Index trend

Previous Quarterly Editions

Expropriation Risk: 72 75 74 76 ▲Political Violence Risk:66 66 66 66 ►Terrorism Risk:63 66 66 66 ►Exchange Transfer and Trade Sanction Risk: 63 73 64 64 ►Sovereign Default Risk:74 65 65 65 ►

Overall Risk Temperature: 68 (Medium high 1) TREND ►

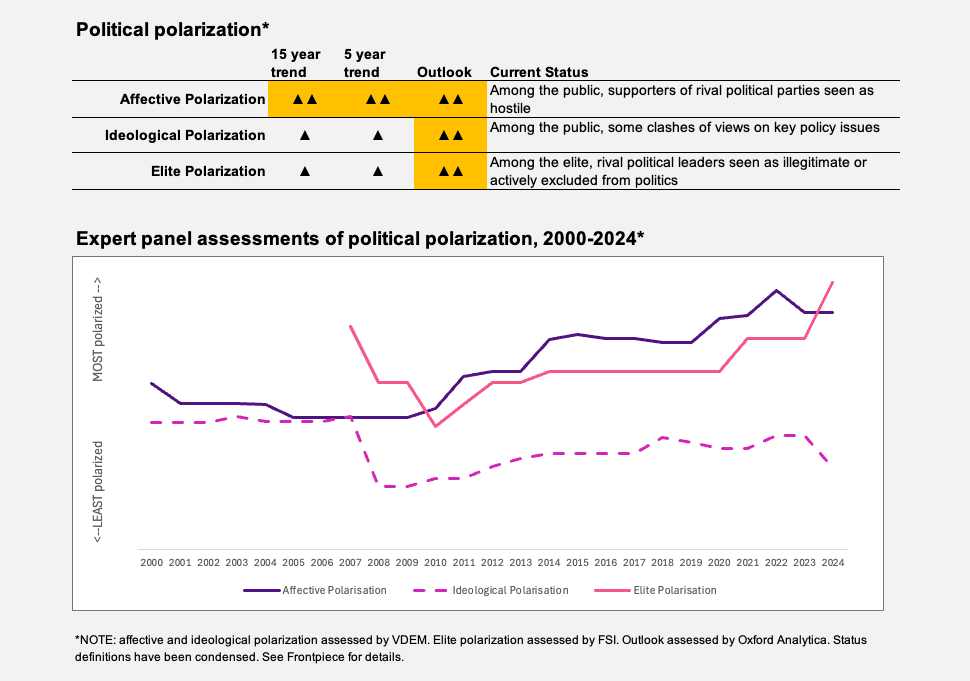

Special topic: Political polarization

Russia’s war against Ukraine has significantly polarized the country’s political landscape, but this polarization largely manifests itself outside of mainstream politics because of the repressive, authoritarian nature of President Vladimir Putin’s rule. While the ruling United Russia party benefits from the continued support of other parliamentary parties whose leadership rallied behind the Kremlin in February 2022, self-exiled opposition leaders oppose the war and consider Putin and his entourage to be war criminals. United Russia premises have been repeatedly attacked with Molotov cocktails, including in December 2024 in Arkhangelsk. More frequent attacks have targeted army draft boards across the country.

The polarization of attitudes within society exists not only with respect to the war itself but also toward returning veterans, many of whom are former convicts who were pardoned in return for agreeing to serve in the army. This cohort with a criminal past has an increasingly negative reputation. Since 2022, they have committed more than 240 murders, according to independent analysis. The government’s insistence on making them more visible, for instance by enacting university quotas in their favor or pushing them into local politics, only exacerbates tensions.

Frictions have been simmering even within the pro-war camp. In January, Zakhar Prilepin, a nationalist writer who in 2023 survived an assassination attempt by Ukraine’s security services, accused fellow ’patriots’ critical of Russia’s Soviet past of collaborationism with the West. This triggered a loud exchange of accusations and insults in the public space.

Significant polarization also exists between those who favor negotiations with the West and those who want Russia to liquidate Ukraine’s sovereignty. The former include a majority of young Russians, residents of large cities, most key businesspeople and liberal-leaning members of the political establishment. The latter include older citizens, people living in the provinces and members of nationalist circles.

TREND ▲

Since the invasion of Ukraine in February 2022, over 1,000 foreign brands have withdrawn from the Russian market, both voluntarily and under pressure from sanctions. In response, Russian authorities began to create obstacles for future withdrawals. All limited liability companies owned by non-residents from ’unfriendly nations’ are prohibited from disposing of their stakes in banks and energy firms without prior governmental authorization. The sale of Russia-based assets by such non-residents is contingent on a 50% or higher discount to the fair market value of the assets and payment of an exit tax.

