A different view of your insurance programme

These days data relating to many aspects of the performance of mining companies is widely available, but many miners miss the insight contained within the data and as a result make sub-optimal decisions. So how are leading mining companies combining data with focussed analytics and deep industry knowledge to view risk in a different way – resulting in better quality risk financing decisions?

Too simplistic? Traditionally, mining companies have insured their risk exposures on an individual basis with reliance placed on historical losses to assess risk, usually by considering each class of insurance in isolation. Premium, market capacity, deductible and insurable limit have been the main drivers, with only limited analytical decision support undertaken to assess placement outcome and pricing. But this single view of risk doesn’t take the true nature of risk into account, which is more complex; it also includes dependencies within and between risk exposures that can now be better understood by combining data with modern analytical capabilities.

Too complex? In addition to buying insurance as individual lines of cover, the various insurance lines are often bought with different renewal dates, with many local policies stretching across different geographies as well as varying levels of deductibles and limits. This complex structure of cover makes it difficult for key decision makers such as Treasurers and CFOs to understand precisely how their company is protected in the event of a series of losses, and as result may lead them to underestimate the true value of insurance as a hedge.

Differences from other hedging strategies This is in stark contrast to the value that mining companies perceive from transferring risk by purchasing hedges in commodity markets, interest rate and currency markets. Due to the binary nature of such structures (there is only a pay-out if an index or a currency falls below a pre-agreed value) they are often viewed by Finance functions as simpler to understand than insurance.

Moreover, layers of hedges across different risk types may be bought to protect the organisation from scenarios that are deemed too risky without transfer of risk to the external market. It is this simplicity that is regarded as particularly attractive by CFOs and Treasurers, compared to the perception that insurance is more complex to understand and hence use as a hedge for effective risk transfer.

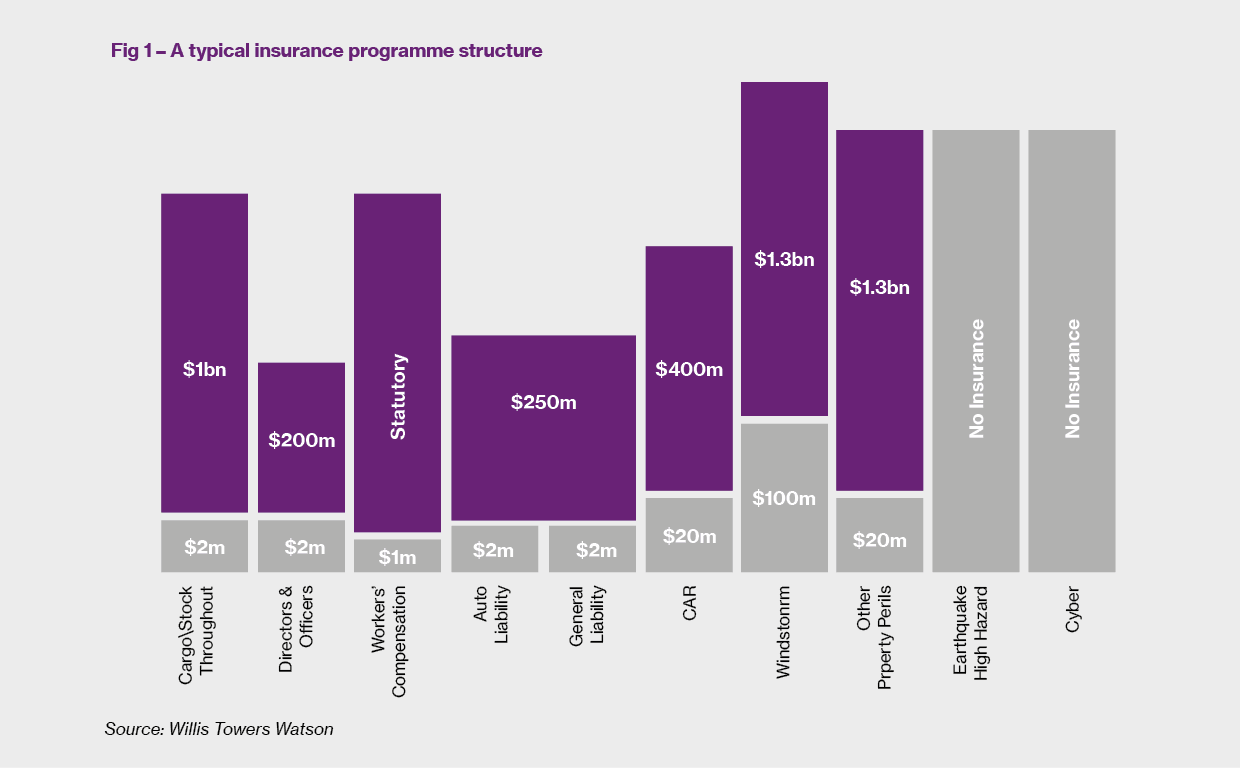

Common insurance structure How then should these different points of view be reconciled? A good place to start is a common representation of the insurance structure that is purchased by the organisation. The structure is often depicted as a series of bars or towers, where the height of each bar approximates to the amount of cover bought, and may look like this:

Does this structure work when the company is under stress? Whilst this depiction is helpful for understanding exactly what amount of cover has been purchased for each line of insurance, it is less helpful when seeking to understand the protection afforded to the organisation in times of financial stress. For this to become easier to understand, we need a different viewpoint.

