Index trend

Previous Quarterly Editions

Expropriation Risk: 59 58 58 56 ▼Political Violence Risk:66 66 66 66 ►Terrorism Risk:23 23 23 23 ►Exchange Transfer and Trade Sanction Risk: 45 45 54 45 ▼Sovereign Default Risk:65 65 65 65 ►

Overall Risk Temperature: 58 (Significant -3) TREND ▼

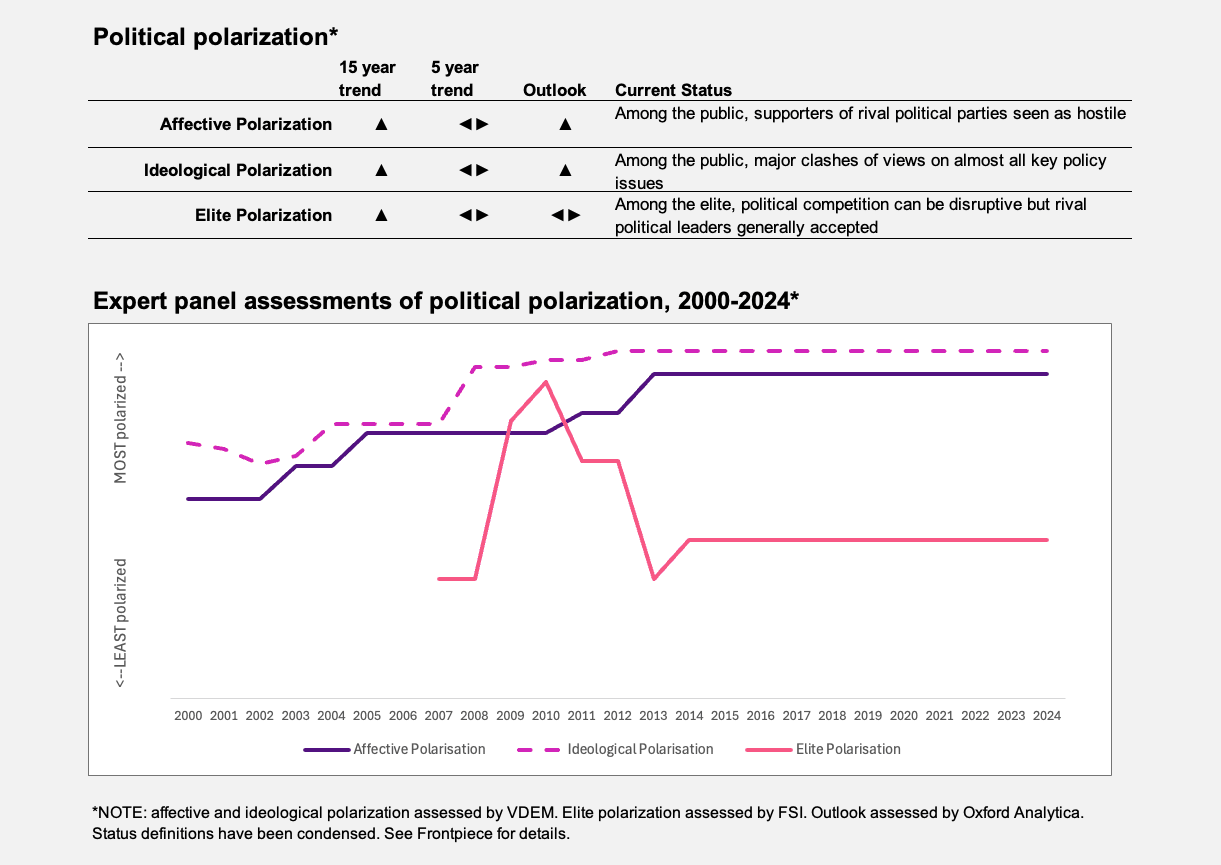

Special topic: Political polarization

Since taking office in December 2023, President Javier Milei has consistently pursued a polarizing discourse both domestically and internationally, demonizing opponents and refusing to negotiate with a Congress in which his own party has only a small representation. Milei’s attacks on public universities, which he accused of socialist indoctrination and threatened to defund entirely, provoked the first large-scale demonstrations against his government’s policies in the early part of last year. Internationally, he has frequently decried the governments of key trading partners such as Brazil and China as corrupt and communist, while wooing far-right leaders such as disgraced former Brazilian President Jair Bolsonaro and the leader of Spain’s Vox party, Santiago Abascal, and referring to the late Argentine-born Pope Francis as a communist and “the representative of evil.”

Milei’s polarizing rhetoric has become even more strident since the election of U.S. President Donald Trump, whom Milei has long identified as a key ally. In his World Economic Forum (WEF) speech in Davos, Milei reiterated his view that “woke ideology is a cancer that must be removed” and accused the WEF of promoting that “sinister agenda.” Thousands of people subsequently protested in Buenos Aires repudiating his comments linking same-sex marriage and pedophilia and calling for the crime of femicide to be eliminated from the penal code. The identification with Trump, largely an unpopular figure in Argentina, has also proved divisive.

