Previous Quarterly Editions

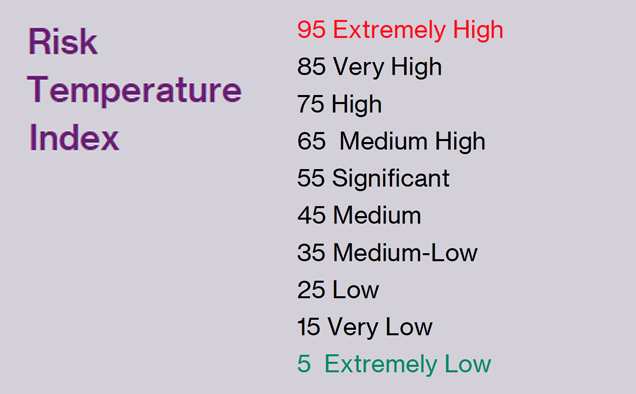

Expropriation Risk: 46 46 52 52 ► Political Violence Risk: 51 51 57 57 ► Terrorism Risk: 68 69 69 69 ► Exchange Transfer and Trade Sanction Risk: 35 35 35 35 ► Sovereign Default Risk: 57 57 57 57 ►

TREND ►

After peaking at more than 400,000 cases in early May, the second wave of COVID-19 infections in India has been in slow retreat with the seven-day average at around 32,000 cases on August 23. However, a high level of cases in some states, especially Kerala, indicates that the pandemic still lurks. The government is preparing for a potential third wave, though with high seropositivity levels in many parts of the country, around 11% of the population fully vaccinated and 37% having received at least one dose, a future wave is expected to be less severe.

With lockdowns and restrictions imposed in many parts of the country during April-May being relaxed after being kept in place for long periods, economic activity has begun to revive. Automobile sales have regained their levels of a year ago and freight carried by the Indian Railways rose by 18.4% in July year-on-year.

Yet there are some areas of concern. The south-west monsoon that provides 70% of India’s annual rainfall and is normally active in June-September has been weak this year. A record poor level of rainfall in August -- with a 28% deficit that is the worst since records have been kept, and low levels in July -- has meant that over its most active phase, precipitation has been 10% below normal. More than a third of India’s cultivated acreage has not received adequate rainfall, which is delaying sowing in many parts of the country.

One consequence could be a higher level of inflation than falls in the central bank’s tolerance range of 2-6%. The Reserve Bank of India has raised its inflation forecast for 2021-22 to 5.7% from 5.1%. Based on this, the bank does not expect to be raising interest rates. But independent forecasters predict that the central bank may have to raise rates, with adverse consequences for growth.

However, financial investors do not seem worried, with the benchmark stock index -- the Bombay Stock Exchange’s Sensex -- touching record levels. Foreign investors too have been on average upbeat, with enhanced capital inflows taking India’s foreign exchange reserves to around USD620bn. A rash of new initial public offerings were oversubscribed, though most settled below their offer price when listed. Unicorns (high-value, private-ownership start-up firms that are valued at over USD1bn) are aplenty among start-ups, numbering ten in 2019, 13 in 2020 and more than 20 in 2021 thus far.

Politically, uncertainty prevails, and unrest is on the rise as parties prepare for elections in seven states in 2022, including in the largest state of Uttar Pradesh slated for May. The ruling Bharatiya Janata Party (BJP) that has much at stake is already in campaign mode -- the party is combining a majoritarian Hindu agenda with efforts to push back the opposition and control messaging through the media to get ahead.

Opposition party leaders allege that central institutions such as the Central Bureau of Intelligence, the Enforcement Directorate and the National Investigation Agency are being used to inhibit them, citing evidence of increased instances of raids and actions by these entities.

Efforts to control the media have led to skirmishes between the government and social media platforms such as Facebook, WhatsApp and Twitter and digital media companies, which the government alleges are purveying fake news and content that is biased against the government. To halt that, the government has set compliance requirements and issued new guidelines for governance of these entities, which they have challenged in court. More recently, such rules and guidelines have been extended to e-commerce entities, requiring them to release on demand information on their customers and clients to the government, on national security considerations.

Meanwhile, the farmers’ agitation against three farm laws -- that they believe work to withdraw state support for agriculture and favour corporates that want to build agribusiness empires -- has completed nine months and shows no signs of abating. The government is refusing to withdraw the bills that were rushed through parliament. More recently, these protests have led to violent clashes between the protestors and the police and paramilitary forces.

Internationally, tensions continue in relations with China and Pakistan (which intensified after the abrogation of the special status provided to the state of Jammu and Kashmir in August 2019). Though talks with China following clashes along the border continue, India’s demand for the restoration of the status quo ante in troop positions has not been met. Meanwhile, the US withdrawal from Afghanistan and the takeover by the Taliban in August has strengthened Pakistan’s hand and could lead to proxy conflicts between India and Pakistan.

Unable to win its case in arbitration proceedings and the courts, the Indian government has finally withdrawn the retrospective application of tax law amendments that led to large demands on firms such as Vodafone and Cairn energy in 2012 and 2014 respectively. While this has assuaged fears that the government was giving itself unfair expropriative powers, the sense that foreign firms will not be given national treatment still remains. The main reason is the Make in India and Atmanirbhar India (or self-reliant India) slogans and initiatives, that signal a turn to a nationalist stance favouring sections of Indian large businesses at the expense of foreign investors.

With elections to seven different state legislatures (including in Uttar Pradesh, the largest and strategically most important), campaign-related violence is expected to spike. Given the reliance of the BJP on a divisive communal platform aimed at winning over the Hindu majority by attacking ‘appeasement’ of minority communities by the political opposition, especially of Muslims and Christians, the risk of destabilising communal conflicts engineered for realising political ends is high. In the north-east, ethnic conflict has spilled over into violence in which the police forces of neighbouring states (Assam and Mizoram) were involved along with civilians.

Resistance to the Modi government’s policies in Kashmir continues, with close to 200 militants killed over 2020 and more than 100 so far in 2021. Casualties among the police and paramilitary forces and among civilians have also been high. Intelligence reports point to a spike in militant activity since the abrogation of Article 370, which granted Jammu and Kashmir special status within India’s quasi-federal framework.

Meanwhile, incidents of left-wing extremism in the eastern regions continue to be reported. In a reply to a parliament question, the minister of state for home affairs reported that there were 833 incidents of extremist violence in 2018, 670 in 2019 and 665 last year.

Large inflows of foreign investment and a high level of reserves has made the task of managing the value of the rupee easier for the Reserve Bank of India. However, with the boom in the stock market unconnected with fundamentals and appearing unsustainable, India faces the risk of the boom unravelling, leading to the sudden exit of accumulated legacy footloose foreign investment.

The Modi government is adhering to its conservative fiscal stance. Though the public debt-to-GDP (Gross Domestic Product) ratio has risen significantly from its pre-pandemic levels because government revenues had fallen sharply, much of the borrowing is in the domestic currency, reducing the probability of default to near nil. Meanwhile, the government has announced a major asset monetisation programme, which is expected to yield INR6tr (USD81.4bn) over four years, which would possibly keep borrowing levels in check.

Return to contents Next Chapter