Index trend

Previous Quarterly Editions

Expropriation Risk: 57 57 57 57 ►Political Violence Risk:48 48 48 48 ►Terrorism Risk:26 26 26 26 ►Exchange Transfer and Trade Sanction Risk: 45 45 45 45 ►Sovereign Default Risk:65 65 65 65 ►

Overall Risk Temperature: 54 (Medium) TREND ►

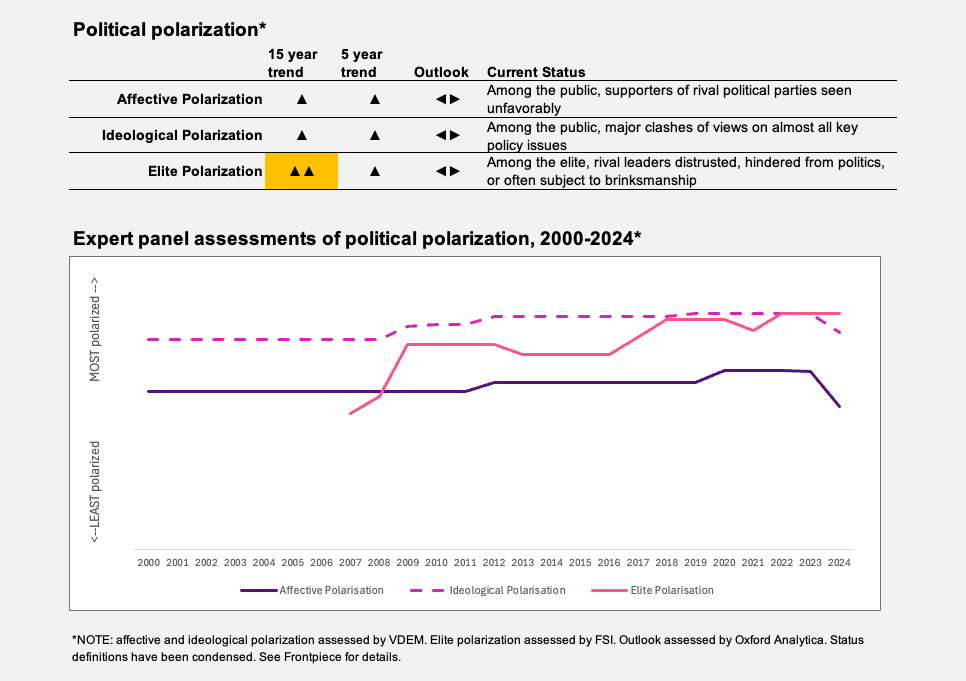

Special topic: Political polarization

South Africa has a very high potential for worsening political polarization. However, this has not precluded compromise and conflict management features, which, to date, have enabled government, opposition and population groups to live with each other — without harmony but with a reasonable degree of civility. Indeed, post-apartheid society has been consciously built around the need for such coexistence, on the awareness among elites of the dire consequences of reverting to a society bifurcated into two implacably hostile camps. Management of polarization was expressed in the negotiations to end apartheid and draft a constitution in the 1990s, widespread (though not universal) acceptance of the rule of law and near-universal acceptance of the verdict of seven free elections since 1994. The continuation of ’managed polarization’ was evident last year when the African National Congress accepted the loss of its parliamentary majority and agreed to form a Government of National Unity with the main opposition party.

Factors that underlie polarization include inequality, spatial separation of racial groups and support for political parties that follows racial lines. South Africa has the highest degree of inequality in the world, with a Gini coefficient currently at 0.63 — a legacy of colonialism and apartheid’s all-embracing structures of economic exploitation and severe political repression. Even 35 years after the end of legislated racial segregation, the population remains largely segregated residentially, with the white population (7.3% of the total) concentrated in certain areas. Segregation in education follows similar patterns. South Africa’s intermarriage rate is ‘extremely low’ according to comparative demography researchers.

Party support follows racial lines: in the 2024 election, among the four largest parties, virtually all those who voted for the African National Congress, Umkhonto we Sizwe and the Economic Freedom Fighters were black Africans, whereas Democratic Alliance voters were 58.6% white, 18.5% South African mixed-race, 14.3% Black and 8.5% Indian.

Populist rhetoric portrays the political, constitutional and economic status quo as the product of a cross-racial elite conspiracy. However, surveys suggest that official values are broader based than that and that social distance is not as extreme as might be expected from basic socioeconomic facts. The well-respected Afrobarometer public opinion survey in 2022 indicated that large majorities would accept people from other ethnic groups and political party affiliations as neighbors.

