Index trend

Previous Quarterly Editions

Expropriation Risk: 66 66 66 66 ►Political Violence Risk:66 66 66 66 ►Terrorism Risk:63 63 63 65 ▲Exchange Transfer and Trade Sanction Risk: 64 64 64 64 ►Sovereign Default Risk:65 73 65 65 ►

Overall Risk Temperature: 65 (Medium high) TREND ►

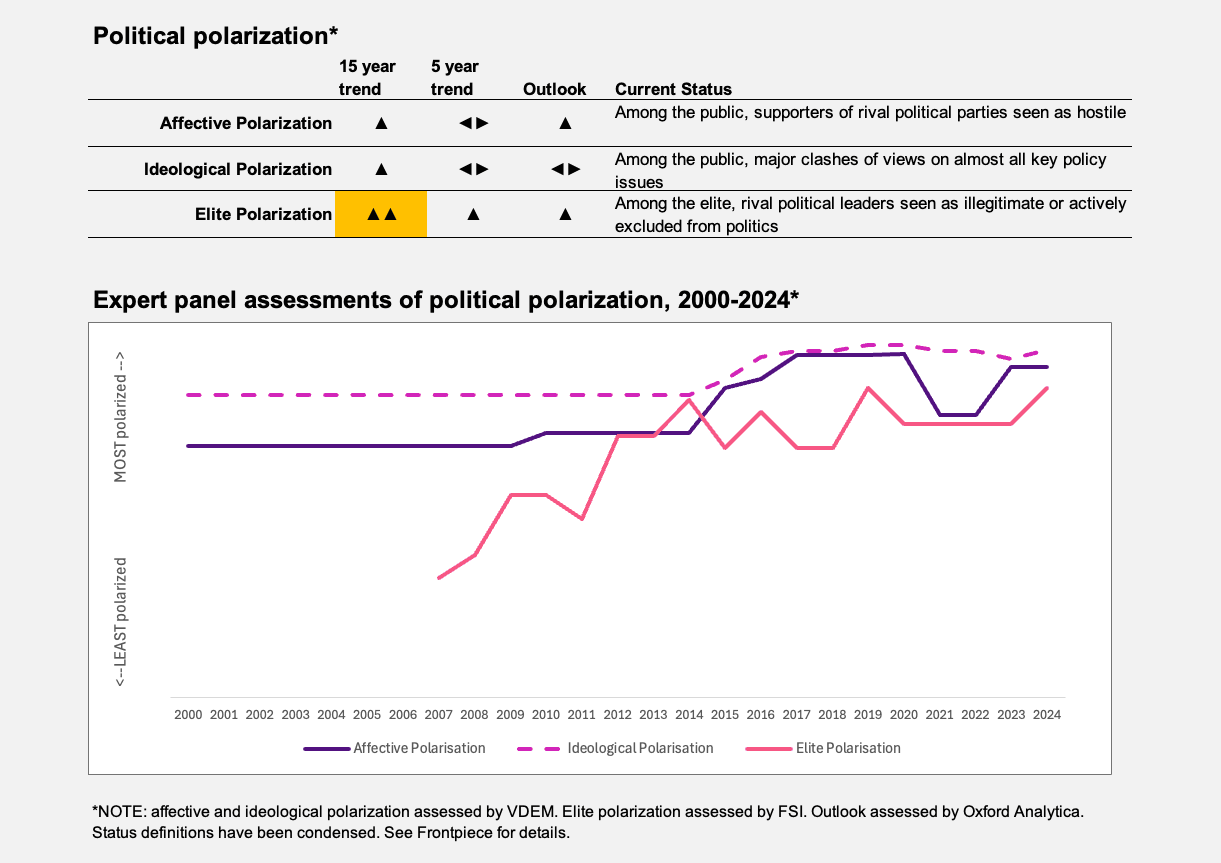

Special topic: Political polarization

Affective polarization in Cameroon has broadly been between the English-speaking minority, located in the south and northwest and the French-speaking majority who have maintained political and economic dominance since independence in 1960. Cameroon was administered by the U.K. and France after Germany’s defeat in the World War I. French Cameroon and British Cameroon merged as a single nation in 1961, but the two parts largely maintained the language and administrative systems of their respective colonial powers.

Unification has disadvantaged the English-speaking populations, who have felt marginalized, fueling political tension and agitation for independence for many years. This has culminated in an armed insurgency that began in October 2017 when Anglophone separatists unilaterally declared independence.

