decrease in renewables costs, together with the exclusion of financing and support services, has forced several withdrawals from fossil fuel projects. For instance, the Australian Utility firm AGL announced an AUD $2.7 billion loss in December 2020 due to rapid market changes (including “behind the meter” technologies such as home batteries and electric vehicles as well as falls in power prices)50. In Indonesia, no new coal-fired plants will now be approved51. Withdrawals of funding for fossil fuel generation may put several assets at risk of being stranded if abatement is not integrated.52

Given this, it is important to build scenarios that can help power companies show sensitivity to changes in the market and resiliency of their business models to such changes. New and existing fossil fuel assets need to measure over what timescale they will be profitable against these scenarios; adding the climate dimension can strengthen decision making here.

The first step in scenario analysis is to build scenarios that explore plausible emissions profiles. The NGFS has recommended using three key scenarios:

Shared Socio-economic Pathways (SSPs) are used to plot technology and market changes in the transition scenarios (1) and (2). The IPCC 1.5 special report53 highlighted four potential pathways (P1-P4) to illustrate use of various fuels and technologies in the energy mix, and the IEA has recently published a useful net zero pathway to 2050. This range of choice highlights that there are many technological and business model choices to achieve the overall greenhouse gas reductions needed. In making the choice, it is important to consider what the output of the analysis is needed for:

During our work with companies and governments, we have found the following examples of climate-related risk:

Acute (short term, localised extreme events) risks need sophisticated regional modelling over the lifespan of the assets.

A new additional concern for both energy companies and governments that may be pursued through the courts is the potential for “stranded liabilities”. This occurs where there are insufficient funds to properly retire assets to protect human health and the environment.56

Costs and budgets for transition, alongside policy, are also changing quickly – the IPCC will shortly release its latest 5-year update on climate (AR6)57, synthesising research from across the scientific world. Given that annual GHG emissions have not yet started to go down meaningfully, it is likely that this report will indicate the rate of decarbonisation needs to accelerate, rather than slow down.

Most scenario work though is focussed on smooth orderly transitions (e.g. a smooth transition of carbon pricing to ~$100 per tCO2e by 2030). The modelling of high impact, low likelihood risks (“Green swans”58) is important it enhances the disorderly modelling to include rapid changes in market and regulatory sentiments (e.g. sudden shift of carbon pricing in 2030 from ~$40tCO2e to $250tCO2e).

The good news is that risk managers can be proactive in addressing transition risks; furthermore, many industries are finding that the insurance sector is uniquely placed to help them, given its experience of being on the front-line of managing the impacts of a changing climate over many decades.

Risk, opportunity and scenario analyses are the cornerstone tools for creating a transition plan and being able to model this over the timeframes involved is at the heart of our Climate Quantified™ framework. We can help put scenarios together, identify and quantify the risks ahead, identifying cash flow changes, asset/equity values at risk and opportunities to maximise profitability during the transition.

The risk financial impact and likelihood work needs to be conducted on an asset level basis, with scenarios in detailed enough form to model likely changes in severity of physical climate impacts at enough granularity. Sectoral and regional transition pathway choices also need to take into account the speed of market, policy and technology changes.

Once scenarios and risks are plotted, asset level assessments of impacts and likelihoods need to be completed to understand the potential for the changing landscape to affect profitability. Risk managers are uniquely placed to ensure their companies are prepared to:

At the heart of this is achieving the balance of keeping to science aligned targets whilst achieving cost-effective transition by:

In assessing the climate risks and opportunities for a power company, it is likely that a cross-over for certain generation sites will take place. This potentially turns assets into liabilities (i.e. stranded assets59) as the cost of continued use of a high carbon asset is more than commissioning new low carbon power (usually a combination of storage with wind and/or solar generation)60.

New renewable energy as a source of power, and as a way of manufacturing green hydrogen, is expected to be cheaper than operating old fossil fuel plants globally by the end of the decade61, and levelized cost of electricity (LCOE) comparisons already have many renewable technologies operating at below the costs of conventional fossil fuels.62 Carbon capture and storage at fossil fuel generation assets needs much higher costs of carbon to be competitive.

