Index trend

Previous Quarterly Editions

Expropriation risk: 45 44 44 42 ▼ Political violence risk:51 57 57 59 ▲Terrorism risk:44 44 44 44 ►Exchange transfer and trade sanction risk: 55 55 55 55 ►Sovereign default risk:74 74 74 74 ►

Overall Risk Temperature: 58 (Significant) TREND ►

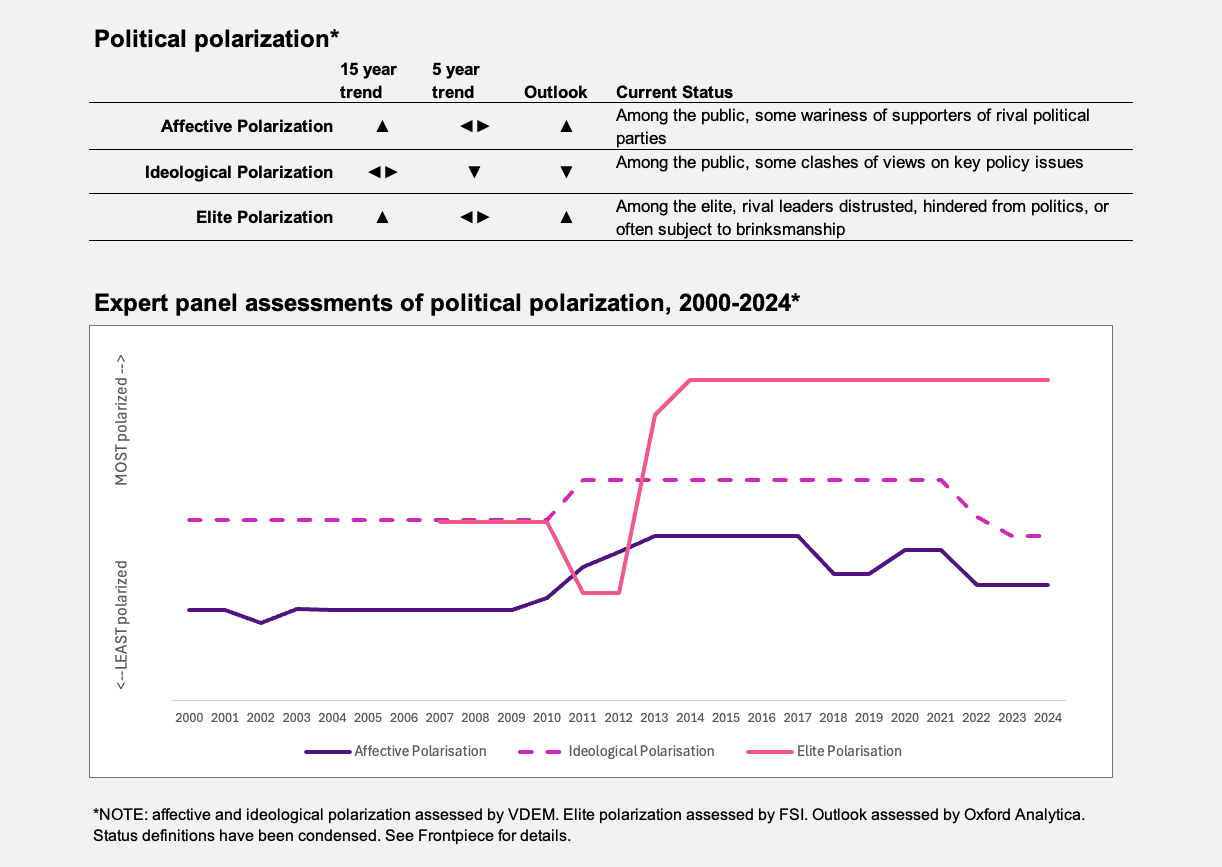

Special topic: Political polarization

Political polarization in Jordan is driven by deep-seated identity and loyalty-based differences rather than purely ideological disagreements. A significant fault line is the divide between citizens of Palestinian origin and those of East Bank Jordanian descent. This often influences political and economic debates (though it is less apparent at the elite level than among the majority of the population). There are also disparities between urban and rural populations. Ideological polarization between Islamists and secularists still exists, but is less central than in the past, as broader dissatisfaction with political and economic conditions has taken precedence.

The war in Gaza has unified all segments of Jordanian society in their stance against Israel, with broad consensus on the desire to revoke the peace treaty between the two countries — even though geopolitical realities and strategic interests make such a move unfeasible.

The key driver of political polarization in Jordan is the perception of unequal access to economic opportunities and political influence. East Bank Jordanians have traditionally held a dominant position in the public sector and security forces, while Jordanians of Palestinian origin have been more prominent in commerce and the private sector.

A rural-urban divide also exists, where rural tribal communities benefit from state patronage while urban populations struggle with underrepresentation. Economic pressures, particularly rising unemployment and inflation, have intensified grievances, reinforcing the notion that political favoritism shapes access to opportunities.

