Index trend

Previous Quarterly Editions

Expropriation Risk: 54 54 54 54 ►Political Violence Risk:57 57 57 57 ►Terrorism Risk:53 53 53 50 ▼Exchange Transfer and Trade Sanction Risk: 54 54 54 45 ▼Sovereign Default Risk:83 83 83 75 ▼

Overall Risk Temperature: 59 (Significant -3) TREND ▼

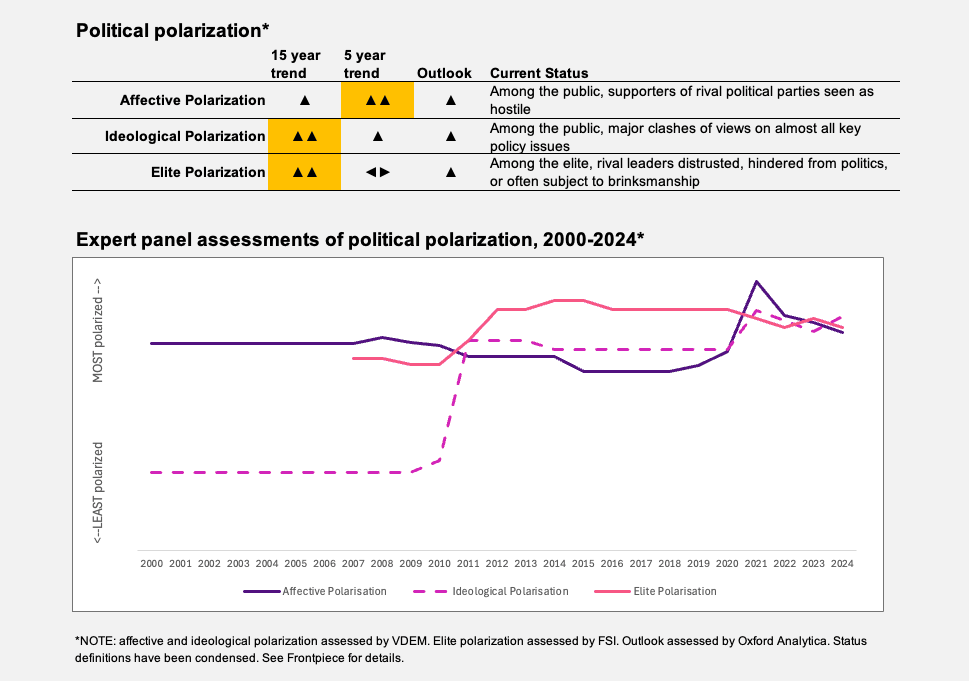

Special topic: Political polarization

Tunisia transitioned from a dictatorship under Zine el-Abidine Ben Ali to a democracy after the Arab Spring revolution that began in late 2010. In the decade that followed, its politics were marked by a strong emphasis on consensus, particularly between secular and Islamist forces, to reduce polarization. This approach was exemplified by coalition governments and the near-unanimous approval of the 2014 constitution. It earned Tunisia international acclaim and was seen as a key factor in avoiding the turmoil faced by its Arab neighbors.

However, while consensus helped establish the ’rules of the game,’ it also stifled political competition. Rather than transitioning to competitive politics, the drive to constantly reach consensus hindered the establishment of a healthy democracy.

Successive governments struggled to address key challenges, such as reforming the economy and establishing a Constitutional Court. Tunisians grew disillusioned with political parties and democracy itself. The compromises made by the two major parties, Ennahda and Nidaa Tounes, not only failed to resolve underlying issues but also, in the end, fueled polarization, leading to the rise of more ideologically extreme politicians.

One of these was Kais Saied who won the presidential election in 2019 on an anti-establishment platform and suspended parliament in 2021 in a ’self-coup.’ He won a second term in October 2024 in tightly controlled elections. Since he took power, he has increasingly sought to control the political environment by arresting his opponents and suppressing dissent. For example, the trial of around 40 high-profile opponents of Saied on April 19, 2025, saw sentences of 13 to 66 years given to defendants charged with conspiring to overthrow Saied. Saied has controlled the judiciary since 2022.

Saied’s consolidation of power since 2021, including ruling by decree and dismantling democratic institutions, has deepened divisions between his supporters and opponents. The suppression of dissent, arrests of opposition figures and restrictions on media freedom have alienated many Tunisians, while others view his actions as necessary to address corruption and inefficiency. Saied also uses populist rhetoric that polarizes society, often framing issues as a battle between “the people” and “corrupt elites.”

