Index trend

Previous Quarterly Editions

Expropriation Risk: 46 46 46 45 ▼Political Violence Risk:49 49 48 48 ►Terrorism Risk:42 42 42 42 ►Exchange Transfer and Trade Sanction Risk: 55 55 55 54 ►Sovereign Default Risk:65 65 65 57 ▼

Overall Risk Temperature: 51 (Medium -3) TREND ▼

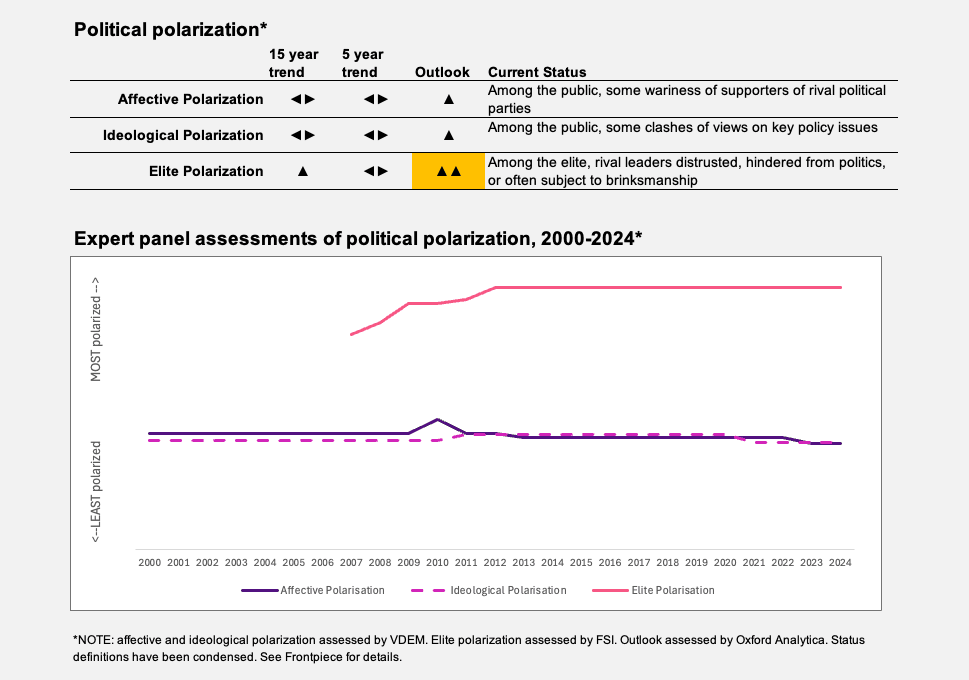

Special topic: Political polarization

The general election due to take place in September or October 2026 has brought the differences between Morocco’s competing political parties into focus. The ruling coalition of three parties that are close to the monarchy has held firm since the 2021 election, and the government was refreshed in October 2024 with an extensive reshuffle that was oriented toward consolidation ahead of the next election. These three parties hold 273 of the 395 seats, with the remainder held by leftist parties, smaller loyalist parties and the Justice and Development Party — an Islamist party that dominated Moroccan electoral politics for a decade before suffering a heavy defeat in 2021 when its seats fell from 125 to just 13.

The current coalition has a good chance of securing a majority in 2026, but this is largely thanks to its powers of patronage rather than any great popularity. Aziz Akhannouch, the prime minister, has built up one of the largest business conglomerates in Morocco, and the sense of the country being run by oligarchs was strengthened when he brought one of his close business associates, Mohammed Saad Berrada, into the cabinet as education minister in the recent reshuffle. The government has also pushed through a new law on strikes that is favorable to business, although some concessions were made to opposition parties and trade unions during its passage through parliament.

The widening gap between this oligarchy and the other parties tends toward an increase in affective polarization.

The Justice and Development Party (PJD) has been revitalized by the return to its helm of Abdelilah Benkirane, a charismatic figure who served as prime minister from 2011 until he was effectively dismissed by the king in 2017. Benkirane has attacked the government for maintaining relations with Israel despite the war in Gaza, for awarding an offshore gas exploration deal to a consortium that includes Israeli companies and for conflicts of interest in the government. A specific instance was the award of a desalination contract to a consortium that included Akhannouch’s business by a panel chaired by Akhannouch.

The differences aired between government and opposition are similar to the trend of ideological polarization. Ideological cleavages relate to the role of Islam in society, Israel, inequalities of wealth and perceptions of corruption.

Elite polarization relates mainly to relations between the government and the palace — and affairs within the palace itself. King Mohammed VI remains popular, despite his frequent and prolonged absences from Morocco. His son, Crown Prince Moulay el-Hassan, is assuming an increasingly prominent role. As the election approaches, there will be maneuvering within the political and business elite to secure the approval of the king.

TREND ▼

Morocco has successfully courted foreign investment for years, including incentives such as preferential taxes and special investment zones. Foreign investors are typically induced to establish partnerships with interests connected to the palace.

In 2019 Morocco published a new model bilateral investment treaty (BIT). This includes protection against direct or indirect expropriation, although it does provide some leeway for regulatory interventions that could be interpreted as indirect expropriation. Two treaties have been signed under the model, with Brazil and Japan. The treaty with Japan took effect in April 2022, while that with Brazil was ratified by Brazil’s senate in August 2024.

