London

On the face of it, it might be argued that life in the London-based Power insurance market is carrying on in much the same way as it has done for many years. The glut of reinsurance market capital, referred to so often in our publications as the principal driver of soft market conditions, shows precious little sign of being withdrawn to be deployed elsewhere. As a result, reinsurance prices have remained low by historical standards, allowing direct insurers to compete more aggressively and fuelling the softening market conditions that we have experienced for the last ten years or so.

But as we have argued for some time now, logic dictates that this continual market softening has to break down eventually; at some stage, premium income levels become so low that it is just not worth underwriting a given portfolio anymore and loss ratios start to become unsustainable. In the past, we have been unable to say exactly when that point would be reached; only that further softening was showing that it had not been reached yet.

Is now the time? To answer that, let’s have a look at some external factors which are influencing conditions in the London Power market.

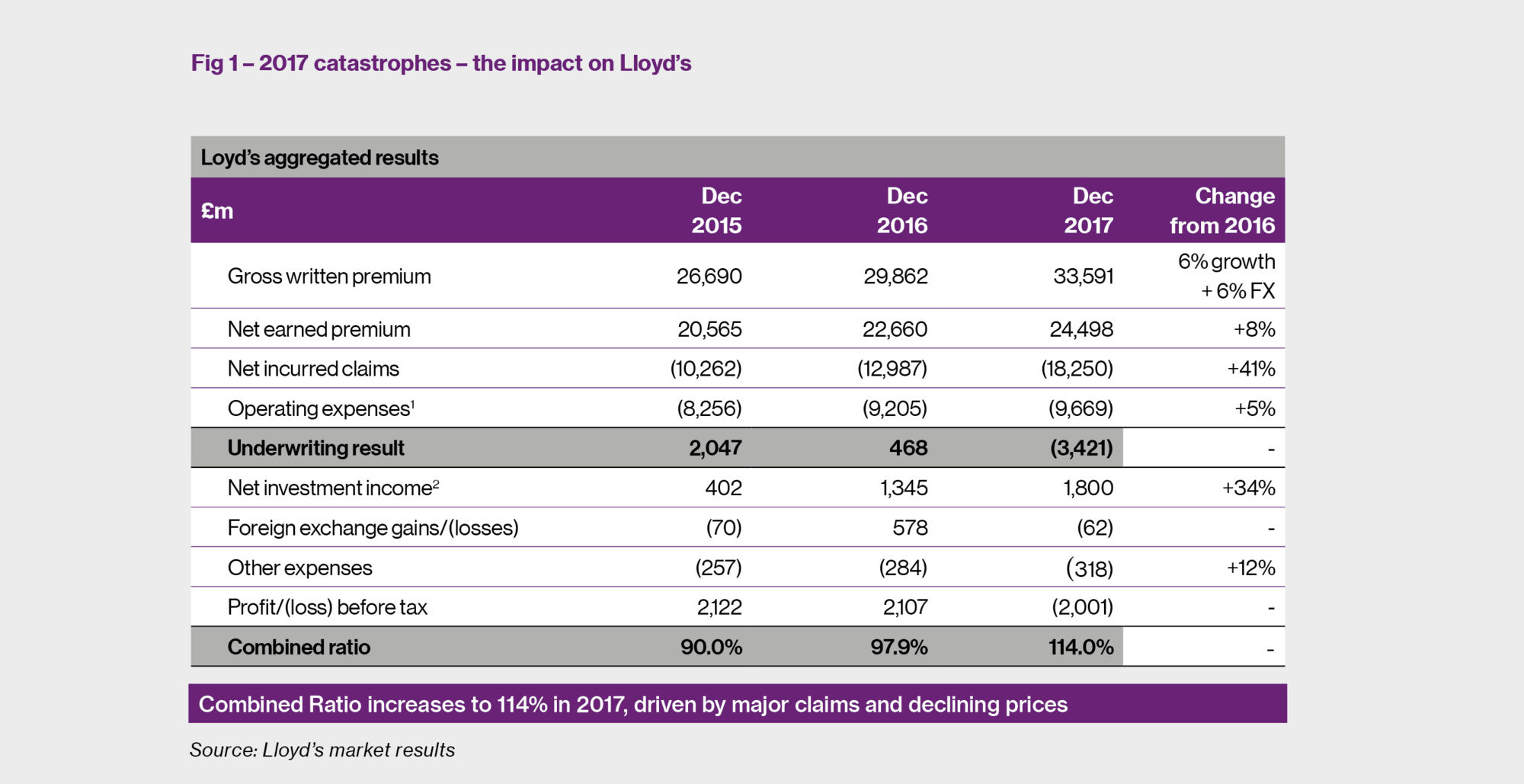

The Lloyd’s PMD initiative While Lloyd’s is by no means the only market underwriting Power, it is an important market for this sector. The widely reported prevailing circumstances at Lloyd’s are therefore a useful place to start while we seek to develop the picture in terms of the challenges faced by global markets at the moment. Under the leadership of John Hancock, the Lloyd’s Performance Management Directive (PMD) put in place a process designed to bring significantly more rigour to the examination of individual syndicate business plans, following the overall underwriting loss made by the Corporation in 2017 (see Figure 1 overleaf). Syndicates which had made underwriting losses in each of the last three years received special attention. Power was one of seven underperforming classes of business identified in a market-wide analysis of Lloyd’s underwriting performance (the others being International Property Direct & Facultative; Overseas Motor; Marine Hull; Cargo; Yacht; and Protection & Indemnity).

Of the 95 Lloyd’s syndicates that presented business plans for 2019, two did not make the grade and have been put into an orderly run-off, 11 syndicates have approval to write more business in 2019 than they did in 2018, and all other business plans were approved, after thorough scrutiny and some refinement. The expected overall premium volume is likely to be down around 5% in 2019 over 2018, bringing it back to the 2017 premium volume of US$42.5bn.

Although it is not our place to comment directly on this process, it seems quite clear that this development is likely to put a break on individual syndicates’ ability to compete in the market by driving down prices in order to achieve increased premium income streams. Given that power was one of the seven identified underperforming classes, we can expect this effect to be felt in the power insurance sector.