Further polarization is evident in tensions between the monarchy and government elites as well as opposition forces — including the Muslim Brotherhood and other reformist movements — who accuse the government of resisting meaningful political change.

Polarization is a growing topic of discussion in Jordan, particularly as protests and public discontent over economic and political issues have increased in recent years. The government’s approach to managing dissent — through accommodation and repression in parallel — has contributed to mixed trends in polarization. On the one hand, periodic crackdowns on opposition figures and activists deepen resentment and reinforce divisions. On the other, government efforts to engage in limited political reforms, such as adjusting election laws and expanding political party participation, signal an attempt to de-escalate tensions. However, these reforms often fall short of public expectations and contribute toward deepening distrust in political institutions. This is reflected in low election turnouts and in recent polls that indicate that trust in political institutions has declined significantly since 2010, when 72% of respondents indicated confidence in political institutions. While public confidence in the government has risen from 31% in 2022 to 39% in 2024, indicating a modest recovery, overall trust in institutions remains well below the 2010 level.

Polarization in Jordan poses potential risks to political stability, particularly as economic grievances and governance concerns deepen public dissatisfaction. While the monarchy has historically played a stabilizing role, growing divisions — whether along economic or political lines — could weaken trust in institutions and fuel unrest. Increased polarization also hinders political reform efforts, as factions struggle to find common ground on key issues such as electoral laws and economic policies. Heightened political divisions could make it more difficult for the government to implement necessary but unpopular economic measures, increasing the likelihood of protests and social unrest.

However, while economic hardships and political stagnation fuel divisions, there is also an undercurrent of pragmatic ‘depolarization,’ as many Jordanians prioritize stability over deep political conflict. Unlike in neighboring states, where polarization has led to outright political crises, Jordan’s monarchy has maintained a careful balancing act, managing opposition while preventing extreme fragmentation. Jordan’s history of controlled political discourse and the monarchy’s ability to mediate tensions suggest that while polarization presents challenges, it is unlikely to result in major instability in the near term.

The recent suspension of the U.S. Agency for International Development projects in Jordan, which previously provided approximately $1.2 billion (nearly 5.7% of government revenues) in non-military aid, including $770.9 million in direct budgetary support and $439.1 million allocated to development projects, threatens to strain the economy. This financial gap may heighten societal tensions, as Jordanian citizens face increased economic burdens associated with hosting refugees, potentially exacerbating polarization between local communities and refugee populations.

TREND ▼

The expropriation risk remains low. Investment law includes guarantees for national and foreign investors against expropriation. This includes stipulations that no economic operations can be expropriated directly or indirectly unless this is undertaken in the public interest and if investors are fairly and speedily compensated in a convertible currency. The only case where expropriation is likely is in the interest of national security, and this usually amounts to confiscation of land. There have been no expropriation cases affecting foreign investors in Jordan, at least in the past five years.

TREND ►

The pre-emptive strikes by the U.S. and Israel against Iranian nuclear capabilities may provoke Iranian retaliation against countries in the region. Israel is hardened against air assault, and Iran may wish to expend its dwindling supply of missiles against targets where its strikes will be more effective - both because these targets lack Israel's multiple rings of anti-missile defenses, and because most of these targets are closer to Iran, with proximity implying defenders will have less of a chance to respond. Iran's goal in this case would be to cause sufficient disruption to make the U.S. question its continued involvement in the conflict. These disruptive efforts could in the first instance involve efforts to close the Straits of Hormuz to shipping; possibly involve attacks on U.S. bases in Iraq, Jordan, Syria, Qatar, and elsewhere (although such attacks might provoke an escalation of U.S. involvement); and possibly involve attacks on oil and gas and other critical infrastructure in the wider Middle East, most likely in Qatar, Saudi Arabia, and the UAE (although such attacks would risk bringing other regional militaries into the war).

An increase in political violence in the coming months is likely, as discontent and protests in urban and rural centers rise across the country. These protests are driven by the deteriorating standard of living. The security forces will likely adopt a more robust response to protestors, which will lead to skirmishes and possible standoffs, especially in tribal areas.

There is a persistent medium-level risk of terrorism in Jordan, given the country's proximity to conflicts in neighboring Iraq and Syria, where terrorist groups such as the Islamic State, Al-Qaeda and Al-Qaeda-linked outfits operate. Moreover, Jordanian communities, notably in Zarqa and Maan, have hosted sympathizers who have joined and led terrorist groups operating in neighboring states and have themselves staged large-scale attacks in Amman.

The security forces have proven effective at mitigating planned terrorist attacks and benefit from efficient intelligence services, which operate in Jordan and are embedded in neighboring states. Nevertheless, terrorism continues to pose a threat.

The most recent major attack in Jordan occurred in January 2024, when a drone strike targeted a U.S. military outpost near the border with Syria. This attack, attributed to an Iranian-backed militia, resulted in the deaths of three U.S. soldiers and injuries to more than 40 others.

