Index trend

Previous Quarterly Editions

Expropriation Risk: 58 58 58 58 ►Political Violence Risk:74 79 79 79 ►Terrorism Risk:98 98 98 98 ►Exchange Transfer and Trade Sanction Risk: 64 73 73 64 ▼Sovereign Default Risk:74 74 74 74 ►

Overall Risk Temperature: 79 (High -2) TREND ▼

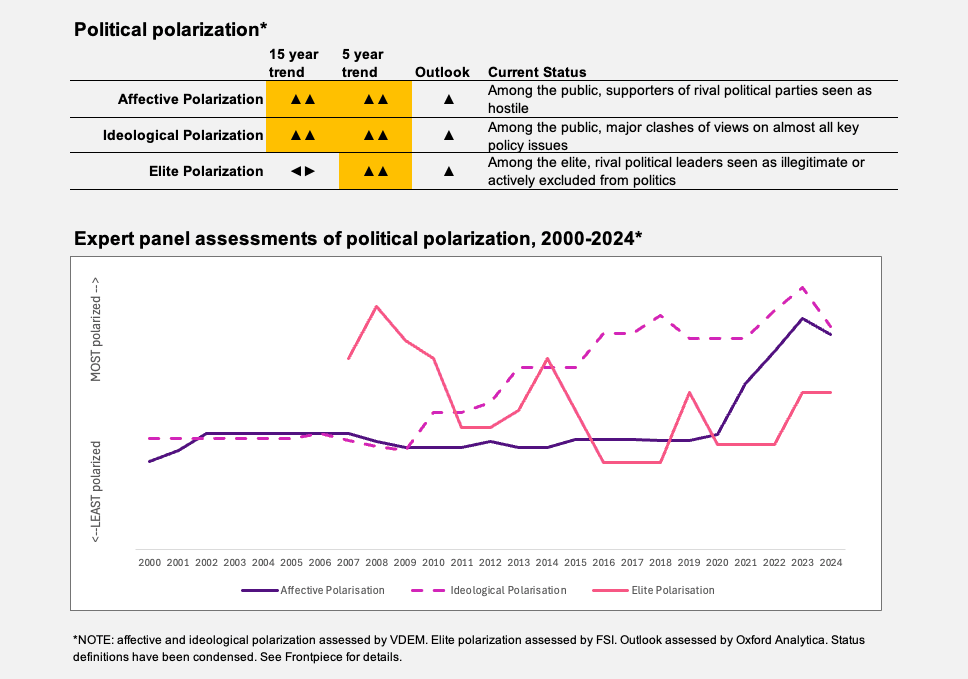

Special topic: Political polarization

Pakistan is experiencing severe levels of polarization, rooted in an especially bitter (and at times violent) confrontation between the civilian and military leadership on the one hand and the opposition and its supporters on the other. After Imran Khan was ousted as prime minister in a parliamentary no-confidence vote in 2023, he resorted to withering and personal public criticism of the Pakistani military — highly unusual in Pakistan. His large support base grew deeply critical of the military, leading to some of the most serious anti-military sentiment seen among the Pakistani public in decades, possibly ever. Violent protests against Pakistani military facilities following Khan’s arrest in May 2023 (another rare occurrence) sharpened this confrontation. An especially harsh crackdown ensued, which included targeting family members of Khan supporters — including female relatives.

The current ruling coalition in Pakistan is closely aligned with the military, and it shares the military’s enmity toward Khan’s Tehreek-e-Insaf (PTI) party. The parties leading this coalition, especially the largest partner, the Pakistan Muslim League-Nawaz (PML-N), have long harbored enmity toward PTI because Khan has reserved his harshest political criticism for PML-N. A key PML-N-allied party, the Pakistan Peoples Party or PPP, is another constant target of Khan and opponent of the PTI.

Khan bears some responsibility for this acute polarization: When he was prime minister, he refused to negotiate or compromise with the opposition (then led by PML-N and PPP). He rarely reached across the aisle, and he treated the opposition with contempt.

In Pakistan, coalition politics often prompt parties that dislike each other (including the PML-N and PPP) to work together nonetheless in order to hold a share of power. However, the current ruling parties want nothing to do with PTI, and Khan has long made clear he would never rule in a coalition with those two parties.

TREND ►

Though the political environment remains volatile due to an ongoing crackdown against the opposition and its supporters, expropriation risks are low in early 2025. This is mainly because the government badly seeks foreign investment to help stabilize a shaky economy, and so it would not do anything that could imperil existing investments. In early 2025, it stepped up efforts to attract new investments, both through existing mechanisms (such as the Special Investment Facilitation Council, a military-driven initiative that emphasizes attracting support from the Arab Gulf region) and new pitches (such as the announcement of new incentives for investors interested in exploiting Pakistan’s critical minerals).

The government showed little interest in policies that heighten expropriation risks. It has long been against nationalization of economic assets. On the contrary, it showed a growing desire to privatize state entities, especially its debt-ridden national airline. It also avoids populist measures meant to cater to public discontent about foreign investment, such as raising taxes on foreign businesses.

The one case where expropriation risks did exist was in Balochistan, a restive province with rising levels of militancy and terrorism, much of it directed against foreign infrastructure investment projects, most of which are sponsored by China. Balochistan is a shaky place for investors because of its political instability, and any foreign investor operating there would have faced the risk that unrest or the threat of it could slow down business activity and negatively affect profits.

