Index trend

Previous Quarterly Editions

Expropriation Risk: 78 78 78 79 ►Political Violence Risk:90 85 85 85 ►Terrorism Risk:24 24 24 29 ▲Exchange Transfer and Trade Sanction Risk: 54 54 45 45 ►Sovereign Default Risk:83 83 83 83 ►

Overall Risk Temperature: 73 (Medium high) TREND ►

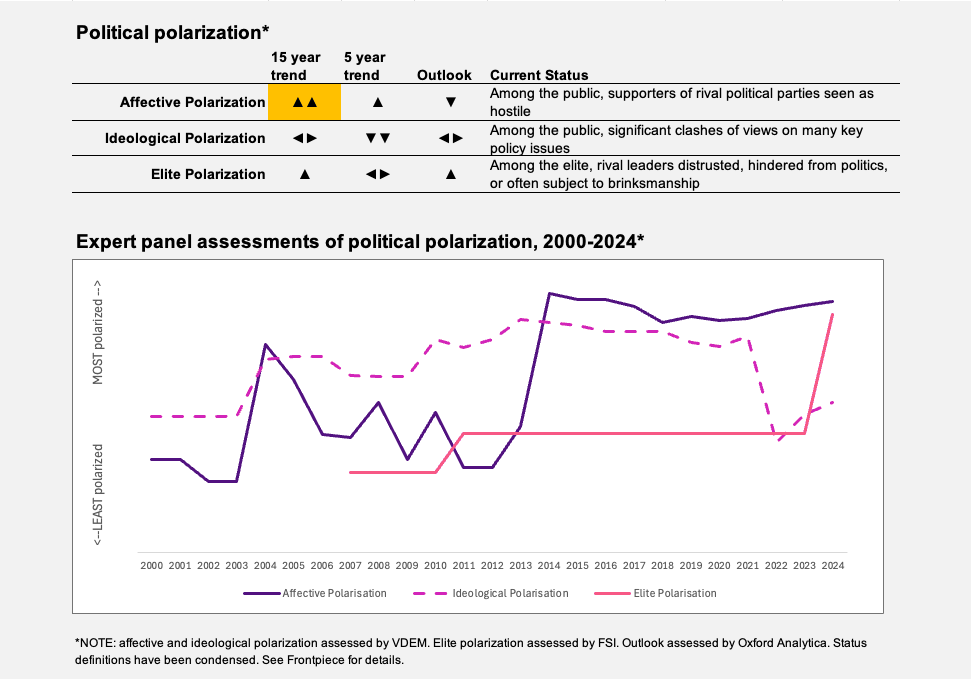

Special topic: Political polarization

Russia’s invasion in 2022 triggered a powerful rally-around-the-flag effect and has temporarily muted many partisan conflicts. Public support has coalesced behind President Volodymyr Zelenskyy, whose approval skyrocketed. In the early phase of the war, even opposition parties largely refrained from harsh criticism.

These conditions significantly reduced affective polarization as Ukrainians focused on shared opposition to a common existential threat. Surveys indicate that while some social and linguistic divisions exist, most Ukrainians do not feel hostility toward internal groups, and perceived societal schisms are often exaggerated by propaganda. The war has united the populace emotionally, curbing the previous bitterness of domestic politics.

There is broad support for the postponement of elections until the conflict ends. Even major opposition figures agree that wartime elections would be impractical and illegitimate. This unity reflects a conscious prioritization of victory and stability over politics as usual.

However, even though elite polarization has lessened during the conflict, rivalry has not disappeared. The most glaring example is that between Zelenskyy and his predecessor, Petro Poroshenko, leader of the European Solidarity party. Although both leaders share a pro-Western, anti-Kremlin stance, their personal and political feud has persisted during the war. In 2022 there was tacit agreement among political elites not to undermine each other publicly during the existential fight, and, for a time, direct attacks were shelved. Zelenskyy’s government suspended its pre-war criminal cases against Poroshenko — which had drawn accusations of political persecution — and Poroshenko’s camp tempered its criticism of the government’s wartime decisions. However, this truce frayed as the initial shock of invasion gave way to protracted conflict. By 2024, opposition voices began reasserting themselves.

The rivalry truly erupted in February this year, when the National Security and Defense Council (NSDC) — chaired by Zelenskyy — imposed sanctions on Poroshenko. Zelenskyy signed a decree approving an NSDC decision to sanction the former president for alleged threats to national security. This unprecedented move froze Poroshenko’s assets, banned capital transfers on his behalf and even restricted his foundation’s ability to purchase defense supplies for the army. Poroshenko slammed the sanctions as unconstitutional and politically motivated, accusing Zelenskyy of dealing a “huge blow to internal unity” which he said had been Ukraine’s “main weapon” against Russia. In effect, the war did not eliminate elite polarization so much as put it on pause — and by 2024 to 2025, the old divisions at the top had resurfaced, potentially with even greater bitterness.

Beyond personal rivalries, ideological differences endure in Ukrainian politics, though their contours have evolved during the war. Any pro-West versus pro-Russia divide has largely vanished from mainstream discourse; the main pro-Russian party was banned in 2022, and its leaders either fled or reinvented themselves as Ukrainian nationalists. All major political forces today share the strategic consensus on defeating Russian aggression and pursuing EU and NATO integration. However, disagreements persist over values, policies and Ukraine’s post-war trajectory that will become more salient once the war ends.