Jordan's liberal foreign exchange law entitles foreign investors to remit abroad, in a fully convertible foreign currency, foreign capital invested in Jordan, including all returns, profits and proceeds arising from the liquidation of investment projects. Non-Jordanian administrative and technical employees are permitted to transfer their salaries and compensation abroad.

The Jordanian dinar will stay pegged to the U.S. dollar. The large current account deficit will be partly financed by inward foreign investment, debt inflows and donor support. Foreign reserves are rising and in January 2025 amounted to $21.1 billion, which is equivalent to 8.3 months of current external payments. This should provide sufficient support to maintain the peg.

External conditions and political resistance to further austerity remain challenging. Despite recent tensions between President Donald Trump and King Abdullah II of Jordan — stemming from disagreements over Trump's proposal to relocate Gaza's Palestinian population — there is no clear evidence that these tensions have affected U.S. loan guarantees to Jordan. Jordan will retain U.S. loan guarantees and access to foreign borrowing at concessional rates from multilateral institutions and will be able to meet its repayments fully. However, it is constrained by wide fiscal deficits and high public debt.

Jordan's reopening of its border with Syria in 2021 and its call for other states to normalize relations with the Assad regime opened the kingdom to the risk of sanctions, especially as Syrian goods transit onward to the Gulf states. However, King Abdullah was careful to secure implicit support from the White House before reopening the border and assurances that the provisions of the Caesar Syria Civilian Protection Act of 2019 — which was initially set to expire on December 20, 2024, but was extended until 2029 — would not include Jordanian businesses or personnel. Given that the Caesar Act enjoys nonpartisan support in the U.S. Congress, Jordan will depend on both the White House and goodwill among its supporters in Congress to ensure that Jordanian businesses are not subject to sanctions. Since the fall of the Assad regime, Jordan's earlier push for regional normalization of relations with Syria has evolved into a pragmatic strategy to manage the post-Assad transition.

Meanwhile, the flow of narcotics, especially Syrian-produced Captagon, poses a significant challenge to Jordanian customs and immigration operating on the borders with Syria. The drug's penetration of Gulf markets means that it will remain a high-profile issue that draws the attention of U.S. policymakers and keeps Amman on the sanctions radar.

Although Jordan has rebounded from the adverse impact of COVID-19, the country's credit challenges are still pertinent, including high government debt and social pressures stemming from weak growth and high unemployment. These will continue to constrain Jordan's creditworthiness. However, the government's commitment to structural reforms and medium-term fiscal consolidation planning, alongside international support from the U.S. and Gulf Arab states — though both are less reliable than they once were — means that the positive outlook is likely to remain stable over the coming few years.

The current account deficit rose from 3.7% of GDP in 2023 to an estimated 5.7% in 2024 due to reduced proceeds from tourism and a decline in international phosphates prices; it is forecast to fall slightly to 5.5% in 2025.

In November 2024, Moody's reaffirmed Jordan's credit rating at Ba3 with a ‘stable’ outlook. This outlook is based on the government's commitment to structural reforms and its track record of effective implementation of fiscal reforms. The stable rating comes on the back of solid and credible policymaking institutions, along with strong international support and considerable domestic savings that together strengthen the economy in face of external vulnerability risks.

However, these strengths are offset by challenges such as high debt levels, structural barriers to growth, elevated unemployment, social pressures and volatile regional geopolitics.

Moody's predicts that the government's debt will decline to 80% of GDP by 2027–2028. The public deficit is likely to narrow because of sustainable revenue gains from tax administration-related reforms targeting increased compliance.

In May 2024, Fitch affirmed Jordan's Long-Term Foreign-Currency Issuer Default Rating at BB– with a ‘stable’ outlook. The ratings are supported by record gradual fiscal and economic reforms and resilient domestic and external financing linked to the liquid banking sector, public pension funds and funding from Jordan's external partners. However, the ratings are constrained by weak growth, monetary tightening, high unemployment and geopolitical risk, plus large external financing needs.

The conflict under way between Israel and Hamas has increased geopolitical risks due to the uncertainty surrounding the conflict's length and the possibility of further escalation. However, in the short term, these risks are offset by substantial international support, both multilaterally and bilaterally, including funding from Saudi Arabia, Canada, Kuwait, Germany, the U.K., the World Bank, the European Bank for Reconstruction and Development, and the International Finance Corporation, as well as reduced vulnerability to fluctuations in food and energy prices and potential supply chain disruptions.

Despite facing substantial external pressures, such as social unrest in the region and conflicts in neighboring countries (Iraq and Syria), Jordan has proved to be resilient in managing to maintain its economic and political stability. However, regional events have resulted in reduced economic growth and a significant increase in government debt. An extended or intensified conflict, even if Jordan remains uninvolved, could undermine the country’s growth prospects and amplify the challenges associated with fiscal consolidation.