The wave of pressure to close coal mines and generation plants is just starting to be felt for gas generation. It is now predictable that attention will continue to be focussed on coal-related and Arctic/Oil Sands production assets and will expand further to all fossil fuel-based assets in this decade.

Many of the common ways of achieving transition plans that have been proposed involve swapping out coal for high efficiency gas and/or introducing carbon capture and storage. This is often cited as being the most economical method. However, given the rapid changes in the costs of renewable energy and storage, this may not remain the case. The EU Sustainable Finance Taxonomy gives guidance for issuers of debt of what technologies are “sustainable” through its classification of technologies that “Do no significant harm” and “Contribute solutions”.63 There is also concern that a $1-4 trillion carbon investment bubble may burst in this decade.64

Developing an appropriate retirement and divestment plan is also key part of any transition plan. In the early part of the transition, divestment of assets may be financially feasible but, whilst improving the carbon balance sheet, might not deliver the emissions cuts at system levels. Already there has been some call for governments and industries to work together to create the energy equivalent of “bad banks” to retire high carbon assets.

But investment in renewables isn’t going to be a get out of jail free card. Value chain impacts will also need to be considered, as many of the rare earth elements that will grow in demand65 are currently being mined in regions where human rights and/or severe impacts to the health of local population and their surrounding environment66 67.

Having a climate strategy and transition plan needs to be delivered in the company. Like any strategy, there are a number of key areas which are important to a successful delivery:

Strategies and plans often fail because company cultures and staff values are not aligned with the goals. It is crucial to work with both HR, talent and reward functions to implement these plans.

Short and medium-term targets are also needed that align with the goal of getting to at least a 50% reduction in emissions by 2030. Incentive plans need to be focussed on achievement of the emissions reduction targets set. Willis Towers Watson’s recent survey has found that four in five companies plan to change their ESG measures in executive pay plans over the next 3 years.71 We work with companies globally to help them implement this.72

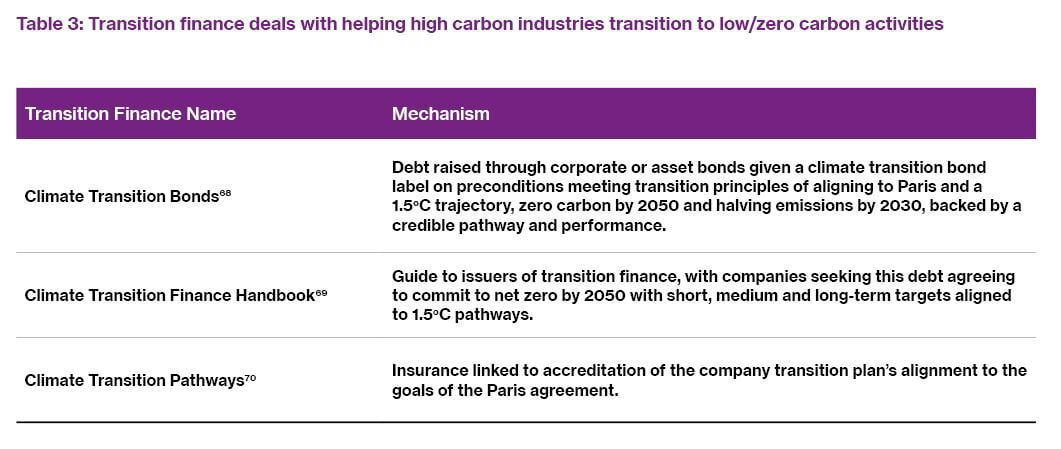

Sustainable and green finance has grown hugely in the last couple of years73, despite COVID-19, and is expected to exceed $1trillion in 2021 and possibly accelerate from there, with demand outstripping supply. However, many of these existing financial instruments focus on purely financing zero carbon or near-zero carbon activities. Exclusionary principles deployed in finance industries mean that many companies are finding rises in the cost of capital and/or difficulty in raising capital and insurance.