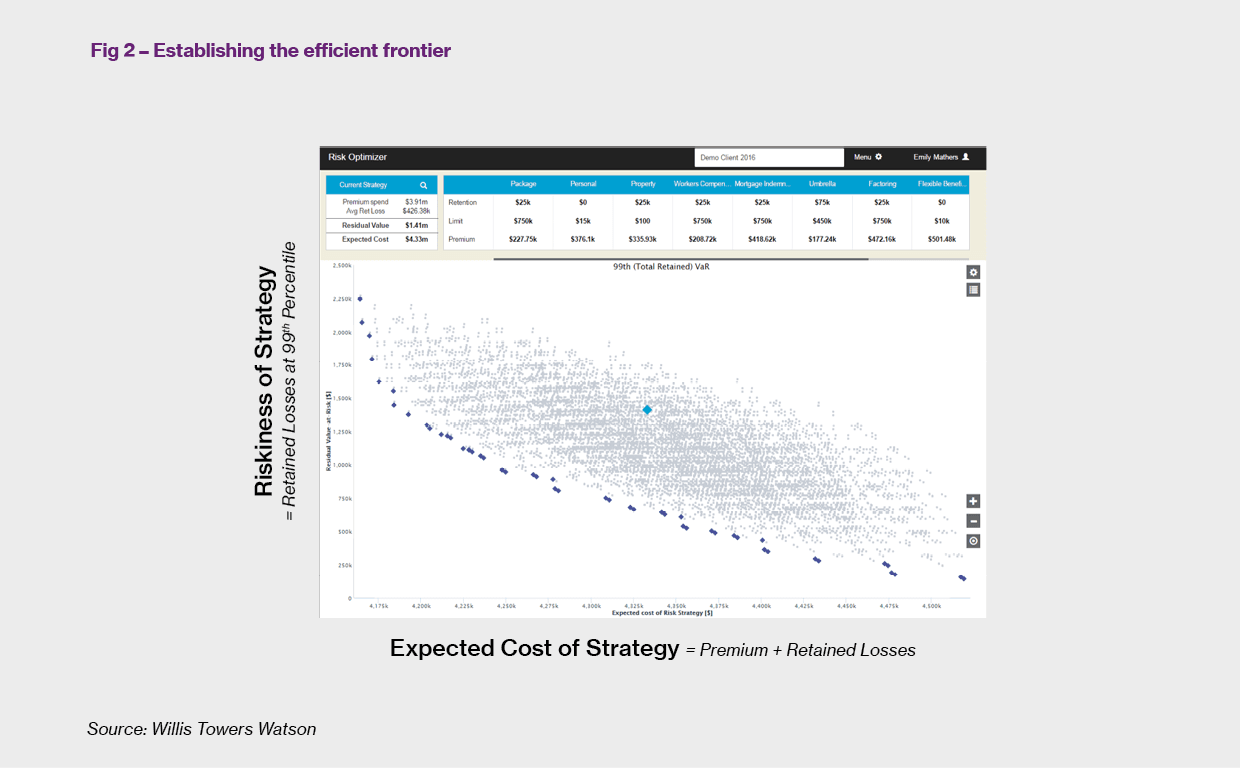

Retained risk and expected cost One viewpoint that CFOs and Finance teams will be familiar with is one that identifies the trade-off between risk and return. For our purposes we will amend this slightly to show the trade-off between retained risk and expected cost, as outlined in Figure 2 below. This view has been designed so that it is easy to see the merits of different financing strategies as well as their impact of the organisation’s bottom line.

The objective is to reduce the amount of retained risk and at the same time reduce the expected annual cost and move to a more efficient programme, closer to the edge of the cloud in the above diagram (in this example, the current strategy, represented by the blue diamond, is positioned way behind the “efficient frontier” and so can be significantly improved).

Towards the efficient frontier – and a better understanding of risk By combining data, industry knowledge and modern analytics, a better understanding of the company’s risk exposures and their variability may be obtained. This insight will often reveal a very different picture from the traditional siloed view of considering different classes of risk in isolation. A significant benefit of this approach is to show where concentrations of risk occur as well as where there are currently inefficiencies in the transfer of risk off the balance sheet.

Combining analytics with industry data to identify trade-offs As a result, many leading companies are now beginning embrace combining analytics with industry data to better understand risk at a portfolio level, and hence to understand the trade-off between the cost of retaining vs the cost of transferring risk.