Unprofitability of other lines of business

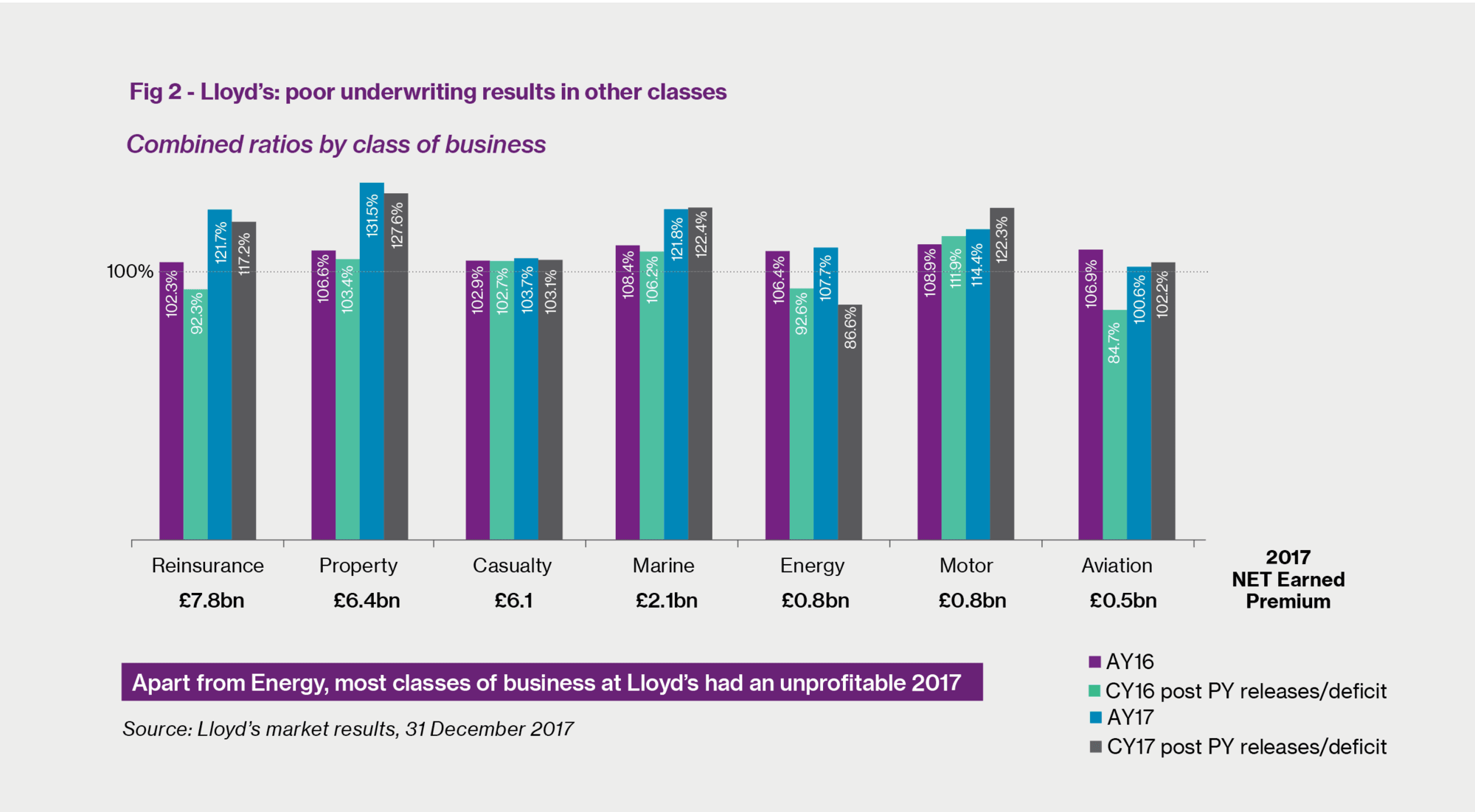

As if this new degree of management scrutiny was not enough to change market dynamics, individual underwriting teams are also being forced onto the back foot by the results of other lines of business closely associated with their own portfolio (see Figure 2 above). Classes of business associated with power, such as Construction, Mining and Downstream Energy, have also been reporting negative underwriting results. The Insurance Insider reported in October that downstream property losses were estimated at US$2.3bn for the year to date, far in excess of the premium pool of around US$1.5bn, as a result of which underwriters in this segment of the market were reported to be seeking double-digit rate rises in 2019.1

Insurance company management pressures In a truly competitive market, it might be thought that if one sector was being forced to pull back from competing at full throttle then another would be able to take full advantage. However, any notion that the company market might differentiate itself by continuing to offer increasingly competitive terms to buyers this year is almost certainly misplaced. If anything the major company market – including the likes of AIG, Swiss Re, Allianz, Munich and Chubb – have been hit more severely by last year’s natural catastrophes and it is understood that their underwriters are under a similar pressure from senior management to scale back on premium income expansion and ensure that they “hold the line” on rating levels and other terms and conditions.

When Swiss Re announced its Q3 results it said that its “cumulative losses for the first nine months are broadly in line with year-to-date expectations”.2 This might suggest that 2018 was on course to be an average year for catastrophe losses.