New transition finance instruments are being created to help companies that could reduce emissions significantly and are willing to action a transition strategy. Access to these debt instruments are subject to pre-conditions that their transition plans and performance align to the Paris Agreement.

Demonstrating that climate action is taking place, governed well, with a robust strategy and with performance measurements, is seen as key to meet conditions of investment, whether debt, insurance or equity. This is also an opportunity space, and one that the power sector has recognised with companies from the sector leading on disclosure in the 2020 TCFD Status report, with an average level of disclosure across the Task Force’s 11 recommended disclosures of 40%74. But it will need to accelerate.

Our team have been helping to define the climate-related metrics and reporting recommendations behind frameworks such as TCFD and CDP, the two pre-eminent disclosure frameworks for climate disclosure. One of the key components is transparency of process, progress and what is yet to be done. Benchmarking performance against peers and being able to learn from leaders in transition planning from across multiple industries is at the core of our research, helping you successfully use your disclosure for stakeholder engagement.

While there may be challenges ahead, the transitioning and adapting to climate change risks presents a strategic opportunity for risk professionals, particularly in the power sector. As Boards grapple with these issues, risk managers can play a leading role, providing not only risk quantification and analysis but also insight to inform strategy in a rapidly evolving risk landscape to secure organisational resilience.

Tony Rooke is Director of Climate Transition Risk in the Climate and Resilience Hub at Willis Towers Watson in London. Tony.Rooke@willistowerswatson.com

Lucy Stanbrough is Head of Emerging Risks research for the Willis Research Network at Willis Towers Watson in London. Lucy.Stanbrough@willistowerswatson.com

1 “Energy Market Review 2021”, April 2021, Willis Towers Watson. 2 IPCC, 2018: Global warming of 1.5°C. An IPCC Special Report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty [V. Masson-Delmotte, P. Zhai, H. O. Pörtner, D. Roberts, J. Skea, P.R. Shukla, A. Pirani, W. Moufouma-Okia, C. Péan, R. Pidcock, S. Connors, J. B. R. Matthews, Y. Chen, X. Zhou, M. I. Gomis, E. Lonnoy, T. Maycock, M. Tignor, T. Waterfield (eds.)]. 3 UNEP Emission Gap Report 2020, 9 Dec 2020 4 UNEP Emission Gap Report 2020, 9 Dec 2020 5 IEA Global Energy and CO2 emissions in 2020 6 Global Energy Review 2021, IEA April 2021 7 IEA – A global pathway to net-zero CO2 emissions in 2050, May 2021 8 Figures based on list of companies with targets approved by the Science Based Targets Initiative as being science based targets (SBTs) in the period June 2020 to May 2021 (downloaded 25th May 2021).

9 https://www.weforum.org/events/climate-breakthroughs-the-road-to-cop26-2021/sessions/taking-stock-of-the-race-to-zero 10 https://unfccc.int/climate-action/race-to-zero-campaign 11 https://www.blackrock.com/corporate/investor-relations/larry-fink-ceo-letter 12 “Energy Market Review 2021”, April 2021, Willis Towers Watson 13 https://www.ceres.org/news-center/press-releases/historic-votes-shareholders-demand-strong-climate-action-us-oil-and-gas 14 https://www.reuters.com/business/sustainable-business/shareholder-activism-reaches-milestone-exxon-board-vote-nears-end-2021-05-26/ 15 https://www.bloomberg.com/news/articles/2021-05-26/shell-loses-climate-case-that-may-set-precedent-for-oil-industry 16 http://climatecasechart.com/climate-change-litigation/about/ 17 “Global Update: Climate Summit Momentum”, Climate Action Tracker, May 2021 18 European Green Deal, EC, Dec 2019 19 White House, “Fact Sheet: President Biden sets 2030 Greenhouse Gas Pollution Reduction Target”, April 2021

