Previous Quarterly Editions

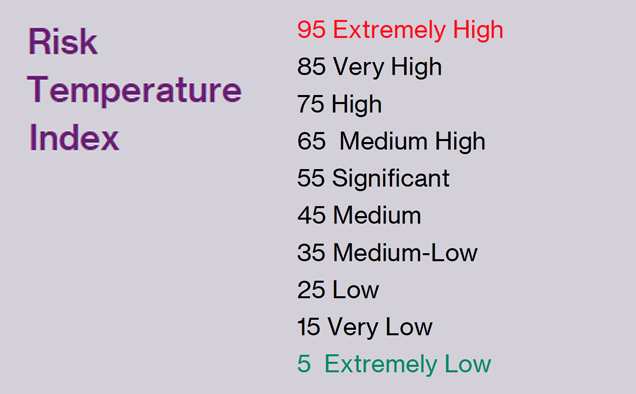

Expropriation Risk: 39 39 41 41 ► Political Violence Risk: 48 48 48 48 ► Terrorism Risk: 50 50 50 50 ► Exchange Transfer and Trade Sanction Risk: 55 64 64 64 ► Sovereign Default Risk: 57 57 57 57 ►

TREND ►

Moroccan authorities’ increasingly abrasive foreign policy has led to rising political tensions with neighbours Algeria and Spain. The risk of the Algeria dispute leading to armed conflict is low, but escalation is possible. There are no vital interests at stake, although the loss of Algerian gas would inconvenience Morocco. The main issue underlying the dispute is Algeria’s aspiration to claw back prestige after having been eclipsed by Morocco’s growth as a regional economic and diplomatic force. If there is a military escalation, it would be likely to start with an increase in violence in the Western Sahara.

Morocco currently consumes about 1 billion cubic metres (bcm) per year of natural gas, all sourced from Algeria, but this is only 3.4% of its total primary energy consumption and could be covered by extra coal consumption. Morocco has abandoned plans for a fixed liquefied natural gas import terminal in favour of the quicker, more flexible floating storage and regasification unit (FSRU). The government is considering a bid from Predator Oil and Gas Holdings to supply the first FSRU. SDX, a Predator subsidiary, also holds a natural gas concession in Guerif, central Morocco, where reserves of about 13bcm have been identified.

Domestically, Moroccan authorities’ main concern is the new COVID-19 wave that began in July with the Delta variant’s rapid spread. This has diminished Morocco’s early success in vaccine roll-out. By late August, 31 million vaccine doses had been administered and 13.6 million people, more than one-third of the 37 million population, had been fully vaccinated. The new surge has prompted renewed curfews and set back revival prospects for tourism.

Despite the COVID-19 wave, elections for the lower house of parliament, regional assemblies and municipalities went ahead on September 8. The Justice and Development Party (PJD), an Islamist party that had been the largest in parliament since 2011, saw heavy losses. The winners were centre-right parties with close ties to the palace. The PJD has been under pressure for some time, following the replacement of its charismatic former leader, Abdelilah Benkirane, in 2017. The royalist parties have benefited from King Mohammed’s resolute COVID-19 response.

The PJD won only 13 of the lower parliament house’s 395 seats, compared with 125 in 2016 and 107 in 2011, and suffered similarly dismal regional and municipal elections results. The winner was the National Rally of Independents (RNI), led by Aziz Akhannouch, a wealthy businessman and agriculture minister since 2011. His party secured 102 seats, compared with 37 in 2016.

The Party of Authenticity and Modernity (PAM), founded by associates of the king to foil the PJD, won 87 seats, down from 102 in 2016. The centre-right Istiqlal party increased its tally to 81 from 46, benefiting from its new leader Nizar Baraka (a former economy minister) and effective campaigning. Turnout was 50.4%, up from 43% in 2016.

Akhannouch is the new prime minister, and his government will be based on an RNI-PAM-Istilal coalition, which will have a comfortable majority of just over two-thirds of the lower house’s seats. An electoral rules change to calculate seat allocation based on total registered voters, rather than votes cast, had been expected to produce a less clear-cut result. It was also thought that turnout would fall, owing to voters’ political disaffection and COVID-19.

The new administration will formalise the policymaking alignment between the palace and the government. This should yield more effective policy management but will mean the king will no longer be able to deflect blame for unpopular policies and events onto the PJD. With the PJD’s collapse, the attraction of more radical strains of Islamist politics could also grow. However, on balance, the election has been positive for Morocco’s political risk profile.