Managed polarization does not appear to be in imminent danger. However, elite anxiety about polarization remains high. Populist parties that openly have an interest in exploiting polarization now account for 25% of seats in parliament. The longer that weak growth, unemployment of over 30% and widespread poverty persist, the greater the danger that polarization will burst the bonds that presently contain it.

TREND ►

A much-delayed Expropriation Bill was signed into law by President Cyril Ramaphosa in January 2025. This legislation is central to the Trump administration’s punitive approach to South Africa. U.S. President Donald Trump claims that the act is racially discriminatory and presages a wholesale deprivation of white landowners’ property. Trump is defending not so much the interests of U.S. citizens and companies but those of white South Africans. Central to both international and domestic contention are new provisions in the act for ‘nil compensation’. Contrary to Trump’s broadsides — which are dismissed as ignorant misinformation by a very broad consensus in South Africa — the act emphasizes due process and safeguarding of rights under the Constitution.

The conditions under which nil compensation may be awarded are strictly defined and confined to land. Land that is being productively used is effectively ruled out. However, the Democratic Alliance and other domestic critics argue that weaknesses in the legislation could be used as leverage for a program of wholesale expropriation under a future populist government. This is contested by independent legal and economic experts. Former President Jacob Zuma’s Umkhonto we Sizwe (MK) party and the Economic Freedom Fighters are both hostile to foreign investment and propose programs of extreme nationalization and expropriation. At present they together hold only 25% of seats in the national assembly, and the next general election is not due until 2029.

Interventions by Trump appointee Elon Musk suggest that a U.S. government campaign against South African government impositions on foreign investors might unfold. These impositions are effectively taxes to further broad-based black economic empowerment policies. Musk — a South African citizen by birth — has claimed that he cannot own a business in South Africa “because he is white.” It is likely that he knows this is untrue, but it may be an opening salvo against regulatory exactions to which, under due process, all domestic and foreign companies are subject.

Following past trends, there have been few explicitly political killings since the May 2024 elections.

Zuma’s MK party garnered 16% of the vote nationally and 45% in KwaZulu-Natal but has been excluded from both national and regional coalitions. This exclusion feeds an already potent sense of grievance and persecution cultivated by Zuma at the head of an ethnically chauvinist party fueled by a warrior ethos. MK is preoccupied with problems of internal party management and has yet to develop a credible path to political influence by legitimate means. Frustration at this could motivate Zuma’s followers to violence in KwaZulu-Natal, perhaps along the lines of the riots and looting that took place in 2021.

Tensions arising from the Trump administration’s perceived bullying and punitive measures on South Africa could lead to U.S. assets being targeted in protests.

Risk levels remain low, with no current specific threats from domestic or international terrorists. Systemic vulnerabilities arising from weak security force capabilities are a source of risk. Improved legislation and regulation against money laundering and terrorist financing, in response to the Financial Action Task Force’s grey listing, has yet to produce high-profile prosecutions.

The rand has given up some of the gains it made against the U.S. dollar resulting from improved confidence at last year’s formation of the Government of National Unity. Market expectations are that it will trade in the region of 18.4 rand to the U.S. dollar in the coming months, with possible rapid movements in either direction driven by global uncertainty and concerns about government stability, driven by difficulties in passing the budget.

A record gold price was supportive in early 2025, and this safe haven effect could continue in the face of global trade war concerns.

Deteriorating relations with the U.S. could lead to punitive trade measures such as expulsion from African Growth and Opportunity Act.

The cabinet did not support Finance Minister Godongwana’s proposed budget in February. In the long-term absence of healthy growth, tax saturation, along with the debilitating effects of previous austerity, has narrowed options for dealing with a potential fiscal crisis.

Taking on more debt is ruled out. Godongwana proposed increased expenditure, mainly on growth-supporting infrastructure, welfare, and workforce expansion for frontline education and health. Raising VAT from 15% to 17% was intended to fund the required 60 billion South African rands. The Democratic Alliance and some other coalition parties refused this, mainly on grounds that it is ’anti-growth.’ Godongwana tabled a revised budget, including a 0.5-percentage-point rise in VAT in each of the two following years. This was passed without the Democratic Alliance but with support from some parties outside the ruling coalition. This support was conditional. In what it clearly perceived to be a deteriorating political situation, the Treasury abruptly withdrew the VAT rise altogether in the night of April 24 to 25, promising expenditure revisions to fill the budgetary gap.

The Treasury now projects debt stabilizing at 76.2% of GDP in 2025 to 2026, before declining. Markets are skeptical of this forecast on grounds of rising debt service costs (22% of budget expenditure at present), supporting state-owned enterprises and global uncertainty surrounding U.S. trade policy. An above-inflation wage deal for the public sector unions just before the budget suggests continuity with the previous ANC administration rather than a new direction.