Index trend

Previous Quarterly Editions

Expropriation Risk: 44 43 43 42 ►Political Violence Risk:35 35 35 35 ►Terrorism Risk:33 33 33 33 ►Exchange Transfer and Trade Sanction Risk: 44 63 55 54 ►Sovereign Default Risk:82 74 75 74 ►

Overall Risk Temperature: 51 (Medium -1) TREND ►

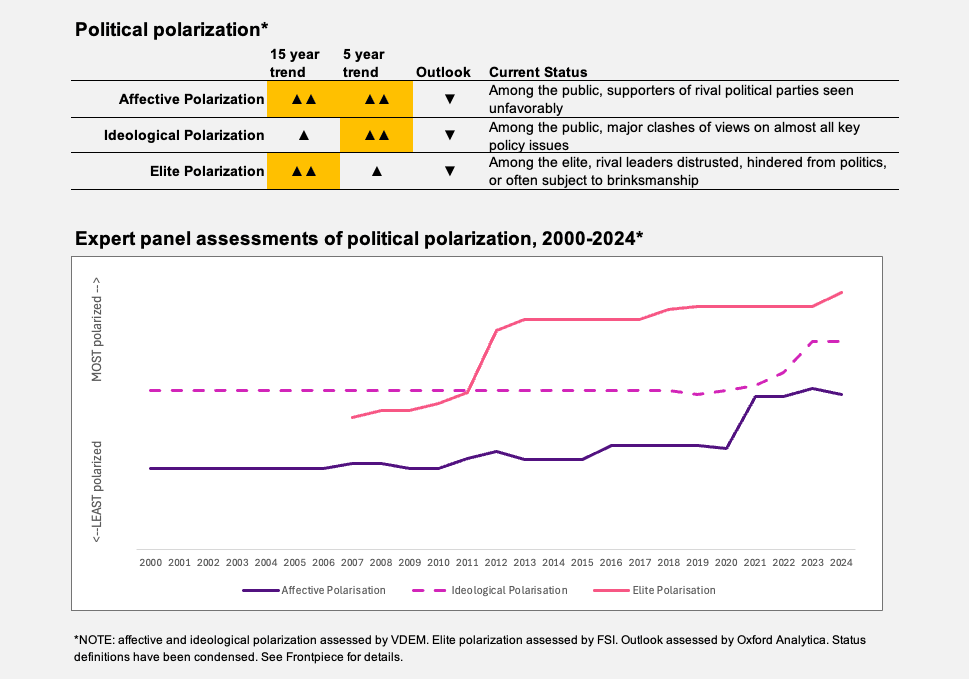

Special topic: Political polarization

Affective political polarization in Senegal is likely somewhat limited, although this is a new phenomenon and is the result of very specific conditions that are unlikely to hold over the next half decade.

The country emerged in late March 2024 from a three-year political crisis in which dozens of opposition protesters were killed and over 1,000 were thrown into prison, including much of the leadership of the then-opposition Patriots of Senegal (Pastef) party. However, Pastef’s overwhelming victory in the March 2024 presidential election and subsequent November 2024 legislative polls have given it both undisputed dominance of Senegal’s political space and a nearly unprecedented degree of political legitimacy. The semi-cathartic electoral resolution of the crisis and the disarray and near powerlessness of the former ruling coalition and its allies has lent a degree of calm to Senegal that it has not seen since at least 2012.

However, the electoral victories of President Bassirou Diomaye Faye and Prime Minister Ousmane Sonko were accompanied by Pastef’s sweeping reform program, promising better standards of living, anti-corruption campaigns, judicial reform and something of a refoundation of the social contract. The government has been trapped by its own rhetoric; its promises of transparency have led to a public audit of state finances, which has revealed that the previous administration of President Macky Sall had grossly misled the public and markets as to the state of government finances. Indeed, the government’s position is much more fragile than most outside observers — even, it seems, the International Monetary Fund (IMF) — had believed.

According to the public auditor, at the end of 2023 the real debt stood at nearly 100% of GDP instead of an announced 76%, while the deficit was 12.3% of GDP instead of the official 4.9%. This puts the government in a fiscal straightjacket, and it has already announced austerity measures on top of an already-tight 2025 budget.

This risks derailing some of the government’s reform promises and antagonizing social groups who were enthusiastic backers of Pastef during the 2024 electoral campaigns. Sonko has asked trade unions to relax their demands given the government’s position, but a number of major strikes are possible in the education, transport and health sectors due to the inability of the government to increase wages.

If the government struggles to deliver on popular expectations — expectations that were already difficult to meet given the country’s deep structural challenges — it could face growing popular anger, a loss of popularity and a potentially re-energized opposition. While this is unlikely to lead in the short term to the kinds of mass mobilization seen under Sall’s administration, it poses longer-term risks of renewed polarization.

TREND ►

The expropriation risk is low to moderate. Despite the administration's sometimes radical rhetoric, its economic program is overwhelmingly reformist rather than revolutionary, with an emphasis on reducing the debt, streamlining budget procedures and improving administrative efficiency. If promises to bolster judicial independence are implemented, expropriation risks may even decline.

However, current fiscal pressures far exceed those expected when Faye and Sonko took office last year. This will add to pressures to find new sources of revenue and to squeeze more revenue out of existing sources. Both Faye and Sonko heavily criticized Sall’s administration for signing murky contracts with foreign investors, especially in the oil and gas industry. Following their election, they promised to review existing contracts and potentially renegotiate them to secure fairer terms for Senegal.