Alongside the Anglophone-Francophone division, polarization also exists between the predominantly Muslim north and the Christian south. However, President Paul Biya (a Christian southerner), who in 1982 took over from Cameroon’s first president (a Muslim northerner), has used co-optation to mostly neutralize the ethno-religious regional polarization. Moreover, Biya owes his longevity in office partly to his ability to keep a lid on elite polarization, though this is on the rise as factions within the ruling party maneuver to succeed him.

TREND ►Judicial independence in Cameroon is compromised by endemic corruption and political interference. According to the Corruption Index by Transparency International, 72% of respondents reported that corruption increased in 2024. In local courts, foreign investors are unlikely to secure victory over commercial disputes against a politically connected domestic investor or a government entity, due to corruption and political pressure.

By law, land can be expropriated for public utility, with compensation paid to the affected parties. An ongoing dispute between Cameroon and Sundance Resources over the Mbalam-Nabeba iron ore project highlights the risk of the government taking over concessions and reissuing them to other investors without full compensation.

TREND ►

Cameroon will hold presidential elections on October 5 this year. The 92-year-old President Biya has been in office for over four decades. He has yet to confirm whether he will seek reelection, but the ruling Cameroon People's Democratic Movement (CPDM) has reaffirmed support for him to seek his eighth consecutive term, despite concerns over his health.

Without a clear successor, a sudden departure from office by Biya would almost certainly trigger a succession battle within the CPDM. That could cause policy paralysis and severe disruption to executive branch operations. An uncertain transition could lead to a military intervention.

TREND ▲

Nigeria-based Islamist group Boko Haram and its offshoot, Islamic State of West Africa Province, continue to stage attacks in Cameroon’s north, where they have been waging an armed campaign since 2014. After a drop in attacks in 2022, last year saw a rise with an attack in August in Darak that left 12 people dead. In February 2025, the Islamist groups staged multiple attacks in villages, wreaking havoc and kidnapping. They have yet to expand their attacks beyond this region, posing limited threats to Yaoundé and Douala, the country’s political and commercial capitals.

In the south and northwest of the country, separatist militants are engaging in indiscriminate attacks on civilian, business and military targets. These attacks include theft of cargoes and burning public infrastructure such as schools, markets and post offices. These Anglophone militants appear increasingly to be copying Boko Haram’s tactics, including targeting school children; using improvised explosive devices; and kidnapping civilians, state officials and local businesspeople for ransom. Nonetheless, collaboration between Anglophone militants and Boko Haram remains unlikely because of their differing religious beliefs and ideologies.

Cameroon’s trade sanctions risk remains low. The risk would increase were the country to help Russian firms and individuals evade sanctions imposed by Western governments, but there are no indications of this, despite Biya’s rapprochement with the Kremlin.

In terms of exchange transfer risk, Cameroon is bound by the foreign exchange regulations and directives coming from the Bank of Central African States (BEAC). A foreign currency exchange regulation that took effect in 2019 has significant implications for commercial transactions and creates a variety of risks, including around onshore bank credit risk, exchange rate, convertibility and transferability. The regulation requires companies to seek authorization from the BEAC before opening offshore current accounts and to renew every two years the permission to maintain foreign currency accounts in the Economic and Monetary Community of Central Africa (CEMAC) region.

However, the central bank granted several concessions to resident companies operating in the mining and hydrocarbons sectors as the new foreign exchange regulation came into effect. These concessions significantly reduce the risk of capital controls and exchange transfer restrictions for the extractives industry — a major revenue earner for CEMAC countries.

For 2025, Cameroon plans to increase funds to settle outstanding public debt. The amount set aside is a 120% increase to that of 2024, indicating the government’s commitment to honor its debts, according to Finance Minister Louis Paul Motaze. The country’s economy is forecast to grow by 4% in 2025 with cocoa production rising by almost 7%, which will likely boost public revenue.

Cameroon’s focus for financing of infrastructure is China, the country’s largest creditor. So far, Cameroon’s public debt is among the lowest in the CEMAC region and is projected to remain below 45% of GDP until 2027, which is well below the limit of 70% set by the central bank of CEMAC.

Despite Cameroon’s low debt-to-GDP ratio, the country has missed a few small payments in 2022, 2023 and 2024, which indicates the underlying weakness in the country’s public finance management. Late payment to the European Investment Bank occurred in August and September 2023 but was not significant enough to warrant downgrading. In 2024, Cameroon was reportedly late in making external debt payments to one commercial creditor. Nevertheless, the country made a payment of 467 billion Central African CFA francs ($767 million, or 1.4% of GDP) of domestic arrears, further indication of the government’s commitment to honor its debts. The main threat to Cameroon’s debt repayment ability is the risk of political destabilization driven largely by the lack of a credible plan to succeed Biya in a country that has not witnessed a transfer of power in over four decades.