Index trend

Previous Quarterly Editions

Expropriation risk: 54 54 53 52 ▼ Political violence risk:57 57 57 57 ►Terrorism risk:57 57 54 58 ▲Exchange transfer and trade sanction risk: 45 45 45 44 ►Sovereign default risk:47 47 37 37 ►

Overall Risk Temperature: 53 (Medium) TREND ►

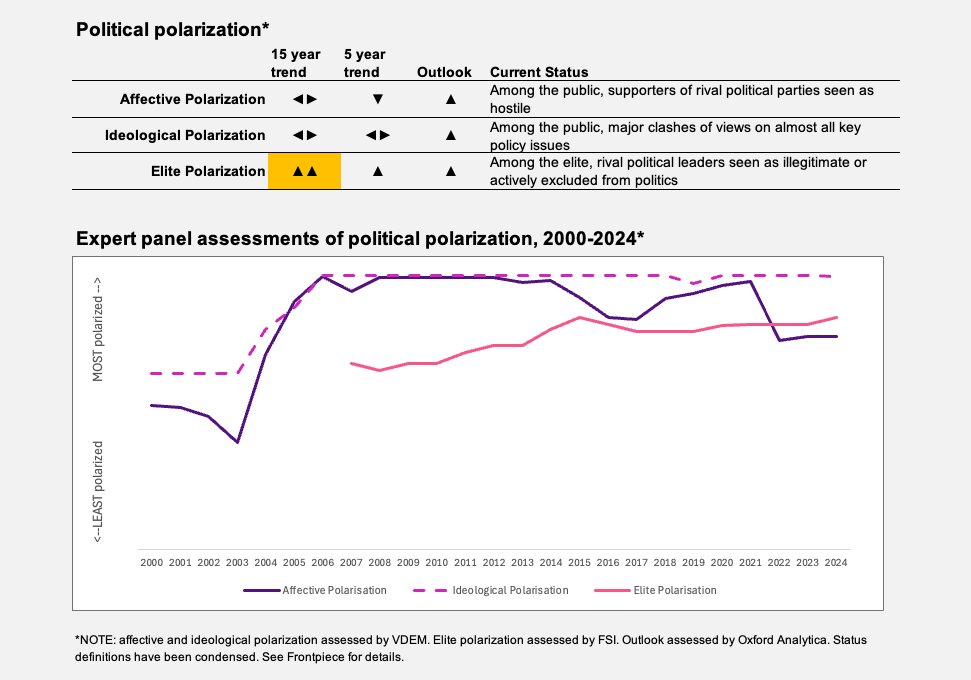

Special topic: Political polarization

Politics in Thailand are a complicated mix of polarization between opposing elite classes — roughly divided between ’old money’ conservatives and ’new money’ billionaires — with a strong tradition of military rule in a constitutional monarchy that nevertheless penalizes any criticism of the monarch.

Since 2000 and the arrival of the Shinawatra political dynasty, established by then-Prime Minister Thaksin Shinawatra, populism has been a growing theme in electoral politics, one that has been interrupted at times by military coups in 2006 and 2014 — the former against Thaksin and the latter against Prime Minister Yingluck Shinawatra, his sister.

In response to the late 20th century surge in populism, the Thai judiciary has become a popular tool of the political right to remove politicians whom they believe have accrued too much support from the Thai public, sometimes along with the dissolution of their parties. Although Thai political parties tend to be organized around individuals rather than ideologies, in recent years they have become more identifiable on the political spectrum through their positions.

Although the labels often imply a more zero-sum polarization than is the case, Thai politics are commonly referred to as being split into the ‘Red Shirt’ and ‘Yellow Shirt’ camps. Red Shirt parties and politicians are considered to be more populist and progressive, often from the ethnic Chinese Thai nouveau riche class that emerged in the mid-1980s, with some roots in rural areas, particularly Thailand’s northeastern region where poverty is the most prevalent. Yellow Shirt politicians hold up the conservative end of the political spectrum and are often more pro-military. They are also reckoned to be more pro-monarchy, although only the more leftist parties profess a position on Thai royalty; most parties pledge their loyalty to the monarchy.