However, Swiss Re commented that its Q3 losses were high for a single quarter. And Q4 will also be an above-average quarter for insured catastrophe losses, with the Californian wildfires and Hurricane Michael pushing the bill for the quarter towards US$30bn.3 Sure enough, Swiss Re reported in December that global insured catastrophe losses in 2018 were estimated to reach US$79bn, higher than the annual average of the previous decade of US$71bn.4

Speaking at the Baden-Baden reinsurance meeting (21-25 October 2018), a Munich Re executive observed that, given the overcapacity in the market, 2018’s losses alone were not expected to increase rates at the 1 January renewals – although it should be noted that at the time this comment was made November’s Camp Fire, the most destructive fire in Californian history5, had not yet occurred. But they added that “underwriting discipline and the need for an adequate return on equity could have an upward impact on prices. The necessity and urgency to be disciplined in underwriting is increasing”.6

Turning away from natural catastrophe losses and to the ‘risk’ experience in the Power sector, it would be reasonable to infer that if Lloyd’s regards Power as an underperforming class then the company market will probably take a similar view. We have commented in previous Power Market Reviews on the continuing ‘attritional’ Machinery Breakdown and other losses typical of the power sector, which have severely challenged insurers’ efforts to make their books profitable on a sustainable basis.

Result – a change of underwriting mood

As a result, we are seeing a change of mood amongst underwriters in virtually every line of business and geography. In very general terms, no longer is their overriding requirement meeting ambitious premium income targets; instead, the focus has generally switched to underwriting profitability. From our conversations in the market it seems that some underwriters are not far away from seeing their own positions coming under threat if they continue to ignore the underwriting criteria laid out by their management.