In April 2023, Putin ordered the Russian assets of Germany’s Uniper and Finland’s Fortum to be placed under “temporary administration.” This was seen both inside and outside Russia as de facto nationalization. In July 2023, Putin ordered similar measures against France’s Danone and Denmark’s Carlsberg. In May 2024, Danone was authorized to sell its Russian business to a preapproved Russian investor. As Carlsberg followed suit in December with an orderly withdrawal from Russia, Putin ordered, the same month, that Belgian brewer AB InBev’s Russian assets be placed under the management of a local company set up only four months earlier.

The risk of outright expropriation of Russian assets remains high for all companies headquartered in any ’unfriendly’ jurisdiction.

TREND ►

The Russian invasion initially led to a wave of anti-war protests, resulting in the arrests of more than 12,000 people between the launch of the military campaign and March 13, 2022, when the protest movement fizzled under a severe crackdown. On March 4, 2022, Putin signed into law a bill criminalizing the spreading of ’fake news’ about the war and the Russian armed forces, with a maximum penalty of 15 years of imprisonment.

The authorities were somewhat taken by surprise in mid-January 2024 when several thousand people took to the streets in the southeastern territory of Bashkortostan to protest the arrest of a civil society activist who had been leading opposition to a local mining project. Detentions and criminal prosecutions ended the protest abruptly. Overall, the intensity of protest activity nationwide will remain low so long as the Putin regime keeps a firm grip on the sprawling security apparatus.

The government has continued to expand its foreign agents list, designating both natural and legal persons for allegedly receiving funding from abroad. Moscow has also pursued a head-on assault on domestic opposition and Western media, including social media. For instance, both Facebook and Instagram are banned in Russia, with their owner, Meta, having been designated an extremist organization. Last August, the Russian telecom regulator began throttling YouTube traffic in a bid to restrict access to critical video content.

There have been regular acts of sabotage and guerrilla warfare in the European part of Russia and Crimea, in addition to the shelling of the neighboring Russian regions by Ukrainian armed forces and recurring sorties into the same territories by the anti-regime, Kyiv-backed Russian Volunteer Corps. Since August 2024, parts of Kursk Oblast have been occupied by the Ukrainian military.

The Islamic State remains a moderate-intensity threat. There are frequent reports of arrests of alleged Islamic State sympathizers by the security services. March 2024 saw the second-deadliest attack in recent history, when a group of heavily armed terrorists rampaged through the Crocus City Hall in a Moscow suburb, killing more than 140 people and injuring more than 550. The attack was claimed by the Islamic State group, but Putin has blamed Ukraine, despite lack of evidence.

The invasion of Ukraine has led to imposition of unprecedented economic sanctions on Russia. This includes multi-jurisdictional freezes of the central bank’s overseas assets, restrictions on sovereign debt trading and bans on the sale of certain currencies to Russia.

Faced with an impending liquidity crisis, the authorities have enacted drastic capital controls. They froze withdrawals from foreign currency bank accounts above a $10,000 limit (last renewed until September 9, 2025), prohibited the transfer of foreign currency exceeding regularly updated thresholds, and allowed both sovereign and corporate debt to be paid in rubles. Since March 2022, the government has been collecting revenue from the sale of natural gas by Gazprom in Europe in rubles only.

Other Western restrictions include the disconnection of a dozen Russian banks from the SWIFT messaging system; U.S., EU and U.K. asset freezes on Alfa Bank, the largest private bank; U.S. blocking sanctions against leading oil producers Gazprom Neft and Surgutneftegaz; and an ever-expanding range of export controls, especially in relation to military technology and dual-use goods.

Since February 2022, the U.K., EU, U.S., Canada and Japan have frozen the Russian central bank’s foreign currency reserves held within their jurisdictions. Russia’s finance ministry estimates that some $300 billion has been immobilized out of the then total of $634 billion.

These freezes, in addition to the U.S., EU and U.K. prohibitions on the transfer of U.S. dollars, euros and U.K. pounds to Russia, prompted Putin to install stringent capital controls and to allow paying down both sovereign and corporate debts in rubles.

Although all three key credit rating agencies (Standard & Poor’s, Fitch and Moody’s) withdrew their Russia ratings in March to April 2022 because of Western sanctions, Moody’s declared Russia to be in default on its foreign-currency sovereign debt on June 27, 2022, for the first time since 1918.