Over the past year, political polarization in Thailand has increased and is likely to widen further, with the return of the Shinawatra family to power, in this case with Thaksin’s daughter, Paetongtarn, as prime minister. In 2024, Thaksin himself returned from a 15-year self-exile to serve a brief prison term and was then released with a royal pardon. Yingluck, also in self-exile, is considering returning to Thailand in the hope of following a similar path. What alarms Yellow Shirt politicians, however, is not Paetongtarn as a second-generation leader of the Pheu Thai Party (PTP) — the family party — but rather Thaksin’s continued presence in Thai public affairs. A petition to the Constitutional Court in 2024 attempted to convict him of ’interference’ in the policies of the PTP and also to dissolve the party; it did not succeed, but future attempts could succeed if political tensions rise further.

TREND ▼

The risk of expropriation is moderate and stable.

Thailand will continue to encourage foreign direct investment as a major driver of economic growth in an attempt to avoid the middle-income trap and so will pursue investor-friendly regulations where politically possible. There are strong possibilities that the country will become a major regional hub for the manufacture of electric vehicles over time, building on its status as the preferred hub for automotive assembly in Southeast Asia.

Nevertheless, Thailand’s forward infrastructure investment projects with China will require care in their negotiation and execution, for two reasons. First, Washington will expect Bangkok, as a treaty ally of the U.S., to favor Western supply chains over Chinese and Russian ones. More specifically, in her meeting with Chinese President Xi Jinping earlier this year, Thailand’s prime minister expressed agreement in principle to pursue completion of a high-speed rail link from Kunming to Bangkok with the construction of a line from northern Thailand to the capital. Beijing had been pressing the project upon Bangkok for a decade. Although the Thai government has indicated that it will be the sole funder of the project, if and when construction begins it could become controversial with affected populations, and even with the Thai national security sector, which has expressed reservations about giving China such access to Thai territory.

TREND ►

The risk of political violence is significant and rising.

Two factors could increase the prospects for political violence in Thailand in the near term. The first is former Prime Minister Thaksin’s growing role in Thai public affairs, particularly with neighboring states. A long-simmering dispute between Thailand and Cambodia over maritime assets in the Gulf of Thailand — which tends to raise nationalist tensions on both sides — has been revived, and Thaksin’s public comments on the conflict have raised hackles with the Thai military.

On top of that, in a period of growing uncertainty in the international economy, a slowdown in economic growth could easily translate into public protests.

TREND ▲

The risk of terrorism is significant and rising.

Bangkok’s negotiations with Muslim separatist groups in southern Thailand have stalled. The resumption of the Israel-Palestine conflict in Gaza has been felt throughout Muslim Southeast Asia, which raises the risk of terrorism slightly.

A greater risk is continued enmity between the U.S. and Iran, which could revive Hezbollah activity in Thailand. In recent decades, Thai security agencies have uncovered Hezbollah cells and plots to bomb tourist sites, particularly in Bangkok, drawn primarily to a sizable number of Israeli tourists in Thailand.

Exchange transfer and sanctions risk is moderate and rising.

The Asian Development Bank reported Thailand’s GDP growth in 2024 at 2.6%, below the regional average and an indication that the Thai economy has yet to recover from the COVID-19 pandemic. The International Monetary Fund projects a growth rate of 2.9% for 2025, but that could be lower if Thailand encounters strong economic headwinds. The country has the second-largest trade surplus with the U.S. in Southeast Asia, and there is no guarantee that the Thai government will be able to negotiate an exemption to increased tariffs with the Trump administration. Moreover, rising labor costs will make Thailand less desirable as a site for Western investment redirected from China, compared with Vietnam and Indonesia. This could incline Bangkok to seek more Chinese investment, albeit in sectors that would not invite secondary sanctions from the U.S.

The risk of sovereign default is moderate and rising.

The Thai cabinet’s approval of a medium-term fiscal plan (2025–2029) projects an increase in the ratio of public debt to GDP, which would climb from 65.7% in 2025 to 69.3% in 2029, ultimately grazing up to the 70% red-light threshold for debt management set by the State Fiscal and Financial Discipline Act of 2018.

The plan is expected to slow economic growth over the five-year period, combined with continued high levels of household debt. A study released by Chulalongkorn University in January this year found 2024 household debt to be 104% of GDP, taking into account informal loans. The official government estimate of house debt, which excludes such loans, was estimated at 90% for the year.