Morocco’s economy was battered by COVID-19’s impact in 2020, and by the effects of meagre winter rainfall on agriculture, which accounts for about 12% of gross domestic product (GDP) and almost one-third of the labour force.

Real GDP contracted by 6.3% in 2020, but has strongly recovered during 2021, including year-on-year growth of 12% in the second quarter, given a much-improved harvest and strong exports recovery. The economy is likely to grow about 6% in 2021, before reverting to 3-4% growth.

Morocco’s external financial position actually improved in 2020, despite tourism income losses. COVID-19 did not seriously affect phosphate and agricultural produce exports, for instance, and automotive sales recovered in the second half. Import costs fell because of lower oil prices. Remittances also helped reduce the current account deficit. This pattern has continued in 2021, except for a rise in oil import costs. In the first half of the year, exports rose by 24% year on year, and remittance flows increased by almost 50%, while tourism income fell by 70%.

The government’s domestic finances were hit hard in 2020; the fiscal deficit doubled to about 7.5% of GDP. The economic stresses were also reflected in the banking sector, as the stock of non-performing loans rose by about 15% in 2020, and the ratio of non-performing loans to total loans rose to 8.6% from 7.6%.

Morocco has successfully courted foreign investment for years, including incentives such as preferential taxes and special investment zones. Foreign investors are typically induced to establish partnerships with interests connected to the palace. There are no restrictions on companies divesting and selling their stakes to third parties. Businesses can run into difficulties during periods of political tension between their home government and Morocco, usually over the Western Sahara sovereignty controversy. However, disputes that have arisen between the Moroccan authorities and foreign investors have tended to be based on commercial rather than political issues.

Western Sahara is the main source of political violence. Tensions have risen including as Morocco has increased its diplomatic efforts to resolve the issue in its favour and deployed troops within a buffer zone along the Mauritania border. Also problematic was a deal struck in December 2020 by the Trump administration to recognise Morocco’s claims over Western Sahara in exchange for Morocco establishing diplomatic relations with Israel.

Within Morocco, there have been sporadic popular protests against corruption, police brutality and deprivation. Disaffection continues to bubble in Morocco’s large informal sector. The authorities’ fears of destabilising protests are reflected in a highly oppressive system of surveillance and tight media controls.

Morocco was one of the main sources in North Africa of fighters that joined Islamic State (IS) in Syria in 2013-17. An estimated 3,000 Moroccans joined IS, most coming from areas in the north known for Islamist militancy. There have been concerns that many of these fighters would return to Morocco and become involved in terrorist activity. However, there have been only a handful instances of Islamist terrorism in Morocco since Al-Qaeda carried out a major assault in 2003 and the risk of terrorism remains low. This is partly because of setbacks for IS and Al-Qaeda but also effective Moroccan intelligence services.

There are no significant restrictions on exchange transfers in Morocco. Access to foreign exchange through the banking system is straightforward, although the central bank does maintain some capital controls.

The exchange rate is pegged to a basket weighted 60% to the euro and 40% to the US dollar. The band within which the rate may fluctuate was widened to 2.5% in 2018, and to 5% in March 2020, as part of the COVID-19 response. The International Monetary Fund repeatedly urges Morocco to shift to a more flexible system. The central bank has agreed in principle, but there appears to be a residual reluctance to give up control.

The risk of trade sanctions applies mainly to goods exported from Western Sahara. The European Court of Justice is involved in prolonged deliberations over a Polisario suit against the European Union, including exports from the territory and its waters in its trade preference accords. Morocco in October 2020 imposed various restrictions and tariffs on goods imported from Turkey, claiming that Turkish exporters had abused concessions provided under a 2016 free trade agreement.

Morocco’s debt has increased due to COVID-19, but is not particularly burdensome by regional standards, and the risk of sovereign default is low thanks to historically high reserves. Gross public debt has risen to 76% of GDP, from about 65% in recent years, while external debt has climbed from about 32% of GDP to 40%.

In March 2020, the government drew down the entire USD3bn available from the IMF’s precautionary and liquidity line (PLL), given COVID-19. The government issued EUR1bn (USD1.2bn) in Eurobonds in September, followed by a successful USD3bn bond issue in December. This has brought Morocco’s stock of sovereign bonds to about USD12bn. The government used part of the proceeds of the most recent bond issue to repurchase about one-third of the PLL. Meanwhile foreign exchange reserves stand at about USD34bn, sufficient to cover nine months of imports.

Return to contents Next Chapter