There are no restrictions on companies divesting and selling their stakes to third parties. The government is enacting reforms to simplify the corporate tax regime, in phases up to 2026. This includes applying a standard rate of 20%, rising to 35% for annual earnings of over 100 million Moroccan dirhams ($10.6 million).

Businesses can run into difficulties during periods of political tension between their home government and Morocco, usually over the Western Sahara sovereignty controversy. However, disputes that have arisen between the Moroccan authorities and foreign investors have tended to be based on commercial rather than political issues.

TREND ►

The main source of political violence is the protracted conflict over Western Sahara between the Moroccan government and the pro-independence Polisario Front. Tensions have risen as Morocco has increased its diplomatic efforts to resolve the sovereignty issue in its favor and deployed troops within a buffer zone along the Mauritania border. There have been sporadic attacks by Polisario fighters against Moroccan government-controlled areas in Western Sahara. In October 2023, an attack on the town of Es-Semara resulted in civilian casualties. This appeared to mark a shift in Polisario tactics, as the group has tended to focus on military targets rather than urban areas. The Polisario Front has drawn encouragement from the increase in anti-Israel sentiment around the Middle East and Africa, as this has put Morocco’s relationship with Israel in a negative light.

The dispute is a major source of tension between Morocco and Algeria, but the risk of this escalating into conflict is low, despite occasional belligerent rhetoric from both sides. Morocco has recently taken steps to bolster its military preparedness for any conflict through requesting $524 million worth of weapons from the U.S., including 18 High Mobility Artillery Rocket Systems (often termed HIMARS). The deal was approved by the U.S. State Department in April 2023, and the HIMARS contract was awarded in mid-2024 to Lockheed Martin, with a 2026 completion date. Morocco enjoyed good relations with the first Trump administration, which led to formal U.S. recognition of Morocco’s claims on Western Sahara, linked to Morocco establishing formal relations with Israel. This close relationship is likely to develop during President Donald Trump’s second term.

Within Morocco, there have been sporadic popular protests against corruption, police brutality and deprivation. The king has also been criticized for his prolonged absences from Morocco. He made a rare public appearance in September 2023 after an earthquake that left more than 3,000 people dead and hundreds of thousands homeless, but it took him more than a day to respond to the disaster. This raises questions about a political system that is so heavily reliant on a remote monarch for important decisions. However, the risk of an insurrection against the monarchy remains low.

Morocco was one of the main sources in North Africa of fighters who joined the Islamic State in Syria in 2013–2017. An estimated 3,000 Moroccans joined the Islamic State, most coming from areas in the north known for Islamist militancy. There have been concerns that many of these fighters would return to Morocco and become involved in terrorist activity. However, there have been only a handful instances of Islamist terrorism in Morocco since Al-Qaeda carried out a major assault in 2003, and the risk of terrorism remains low. This is partly because of setbacks for the Islamic State and Al-Qaeda but also thanks to the effectiveness of Morocco’s intelligence services.

There are no significant restrictions on exchange transfers in Morocco. Access to foreign exchange through the banking system is straightforward, although the central bank does maintain some capital controls.

The exchange rate is pegged to a basket weighted 60% to the euro and 40% to the U.S. dollar. The band within which the rate may fluctuate was widened to 2.5% in 2018 and to 5% in March 2020. The International Monetary Fund (IMF) repeatedly urges Morocco to shift to a more flexible system. The central bank has agreed in principle, but there appears to be a residual reluctance to give up control.

The central bank has made relatively light use of its monetary tools to dampen inflation, which reached a peak of 10% in February 2023 but fell sharply in the second half of 2023, reflecting lower fuel and food prices, and averaged just 0.9% in 2024. The central bank lowered its base rate to 2.75% in June 2024, with further cuts to 2.5% in December 2024 and 2.25% in March 2025.

The risk of trade sanctions applies mainly to goods exported from Western Sahara. The European Court of Justice (ECJ) is involved in prolonged deliberations over a Polisario suit against the European Union, including exports from the territory and its waters in its trade preference accords. A recommendation from the court’s advocate in March 2024 was welcomed by the Polisario, as it called for the suspension of an EU-Morocco fisheries accord to remain in place and for food exports from the region to be labeled as coming from Western Sahara. The ECJ issued its final ruling in October 2024, overriding objections from Morocco’s main European trading partners. Morocco’s free-trade agreement with the U.S. could come under scrutiny from the Trump administration, but it does offer opportunities for Morocco to increase its exports to the U.S. as other countries and trading blocs struggle with the imposition of high tariffs.

Sovereign default risk is low. Morocco’s total external debt stands at about 50% of GDP, of which public debt is just under 30% of GDP, according to the IMF. Total public debt, including domestic borrowing, is about 70% of GDP. The public debt includes a stock of about $13 billion in sovereign bonds. Positive market sentiment of Morocco’s default risk was reflected in the strong response to the most recent sovereign issue in March 2023, raising $2.5 billion. The total public debt service cost is a manageable 2% to 3% of GDP over the next five years. Morocco has a solid buffer of foreign exchange reserves, sufficient to cover about six months of imports, and its position has been further reinforced by a $5 billion flexible credit line from the IMF. Morocco’s trade deficit increased by 7.3% year on year in 2024, as increases in imports of capital and intermediate goods canceled out improvements in automotive and phosphate exports. Tourism revenue increased by 7.5% in 2024, and there was a 25% rise in gross foreign direct investment, which reached $4.3 billion.