This deeper understanding of the correlations of risk helps to identify ways to reduce volatility by measuring the effects of diversification and may be used to develop alternative strategies. These strategies may then be assessed and compared using the lens of riskiness versus expected cost shown on previous page.

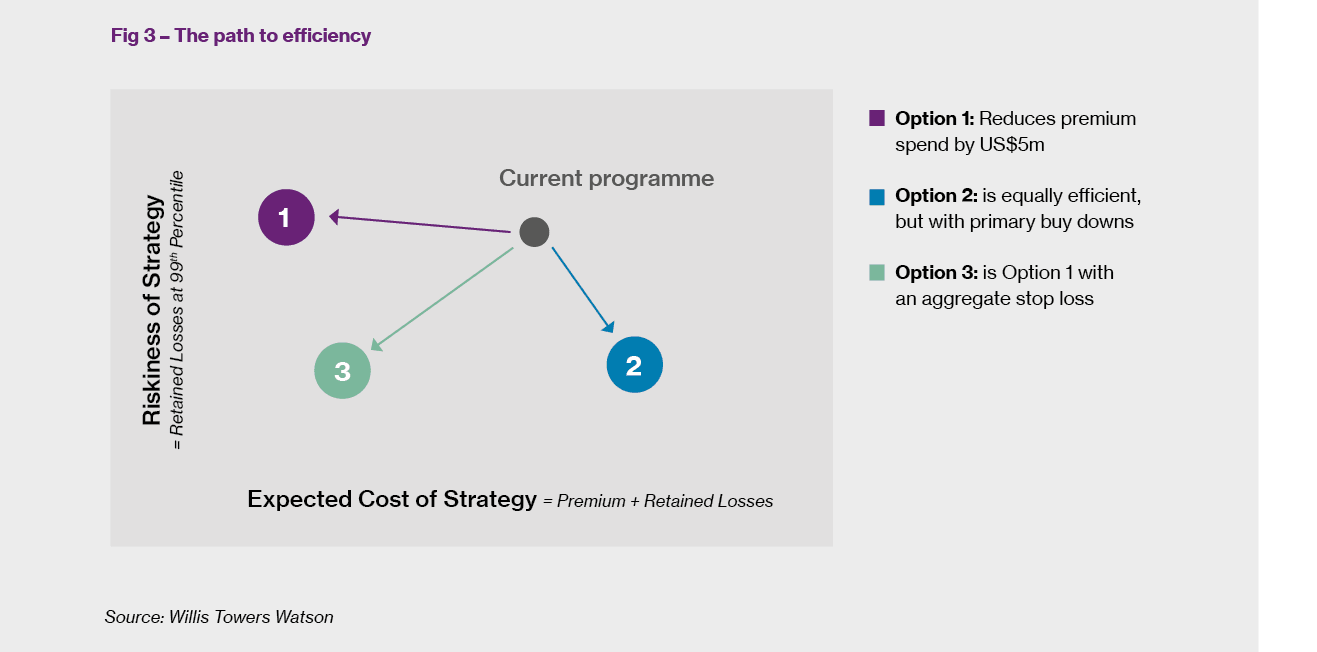

This path to efficiency was recently highlighted to a client in the following diagram and shows three different options, all of which are more efficient than the current strategy. They represent an annual cost saving to the company, as well as significantly de-risking the balance sheet at the same time.

Advantages of optimization The proposition for mining companies here is clear:

Methodology In practice, this is carried out in six distinct steps:

Developing tailored cover The increased availability of data and use of analytical methods is also leading to the development of alternative forms of risk transfer, such as parametric solutions, which can transfer financial volatility arising from weather related events or natural catastrophes away from company balance sheets. By understanding the variability inherent in risk exposures that are not necessarily insurable, it’s possible to use analytics to develop tailored cover based on measurable factors such as volume of rainfall, wind speed, footfall and temperature.

Decision making audit trail Another important benefit of using an analytical approach is the creation of an audit trail of decision making for risk financing. By considering current risk exposures, as well as the efficiency of both the existing risk transfer programme and of alternative structures, it can be shown that an objective and robust approach has been followed which takes both the interdependencies of risk and a consideration of the merits of different strategies into account before any decision is taken.

Benefits of this approach More generally, companies that use this approach find that they:

To conclude, a couple of recent examples will help to show the breadth of questions that can be answered by this approach.

Multinational mining company – retaining and optimizing risk Following a series of large liability losses, this client recently approached us with two critical objectives:

Dam owner - breach assessment We recently helped our client to better understand their Third Party Liability loss potential arising from a dam breach. This multi-disciplinary study, including hydraulic modelling, risk engineering and loss control approaches, provided a threefold benefit as detailed below:

Andy Smyth is Senior Partner in Willis Towers Watson’s Structured Risk Solutions division in London.