The political environment was calmer in late 2024 and early 2025 than it was early in 2024, though this calm is deceptive. The civilian and army leadership intensified a deep crackdown on the opposition that made it difficult for opponents of the government to mobilize on the streets. For that reason, there were few large protests or demonstrations in major cities, and little political violence, even though Khan’s continued imprisonment angers his large support base.

However, the risk of political violence remains considerable in parts of Pakistan. First, anger at the state, and especially at the security force’s heavy-handed policies toward dissent, was especially strong in western areas of Pakistan, in Balochistan and Khyber Pakhtunkhwa provinces. These regions did have some large protests, with authorities cracking down with the use of force. These were largely in non-urban areas. In March, after ethnic separatists seized an entire train in Balochistan, Pakistan’s military announced that the “rules of the game have changed,” signaling a more muscular approach to targeting violent actors. In the past, Pakistani military operations under the guise of counterterrorism have targeted peaceful communities in areas with strong anti-state sentiment. This suggests there could be greater crackdowns in Balochistan and Khyber Pakhtunkwa that could produce more anger and resistance and a heightened risk of political violence.

The terrorism risk is now higher than at any time since 2014, when Pakistani counterterrorism operations degraded a potent Pakistani Taliban threat. The same group has made a comeback, buoyed by the safe havens it has enjoyed in Afghanistan following the Taliban takeover there in 2021. Data released in early 2025 showed an alarming rise in attacks. According to the Pakistan Institute for Peace Studies, the number of attacks in 2024 rose by 70% compared with the previous year. Most were in Balochistan and Khyber Pakhtunkhwa, though all four provinces suffered attacks. Additionally, the Institute for Economics and Peace’s Global Terrorism Index 2025 ranked Pakistan second among nations hit hardest by terrorism, with deaths from terrorism increasing by 45% compared with the previous year.

The Pakistani Taliban (TTP) is the most potent terrorist threat, but the big story in late 2024 and early 2025 was the increasing threat posed by Baloch separatists — mainly the Balochistan Liberation Army (BLA). The number of attacks staged by BLA and other banned Baloch insurgent groups increased by 119% between 2023 and 2024. In March, a group of loosely affiliated Baloch separatist groups announced they were forming a united new force called the Balochistan National Army.

Terrorist targeting patterns remained consistent with what has been seen over the past few years: Pakistani security forces have been hit the most, and mainly in western Pakistan (near the Afghanistan border) and in non-urban areas. Civilians were also generally not targeted. However, with the most potent groups increasing attacks and working more closely together, there is a strong risk that targeting could expand to civilians and to urban spaces across the country. After the BLA took an entire train hostage in March, the government announced that it would go harder after terrorists. However, limited economic resources and the lack of a political consensus make a full-fledged, nationwide counterterrorism operation unlikely.

TREND ▼

Although falling inflation, a cautious easing in interest rates and a thin rebuild of foreign-exchange reserves have bought Islamabad breathing room, any fresh squeeze on those buffers could see the authorities revive the ad hoc capital controls and import restrictions they used during the 2023 crisis, again trapping foreign profits in-country and using trade rules to conserve hard currency.

Lower inflation, replenished reserves and a stabilizing currency prompted the government to claim victory for macroeconomic stabilization after Pakistan’s economy nearly defaulted in 2023. However, most of these improvements can be attributed to large infusions of funds from the latest International Monetary Fund (IMF) package and other donor assistance. Structurally, the economy remains shaky.

Decreased inflation was a bright spot. After peaking at 27% in August 2023, consumer price inflation fell to a nearly 10-year low of 1.5% in February this year, due in part to higher agricultural output and lower global commodity prices.

Pakistan’s State Bank lowered interest rates several times last year, an indication of its confidence that inflation is more under control. However, in March this year, after six consecutive cuts, it decided to keep the main rate the same at 12%. This was likely due to continued challenges — debt, high costs for some key foods and fuels, and still-precarious foreign reserve supplies — as well as the global economic uncertainty and volatility prompted by the policies of the Trump administration in Washington.

Pakistan’s debt and liabilities continued to mount, part of an ongoing pattern. Government statistics announced in February showed that they increased nearly 8% during the first quarter of Pakistan’s 2025 fiscal year (July – September 2024) compared with the same period of the previous fiscal year. This came after an 11% rise by the end of June 2024 compared with the fiscal year prior — to the tune of $130.5 billion, an increase of $4.4 billion from the previous fiscal year.

Export performance was a bright spot. Exports of apparel — part of Pakistan’s largest and most globally significant export industry — enjoyed 19% growth over the first eight months of the current fiscal year (July 2024 – February 2025). Textiles and apparel more broadly grew 9.3% over the same period. However, this strong performance did not prevent a significant widening of Pakistan’s trade deficit, which increased 35% in December 2024 after some long-standing import restrictions were removed. This higher trade deficit underscored the risk of Pakistan maintaining a non-diversified export economy: Textiles dominate its export base, and with few other products to supplement this, the economy is vulnerable to higher trade deficits even when export performance is strong. A persistent trade deficit would lead to a depletion of foreign exchange reserves, making it challenging for Pakistan to meet its external debt obligations.

Still, overall, Pakistan’s default risk is relatively low, compared with several years ago, thanks in great part to large infusions of external financing (headlined by the latest IMF package) and robust remittance flows, which rose 25% year-on-year in January.