20 White House, “Fact Sheet: Expansion and Modernisation of the Power Grid”, April 2021. 21 TCFD Recommendations, Financial Stability Board’s Task-Force on Climate-related Financial Disclosures, June 2017 22 Bankers for Net zero, Volans and UK banks 23 https://www.climatebonds.net/transition-finance/fin-credible-transitions 24 https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/climate-transition-finance-handbook/ 25 Net zero Banking Alliance 26 Expected to launch at COP26 including AXA, Allianz, Aviva, Munich Re, SCOR, Swiss Re and Zurich Insurance Group 27 Investor initiative CA100+ to ensure world’s largest greenhouse gas emitters take necessary action on climate change 28 UNEP-FI & PRI, Net zero asset owners alliance 29 Net zero Asset Managers Alliance 30 https://www.sayonclimate.org/ 31 https://www.climatetransitionpathways.com/ 32 Coalition for Climate Resilient Investment (CCRI) 33 UNFCCC Race to Zero Campaign

34 GFANZ – an alliance of financial net zero alliances. 35 https://sciencebasedtargets.org/business-ambition-for-1-5c 36 SBTi Power Sector 1.5C Guidance, Science Based Targets Initiative, June 2020 37 IEA – A global pathway to net zero CO2 emissions in 2050, May 2021 38 Greenhouse Gas Emissions by Countries and Sectors, WRI, Feb 2020 39 "Beyond petrostates", Carbon Tracker Initiative, Feb 2021 40 The Economist, Sept 2020 41 https://www.rethinkx.com/energy 42 “Renewables 2021 Market Review”, Willis Towers Watson, Jan 2021 43 Climate Transition Pathways 44 Investor initiative CA100+ to ensure world’s largest greenhouse gas emitters take necessary action on climate change 45 https://www.sayonclimate.org/ 46 https://actinitiative.org/ 47 “Managing Climate Risk in the U.S. Financial System”, US Commodity Futures Trading Commission, Sept 2020

48 “A call for action – Climate change as a source of financial risk”, NGFS, April 2019 49 Whitehouse Briefing: Executive Order on Climate-related Financial Risk, May 2021 50 Renew Economy and Sydney Morning Herald Feb 2021 51 Bloomberg, May 2021 52 Bloomberg, May 2021 53 https://www.ipcc.ch/sr15/ 54 “Understanding the impact of a low carbon transition on Uganda’s planned oil economy”, (as Climate Policy Initiative Energy Finance team) Dec 2020 55 "Beyond petrostates" Carbon Tracker Initiative, Feb 2021 56 “The Flip Side: stranded assets and stranded liabilities”, Carbon Tracker Initiative, Feb 2020 57 International Panel on Climate Change, AR6 released in stages over 2021 and 2022 58 Green Swans, Volans 59 “Stranded assets: a climate risk challenge”, B Caldecott, E Harnett, T Cojoianu, I Kok and A Pfeiffer, IADB, 2016 60 E.g. “Duke IRPs focus on new gas-fired generation creating serious stranded-asset risks”, IIEFA US, Jan 2021 61 "Coal-developers-risk-600-billion-as-renewables-outcompete-worldwide", Carbon Tracker Initiative, Mar 2020

62 Projected costs of generating electricity 2020, IEA and OECD 63 EU Sustainable Finance Taxonomy, EC. 64 “Toward Risk-Opportunity Assessment in Climate-Friendly Finance, JF Mercure, 2019 65 "European Commission, Critical materials for strategic technologies and sectors in the EU - a foresight study, 2020" 66 Mining and Bio-diversity, CDP briefing, 2020 67 “Responsible or reckless? A critical review of the environmental and climate assessments of mineral supply chains“, Jordy Lee et al 2020 Environ. Res. Lett. 15 103009 68 “Financing Credible Transitions”, Climate Bonds Initiative & Credit Suisse, Sept 2020 69 Climate Transition Finance Handbook, guide for issuers, International Capital Market Association, Dec 2020 70 Climate Transition Pathways – TBC in Q1. 71 ESG and executive pay survey, Willis Towers Watson, Dec 2020 72 Executive Compensation, Human Capital Governance and ESG, Willis Towers Watson. 73 “Debt engineers tackle climate change with bonds to rewild land”, Bloomberg, Feb 2021 74 2020 TCFD Status report