So although the overall theoretical capacity levels remain at record levels, brokers are finding it much more challenging to deliver the results that buyers have enjoyed now for so many years.

Result: a market turnaround is now a fact, not just an assertion The Power market place has been a challenging environment for a number of years, due to the prolonged downward pressure on rates coupled with the annual losses equalling or surpassing the premium available for the class. The downward pressure has been in main due to the abundance of global capacity, coupled with the strength of offering regionally and internationally. The market had started to reach its breaking point towards the back end of 2016. Although reductions were still the starting point, they were mostly limited to single digit reductions compared to the wider Property market having double digit reductions.

The catastrophe events in the last quarter of 2017 saw the norm for renewals move from single digit rate reductions to flat rate as a starting point, with expectations the treaty renewals would further impact rate expectations going into 2018. Although the catastrophe events did not have the impact on treaty renewals that had been widely expected, the starting point has remained at flat rate renewals for non-loss making, low cat exposed territories.

Looking ahead to 2019 – five key dynamics

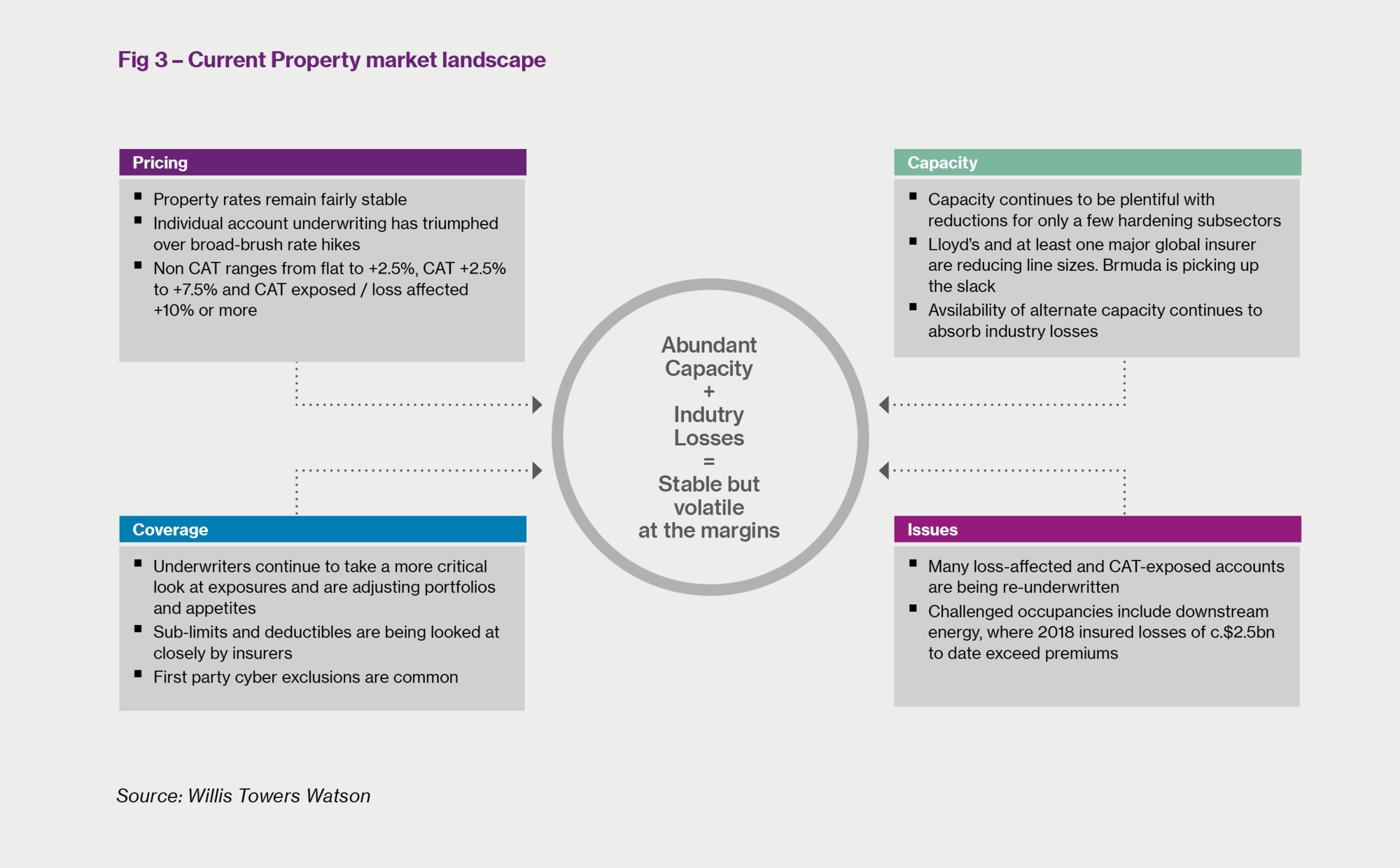

Figure 3 above provides an overview of a market that is no longer soft, but is still characterised by plentiful levels of capacity for most risks. Going into 2019, there are five key market dynamics that continue to influence risk pricing for the sector that we touch on below:

Carlos Wilkinson is Head of Power at Willis Towers Watson in London.

Ed Cooper is an Executive Director at Willis Towers Watson in London.

Despite initial speculation that the market would harden at the start of the year, rate increases failed to materialise during the first half of 2018 as flat premiums became the norm for renewals in the absence of significant losses or meaningful changes to the risk exposure. Consequently, in the context of the overall renewal process risk adjusted premium increases could more often than not be consumed within the recent negotiation.

However as we approach the closing stages of the year we are witnessing a palpable shift in market conditions, with insurers now working under a mandate to obtain rate increases across their portfolios. In the main, underwriters are achieving this by targeting distressed and highly exposed accounts for significant rate increases; however, most recently insurers have demonstrated an intention to raise rates across the board, regardless of whether an account is performing well or not.

Corporate governance A key contributing factor for this shift in market dynamics is the greater focus from Lloyd’s on insurer profitability. Lloyd’s’ desire to arrest declining loss ratios by requiring syndicates to return unprofitable elements of their business to profitability (in conjunction with the ‘Decile 10’ initiative) has forced an unquestionable reaction from the market. As a result, technical pricing adequacy is very much under the spotlight and invariably rates are moving in a single, upwards, direction.