These negotiations are reportedly currently under way, particularly with Australia's Woodside Petroleum, operator of the Sangomar oilfield, and BP, which has led development of the Grand Tortue Ahmeyim offshore gas project.

The companies have reportedly been impressed by the government's realistic and well-briefed approach, and it seems likely that they will be able to reach compromise agreements on adjustments to the terms of these flagship projects, both of which entered production in recent months.

A related issue is that, partly because of Senegal’s fiscal position, the government has made aggressive efforts to enforce tax laws and collect arrears from a variety of economic actors. Both Faye and Sonko built their careers in the tax administration, and this issue is important to them.

Future investors may thus face more forthright demands for revenue-sharing and greater pressure to ensure higher levels of local employment and clearer benefits to host communities. The new administration may also seek more from existing international agreements, such as a renewal of lapsed fishing accords with the European Union, which are perceived to have negatively impacted fishing stocks and local employment.

Despite the approaching end of the government’s honeymoon period and rising social demands, the risks appear minimal in the coming months. Major protests last year, and their violent repression, were the outcome of a three-year-long political crisis between Sall’s administration and the former opposition, whose most prominent figure is the current prime minister. With Sall out of the picture and most of the 1,000 opposition activists, including Faye and Sonko, now released from prison, the main drivers of tension have abated.

However, the new administration’s fiscal constraints and other obstacles — including powerful vested interests, institutional hurdles and structural imbalances in Senegal’s economy — threaten the government’s reform ambitions. There are few easy policy solutions to these problems, meaning that many within Pastef’s enthusiastic voter base could grow disillusioned with the lack of progress in the coming years. This could provide the seedbed for future unrest and popular mobilization. There are already serious threats of major strike actions.

The terrorism risk is low to moderate as regional jihadist insurgencies approach the Senegalese border. Jihadist expansion in southern Mali is especially concerning. Credible reports suggest that Mali-based jihadists have at times entered Senegal’s southeastern Kedougou region for refuge and resupply. Artisanal mining communities in the region are potential vectors for jihadist infiltration and expansion.

The government has been aware of the threat for some time. It has significantly increased its security presence in the region and increased public investment to address the economic causes of insurgency. The new administration has also instituted a ban on artisanal mining along the Falémé River on the Malian border in Kedougou, officially for environmental reasons due to spillover of toxic chemicals into the local river and water supply. However, the move also likely aims to reassert state control over a sector that could provide potential funding for jihadists.

Overall, the Senegalese state is significantly better resourced and capable than its Malian neighbor. This will play in its favor against jihadist ambitions. However, it may not prevent an insurgency from developing in the Kedougou or Tambacounda regions in the coming years, although such a prospect does not appear imminent.

Meanwhile, the terrorism risk in urban areas, especially Dakar, is currently limited. Regional jihadists have not showed much interest in targeting urban areas outside of the Sahelian states in recent years, although this is always subject to change.

Meanwhile, the government appears to have made progress with remnants of the decades-old separatist rebellion in the southern Casamance region. If this continues, insecurity in that region could decrease further, improving local stability and economic prospects.

The risk in the coming months is extremely limited as long as Senegal remains within the CFA monetary zone, a currency pegged to the euro whose exchange rate is guaranteed by the French treasury.

Furthermore, the new administration is unlikely to move aggressively on its official ambitions to withdraw from the CFA. It has already walked back campaign declarations, now suggesting that any move away from the CFA would only occur in consultation with other CFA-zone member states. Faye's official program is also clear on both a multiyear timeline and its ultimate realization being contingent on fulfilling key macroeconomic criteria.

If this were done outside of a negotiated, well-telegraphed process, the short-term costs could be significant, and the new currency would likely suffer major depreciation in its early days. One potential warning sign of an abrupt departure from the currency would be a dramatic degradation of relations with Paris. Another potential trigger would be a decision by the regional central bank to devalue the currency significantly, something that has been discussed in recent years but evokes a traumatic 1994 devaluation that has left deep-seated social and political scars.

The likelihood of Senegal leaving the CFA zone will nevertheless grow over time. While this will increase uncertainty over monetary policy and capital flows, if well managed it could benefit the Senegalese economy.

So far, official statements suggest that the new administration will approach the question pragmatically.

Given Senegal’s generally neutral-to-Western-leaning international orientation and democratic governance, trade sanctions are also unlikely. However, the arrival of the Trump administration in the U.S. has introduced an element of uncertainty for all countries. A U.S. travel ban is certainly possible, although Senegal does not appear to be on the lists leaked so far.

The default risk in the coming months remains low, despite worrying debt levels. Planned austerity measures as well as aggressive efforts to raise revenues by expanding the tax base and boosting export revenues all signal the government’s commitment to fiscal probity, even if some of its goals may prove unrealistic. The IMF, which had suspended its program last year, is likely to reach a new deal with authorities later this year, which may reassure creditors.

On the downside, the government’s announced budgetary austerity clashes with earlier GDP growth prognostics; the current, optimistic IMF forecast is 9.6% this year. This would potentially fail to address the debt problem adequately in the medium term.

At the same time, expected new revenues from oil and gas fields may give the administration some fiscal space unavailable to other governments in a similar situation in the coming years.