TREND ►

Expropriation risk in Ukraine must be viewed through the lens of war-related state intervention versus peacetime investment protections. On one hand, under martial law the government can forcibly confiscate property for defense purposes with compensation paid later as provided by law, which elevates expropriation risk as long as the war continues. The government in November 2022 invoked this power for the first time to take control of majority stakes in five strategic companies — including an engine maker and energy firms — previously owned by some of the country’s wealthiest tycoons. Zelenskyy justified the move as critical for national survival and explicitly rooted in existing law.

Since the war began, Ukraine has confiscated over 50 companies belonging to Russian citizens and Ukrainians found to have collaborated with Russia. The confiscated assets are technically owned by the government’s privatization arm, the State Property Fund, and can be put on sale with a view to generating funds for post-war reconstruction.

Two new cases this year are connected to sanctions imposed on individuals. On February 20, the government announced plans to nationalize 49.5% of Poltava Mining, the Ukrainian subsidiary of Ferrexpo, a firm incorporated in Switzerland and listed in London, but controlled by Kostyantyn Zhevago, a Ukrainian businessman sanctioned by the Zelenskyy government for allegedly undermining national security. Then, on March 6, the Ministry of Justice filed a suit to confiscate more than 440,000 tonnes of bauxite and 110,000 tonnes of alumina stored at a plant belonging to Russian oligarch Oleg Deripaska’s Rusal company.

Outside extraordinary wartime measures, Ukraine has shown a strong commitment to protecting investors and avoiding arbitrary expropriation. The Zelenskyy administration before the war had pursued reforms to improve the business climate, offering incentives to foreign investors. There have been no cases of the government expropriating foreign companies’ assets arbitrarily. On the contrary, Ukraine depends on Western economic support and will urgently need foreign capital for postwar reconstruction, so it will seek to reassure partners that property rights (except for Russian state or sanctioned entities) will be respected.

The immediate risk of political violence relates entirely to the war with Russia — and this risk is extremely high. No other political risk factor compares to the immediate violence inflicted by Russia’s invasion: Thousands of civilians have been killed, millions displaced, and cities across Ukraine have been shelled or bombed. Russian missile and drone strikes have frequently targeted civilian infrastructure — power grids, residential buildings, hospitals — causing casualties and terror far from the front lines. Every region of the country lives under the threat of long-range attacks.

In terms of internal political violence — civil unrest, insurgency or violent protests — the risk is low and likely to remain so as long as the war continues. There have been no significant anti-government protests or violent political clashes in government-controlled territory since the invasion. The public largely accepts curbs on demonstrations and media as necessary in wartime, and there is a strong social pressure against undermining the war effort.

However, underlying pressures are building. The economy has been severely damaged, poverty has risen and millions of people have been displaced — conditions that would be ripe for unrest without the unifying pressure of the war. So far, Ukrainians have shown resilience and patience, directing their anger toward Russia rather than their own leaders, but the longer the conflict drags on, the greater the fatigue and potential for demonstrations demanding better living conditions or even a push for negotiations. If a ceasefire or peace is achieved, external violence would drop sharply — but that might be the moment when suppressed internal political grievances surface.

TREND ▲

In recent months, Russia appears to have been making more active use of collaborators and saboteurs recruited from among Ukrainians for terrorist-style attacks such as arson attacks on Ukrainian military vehicles and attempted bombings of transport infrastructure. The risk of terrorist attacks not linked to Russia is very low, as the Ukrainian state has no other external or internal enemies that employ terrorist tactics.

The local currency — the hryvnia — stabilized against major currencies in the first quarter of 2025, after sliding down for much of the previous quarter to reach a new all-time low against its de facto peg, the U.S. dollar.

The central bank maintains currency restrictions to conserve international reserves, which have been shored up to record levels (over $40 billion as of March) by donor funding. These reserves provide a buffer (about five to six months of import cover) and have allowed some cautious steps toward liberalizing the exchange rate in May last year, with more planned. However, if external financing falters, the hryvnia could come under severe pressure, potentially forcing a return to tighter currency controls.

Ukraine’s trade sanctions risk relates to Russia primarily, but the two countries have exhausted their scope for further sanctions.

Ukraine’s sovereign default risk is very high, even after recent measures to restructure its debt and buttress government finances. In practical terms, Ukraine is shut out of international capital markets. It cannot borrow commercially at reasonable rates and relies on official support from friendly governments and multilateral institutions. Credit rating agencies classify Ukraine’s foreign debt status as ’selective default’ or ’restricted default.’

In September last year, Kyiv completed a comprehensive restructuring of about $20.5 billion in bonds that it negotiated with international creditors, including a 37% write-down, saving it $11.4 billion through 2027.

Despite these measures, Ukraine’s external public debt burden reached around 90% of GDP last year and is poised to grow. The fiscal deficit has ballooned to nearly 20% of GDP due to military spending and collapsing revenues, and Kyiv fills this gap only through international aid and printing money. As long as the war continues, the government will depend on tens of billions of dollars in external support annually to finance basic expenditures. This means that the risk of a renewed debt crisis or default will quickly resurface if external support falters.

Whenever the war ends, Ukraine faces a reconstruction effort estimated in the hundreds of billions of dollars and will likely require some form of debt forgiveness or long-term aid to avoid insolvency.

The content of this document is believed to be accurate at the time of publishing but due to the rapidly evolving situation, changes are occurring frequently and this information may have been superseded. Coverage may vary depending on the jurisdiction and circumstances. For global client programs it is critical to consider all local operations and how policies may or may not include coverage relating to the Ukraine crisis. WTW is not in a position to provide any advice in relation to sanctions. Please ensure you are taking advice from your own legal and/or other professional advisors before taking any action. The views expressed in the section are the opinion of Oxford Analytica and do not necessarily reflect those of WTW.