Capacity developments: a contraction on the horizon? In tandem with applying upward pressure on rates, the greater regulatory scrutiny may also begin to play a part in restricting available capacity in the market. Whilst at present the total global Liability capacity remains relatively stable, total capacity in the market may begin to contract as we enter into 2019 and beyond. However such a contraction is unlikely to be consistent across the globe as certain regional markets such as Asia reap the rewards of more profitable underwriting performances. Nonetheless, the expertise and experience of the London market, especially amongst more complex sectors such as Power, remain paramount drivers for London retaining its value and attraction as a global insurance market.

Concurrently, whilst the position is by no means universal, the number of insurers exiting the coal sector is increasing and power companies purchasing high limits who are either solely or heavily involved in coal operations will be unable to avoid the effects of this capacity supply dropping out of the market.

Insurer retentions results in greater aggregation control Reinsurance treaties have also played a part in influencing underwriter appetite. Increased insurer retentions have resulted in greater aggregation control and a reduction in the willingness for insurers to deploy large primary lines. Nevertheless at US$ 3.3bn there still remains ample capacity in the market for even the most significant of limits and programmes with more modest levels of indemnity continue to benefit from the healthy competition produced by the capacity available. If the circumstances allow for it, this surplus capacity can be used by brokers to restructure clients’ insurance programmes to generate economic efficiency savings.

Consistent coverage In terms of coverage, market conditions have remained largely consistent, except for an increasing pressure from insurers to exclude cyber liability from General Liability programmes. Common extensions such as Electromagnetic Fields (EMF) and Unmanned Aerial Vehicles (UAV) clauses continue to be accepted on a standard basis and Pure Financial Loss Failure to Supply extensions remain available, subject to meaningful additional premium and exposure information.

Riding the wave Amongst all of this change and uncertainty, buyers are treading unchartered waters in terms of what this means for their insurance programmes. As a result, it is more important than ever that clients ensure that they not only nurture and build their longstanding relationships with markets, but that they also appoint a broker capable of assisting them ride the wave of market developments. Equipped with comprehensive underwriting information, a coherent marketing strategy and enough time to engage with insurers early, credible and experienced brokers should still be capable of arbitraging market relationships in order obtain successful results for their clients, albeit more likely in the form of structure and coverage improvements than rate discounts.

Matt Clissitt is an Executive Director at Willis Towers Watson in London.