Against the backdrop of an ailing economy, controversial measures and public discontent with the government, divisions will persist.

TREND ►

Although not outright expropriation, delays and obstructions from the government can hamper business operations in Tunisia. The unpredictable and autocratic style of the president is a concern for businesses, especially given that judicial independence is eroding.

A tribunal from the International Center for Settlement of Investment Disputes ruled in Tunisia's favor in December 2023 in a long-running expropriation claim brought by the Dutch ABCI Investments. The latter had sought damages worth $12 billion in a dispute over its failed attempt to buy a stake in the Banque Franco-Tunisienne in 1982.

More recently, Zenith Energy initiated arbitration proceedings against Tunisia under the United Kingdom-Tunisia bilateral investment treaty. Zenith seeks $503 million in damages for ’unreasonable and arbitrary obstructions’ affecting its subsidiaries in the Sidi El Kilani and Ezzaouia concessions. The hearings are set for December 2025.

Several businessmen have been arrested over the past few years, notably the tycoon Marouane Mabrouk, who was detained in November 2023 over allegations of embezzlement during the rule of former President Ben Ali. Saied has stepped up calls in recent months for prosecutors to take tougher action against business leaders over historical corruption claims, seemingly in an attempt to pressure them to accept settlement deals that would provide the state with a much-needed injection of funds.

Protests have risen substantially over the past year. A Tunisian organization that tracks protests and social movements, the Tunisian Social Observatory, recorded a near 140% increase in protests in February 2025 compared with the same period in 2024, from 179 protests to 429. Demonstrations were widespread, with various groups — including unemployed graduates, school supervisors and substitute teachers — demanding better infrastructure, regional development and socioeconomic improvements. Few of these protests and strikes are violent, and Tunisia has a robust history of civil action. Yet a small risk is there.

TREND ▼

Terrorist attacks have decreased as extremist organizations’ communications and organizational networks have been effectively disrupted since two mass shootings in 2015. On January 31 this year, the government extended a state of emergency until the end of 2025.

Most incidents in the past few years have been ’lone-wolf’ attacks. The most recent are three in 2023: In May, a member of the National Guard shot dead three security officers and two worshippers at a Jewish pilgrimage site, while separate knife attacks in June and July left one police officer dead and another wounded.

Foreign currency reserves decreased from 105 days’ worth of imports in early 2024 to 98 days’ worth of imports by March 2025 (approximately 22.45 billion Tunisian dinars) — close to the critical level of three months’ worth. Over 40% of Tunisia’s debt is issued in hard currency, exposing the economy to potential dinar devaluation.

The government attempted to partially liberalize foreign exchange transactions in 2024, to improve the business environment and attract foreign investment. However, in November 2024 parliament rejected the proposed amendment to the 2025 Finance Bill that would have simplified the opening of foreign currency accounts for those residing in Tunisia.

The Central Bank of Tunisia plays a central role in regulating foreign exchange operations. However, concerns about its independence have grown since a 2024 law allowed exceptional fiscal monetization, which could undermine the bank’s ability to manage monetary policy effectively.

Tunisia's trade sanctions risk primarily relates to EU sanctions targeting individuals and entities associated with corruption and the misappropriation of state funds, particularly those connected to the Ben Ali regime. The sanctions include asset freezes and restrictions on economic resources, which apply to individuals, companies and entities identified as responsible for financial misconduct.

Tunisia faces a high risk of sovereign default. Its debt-to-GDP ratio is expected to rise from 83.7% in 2024 to 84.3% in 2025. To reduce reliance on foreign debt, the government has turned to domestic financing, primarily through commercial banks, which already hold sovereign debt equivalent to 12% of GDP. This growing dependence increases banks' vulnerability to sovereign risk.

Efforts to improve Tunisia's fiscal position have seen some success, with the deficit projected to narrow from 6.9% of GDP in 2023 to 5.1% in 2025. However, the economy is highly exposed to external shocks due to reliance on imported energy and food. Political resistance to reforms backed by the International Monetary Fund, such as subsidy cuts, has constrained multilateral financial aid, leaving Tunisia reliant on bilateral support. This fragile fiscal and trade environment heightens the risk of default.