Milei has capitalized on the heavy defeat of the previous Peronist government, dominated by then Vice President and now Peronist party leader Cristina Fernandez de Kirchner, herself a polarizing figure who has likewise sought to demonize opponents, branding them as enemies rather than opponents. His election was due to the economic collapse presided over by the previous government, which initially was largely blamed for the economic crisis. This is now shifting, with mounting concerns over poverty, unemployment, inflation, poor growth and corruption under the current administration. This is particularly the case with respect to the impact of falling real pensions and public-sector job cuts, which are prompting rising protests and higher levels of violence. Violent security-force responses to those protests are further driving polarization.

With disapproval of Milei now rising (especially since his involvement in the $LIBRA cryptocurrency scandal and questions over the key role of his sister Karina as his secretary-general and gatekeeper), feelings of political polarization are again rising. Recent opinion polls have seen Milei’s disapproval ratings outstrip approval while voting intentions for the Peronists are rising ahead of the October midterm elections. Most tellingly, the two parties together account for 92% of responses to the question “Who do you most want not to win the election?” — with Milei’s La Libertad Avanza reaching 50.7%.

Although political and economic elites have been more willing to ally or at least have patience with Milei, splits and defections within his own party are becoming increasingly acrimonious, as are divisions between it and former President Mauricio Macri’s PRO party. Key export sectors such as agriculture and steel are also increasingly frustrated with government policies and the impact of U.S. steel tariffs, which Milei has seemingly made no attempt to negotiate. Government relations with traditional media, also increasingly demonized and excluded from government press conferences, have also spilled over into open confrontation.

TREND ▼

Expropriation risk to foreign investors per se is minimal at present, given the number of companies that have already exited Argentina, lack of government funds and the current government’s hope of encouraging foreign investment. Indeed, the current government is focusing on privatizing state companies (albeit with limited success thus far and after having reduced the number of companies up for privatization from 40 to only three) rather than taking on new obligations.

However, the U.S. District Court ruling awarding some $16 billion to minority investors in energy company YPF following the 2012 expropriation of 51% of the company is unlikely to be complied with, raising the likelihood of new efforts to embargo Argentine state properties overseas and complicating any effort to improve investor sentiment. Subsequent events suggest that the value of YPF shares could be further deteriorated, in essence representing a virtual expropriation for its private shareholders. Plaintiffs seeking to identify assets to be seized in order to comply with the U.S. District Court judgment aim to demonstrate that public companies such as YPF are in practice “alter egos” of the state; YPF’s overseas assets could risk seizure given the dearth of specifically state-owned assets abroad that could be subject to seizure.

TREND ►

Protests have continued since Milei took office despite the introduction of draconian security measures to curb demonstrations. While they have largely remained relatively peaceful, more recently the weekly protests in support of pensioner demands have become increasingly violent, with participation by organized groups of violent football supporters as well as a more aggressive response by the security forces. Overall, personal security and the risk of violent crime will remain a key concern, notably in connection with a sharp rise in drug-trafficking-related violence in Rosario, Argentina’s second-largest city.

TREND ► There has been no major terrorist attack in Buenos Aires since 1994, and the risk of terrorism in Argentina remains low. However, in August 2024 the government said it was taking very seriously warnings by Israel that Iran could be planning attacks on countries considered “friends of Israel” — notably including Argentina. Subsequently seven people were arrested in Mendoza province for allegedly belonging to a terrorist cell planning attacks on Jewish targets there, although the circumstances appeared confused. In January 2025 a delivery driver was arrested in Rio Negro province and alleged to be involved in an Islamic State group plan to carry out a terrorist attack on an unspecified target. Continued heightened tensions surrounding the Gaza war and possible Iranian retaliations for Israeli strikes, together with Argentina’s porous borders and large Jewish and Arab communities, mean that an attack cannot be ruled out.

Central bank reserves rose after Milei came to office, reaching nearly $28.2 billion as of March 2024. However, the Central Bank has subsequently been forced to intervene in exchange markets to try to reduce the gap between the official and parallel exchange rates; foreign debt repayments and recent interventions aimed at shoring up the peso following devaluation rumors have seen sharp drops in reserves, which were negative by around $7 billion by mid-March. Efforts to encourage farmers to sell their stocks through a temporary reduction of export taxes have had little success.

The new International Monetary Fund (IMF) deal announced this month prompted the government to announce the adoption of a more flexible exchange rate regime (allowing the Argentine peso to float within a range of 1,000 to 1,400 to the U.S. dollar) and a partial loosening of capital controls, although the latter remain largely in place for companies.

The main concern will remain a possible default on domestic debt as well as the onerous and short-term conditions on which rollovers are being made. Despite heavy capital and interest payments on foreign debt falling due this year, the new IMF deal, including $20 billion in fresh funds, together with new lending from other international financial institutions, will alleviate short-term concerns over foreign debt, even though longer-term doubts remain.

The government could launch a new debt swap to alleviate the domestic payments scheduled for 2025 (some $54 billion). However, its success would mainly depend on keeping most capital controls in place, which will discourage investments and delay any return to global capital markets.

Although the new government achieved a fiscal surplus in 2024, largely by slashing public spending in such areas as pensions and transfers to provinces, this will be difficult to sustain unless the government continues to cut spending, which will be politically difficult with midterm legislative elections due in October; primary spending already showed a rise in the early part of 2025. GDP contracted by 1.7% in 2024, despite some recovery in the past two quarters, with fixed investment, manufacturing, and public and private consumption all down sharply, in large part due to spending cuts and rising concerns over unemployment. Absent a strong rebound in coming months, it will be difficult to sustain the zero deficit target while appeasing mounting social concerns.