Introduction – is a hard market for the Power Construction round the corner? The recent high profile hydro claims continue to dominate the Power Construction insurance market. Rate reductions are tapering off as markets are pushing for price increases; insurers are also becoming more selective over offering the wider coverages obtained within the broader broker wordings when being presented with a new large scale power project. Natural catastrophe events are likely to further this decline and we are seeing some individual rate increases in exposed locations.

Within the last twelve months several recognised Power Construction insurers have closed or diluted their construction underwriting accounts; these markets include Beazley, Talbot, Hardy, MS Amlin and Tokio Marine Kiln. This has resulted in a reduction in combined capacity of circa US$ 325m from the Power Construction market and further rumours circulate that other insurers are to follow suit. However, capacity is still plentiful and the appetite to underwrite new power projects is still strong.

New gas turbine technology – some teething problems

The evolution of gas turbine technology appears to be showing no signs of slowing down, with the introduction of newer and more efficient machines many of which are now (or are close to) coming out of final validation and achieving a full first year’s commercial operations.

However, as evidenced in some of the recent announcements, not all new models have achieved this milestone without some signs of initial teething problems which Original Equipment Manufacturers are now working hard to rectify, not just for all existing plants already under construction or now in operation but also those currently on order.

With virtually the full range of existing and more established models also undergoing continued enhancement, it is not easy for insurers to keep track of what unit is being presented to them when looking at a new risk for the first time. An early clarification of this and the other key features of the plant can only assist the broker when making his first approach to insurers.

Minimum deductible thresholds

With bigger machines potentially meaning a higher replacement value, insurers are keen to maintain a minimum threshold when it comes to the level of deductibles to be applied to large frame gas turbine and generator sets whilst at the same time seeking reassurance on the robustness of the Original Equipment Manufacturer warranty they expect to be in place. Insurers historically have been reluctant to assume the risk of design and manufacturing of such new and enhanced machines and will where possible continue to limit the scope of the cover they provide to what they perceive to be the “construction” risk when covering such projects. It is unlikely they will change this approach as the new and cutting edge technology continues to be rolled out.

IGCC resurgence as coal maintains its profile Although coal continues to lose pace to gas in some parts of the world due to continued environmental concerns and pricing exposures (in particular in the US with the “fracking” and “shale gas” boom providing an abundance of gas supply) it is still a major if not dominating fuel for power in some parts of the world. Furthermore, a small but apparently growing resurgence in Integrated Gasification Combined Cycle (IGCC) assets, with new demonstration plants coming on line around the globe promoting the case for further clean coal research and development, adds fuel to the argument that coal can still be viewed as a growing factor in the overall generation mix.

Boiler design an insurer focus

Continued development in super and ultra-super critical boiler design using higher temperatures and pressures with the resulting need for newer and more exotic materials to be used in certain boiler sections remains a key area of focus for insurers. Some high profile losses at units using some of these materials has only increased the concern insurers and their engineers have and so design and composite make-up of the boiler continues to be at the forefront of insurers minds when presented with a new coal fired project.

QA/QC critical

When considering a new risk (gas or coal fired) insurers will also want to see evidence of a robust and comprehensive QA/QC programme, including a focus on Positive Materials Identification (PMI) and a detailed understanding of the planned inspection programme for the project, including details of the Owner Engineer’s role in the QA/QC process.

New hydroelectric plants pose increased nat cat risk

Hydraulic energy accounts for a very significant percentage of the world’s electricity produced from renewable sources. As demand for hydro projects grows, the need to find land suitably sited to build dams becomes more challenging in order to minimise disruption to the indigenous populations and also so as to not disrupt the water demands of local agriculture.

Consequently, hydroelectric dam projects are increasingly being developed in ever more remote locations. Due to the nature of these projects these locations are often in areas that have an increased natural catastrophe exposure and/or are being considered for fluvial water courses that have very large variations in seasonal river flow that can create significant challenges during construction.

Tunnel coverage restrictions

It’s is often the case that hydroelectric plants will have large diameter tunnels constructed as part of the project. Depending on rock type and the degree of fracturing and faulting, these water transfer tunnels are often constructed by drill and blast. Regardless of the method of tunnelling proposed for the project, underwriters will seek to restrict insurance cover for loss/damage to tunnels under construction either to a percentage of the original linear construction cost (usually 150%) or a monetary limit of liability but less than the total value of the entire tunnel construction value. This is because the cost of repair and rectification of failed tunnels can sometimes significantly exceed the original construction cost due to issues related to access and also the associated cost of reinstating ground and/or profile around the original tunnel alignment.

Conclusion

The power generation industry has thrown up many challenges to the construction insurance market over the last 25 years, particularly as power generation technologies strive to keep pace with increasing demand for reliable power supply. The recent major losses in the hydro sector continue to be measured for potential impact on the way insurers evaluate similar projects in the future. New and more efficient gas turbine technology and boiler designs will be closely reviewed by specialist power markets as new projects are operated on a commercial basis.

David Forster is a Divisional Director at Willis Towers Watson in London.

Capacity stabilises Over the last few years, the capacity for Property Terrorism has remained fairly stable at around US$ 4.5 billion, after years of dramatic growth. During that time, the market capacity for the sub-perils of Political Violence and Terrorism Liability has steadily grown to around US$ 1.9 billion and US$ 1.7 billion respectively, whilst NCBR (nuclear, chemical, biological and radiological) terrorism and “cyber physical damage” terrorism capacity have grown quite rapidly in the last two years to around US$ 600 million and US$ 1.3 billion respectively.7

Little fall-out from Lloyd’s initiatives Whilst the market is predominantly Lloyd’s based, the performance reviews and extra scrutiny of business plans being undertaken by Lloyd’s at present are not expected to have major impact on market capacity over the next year - only two syndicates with terrorism market capacity (The Standard 1884 and Advent 780 due to their integration into Brit 2987) have entered run-off. Some syndicates are closing their Marine or Property lines where they might have previously purchased combined treaty cover, but the impact is expected to be minimal due to most being able to move this Terrorism treaty cover into an alternative combined treaty programme with another line. Furthermore, whilst they are reducing line sizes in other classes, AIG’s Terrorism capacity is not expected to reduce dramatically in 2019. However, as they continue to tighten underwriting principles there is some expectation that their capacity will not be as easily available on longer term deals or on more challenging risks.

Overall, it is therefore expected that the Terrorism market capacity across all sub-perils may see some flattening and stabilisation; there is potentially for some decrease in overall capacity but this is not expected to have any major impact on supply against general buyer demand.

Pricing: no dramatic changes anticipated In line with the minimal impact expected from the Lloyd’s and AIG performance reviews on capacity, pricing and rating is not expected to see any dramatic change either through 2019. Since the heavy natural catastrophe season of 2017, pricing has mostly flattened and this is expected to continue. Reductions are still possible in certain cases, but generally only up to around 5%, and in countries or regions where the security situation is deteriorating, rates are increasing in line with heightened risk.

Losses – attritional rather than catastrophic In recent years the world has seen thousands of Terrorism and Political Violence events globally, but the majority of attacks against the power industry have mostly been seen in the Middle East, Africa and Central Asia, where the legacies of ongoing conflict perpetuate themselves. Whilst Europe and North America has seen an increase in attacks in recent years, along with the foiling of numerous planned attacks against the power industry, the majority of actual attacks have mostly been in city centres and have targeted mass casualties rather than infrastructure.

The Terrorism and Political Violence market has continued to pay a number of losses to the power industry; however, the majority of these are small and/or attritional rather than catastrophic. While these losses continue to be paid and may have some impact on renewals for those particular affected insurance buyers, this is not expected to have any major impact on general market capacity or pricing any further than the changes otherwise caused by any shift in the security environment in those regions.

Lyall Horner is Senior Associate, Financial Solutions at Willis Towers Watson in London.

1 https://www.insuranceinsider.com/articles/122529/downstream-market-looks-for-double-digit-rate-rises-in-2019 2 “Swiss Re pegs Q3 cat and large losses at $1.4bn” - Insurance Insider, October 18 2018 3 https://insuranceday.maritimeintelligence.informa.com/ID1124715/Industry-Q4-cat-bill-edges-towards-$30bn-as-loss-estimates-mount 4 https://www.reinsurancene.ws/cat-losses-returned-to-normal-levels-over-2018-peel-hunt/ 5 http://time.com/5470154/camp-fire-human-remains/ 6 “Reinsurers push for flat property cat renewal at Baden-Baden” - Insurance Insider, October 25 2018 7 Source: Willis Towers Watson