London insurance market update

Introduction: the origins of today’s market turnaround This time 12 months ago we described the mining insurance market for Property risks as being on the brink of hardening after 14 years of incessant softening of terms and conditions. However, at that stage in the market cycle we were not quite sure whether this hardening process would continue, or whether the continued overall supply of (re)insurance capital would eventually lead to a petering out of the process.

Perhaps, after 14 years of experiencing the same overall macro effect of (re)insurance market over-supply, we had reason to be cautious before we pronounced the end of the soft market. 12 months on, we now have no such qualms. During the last year a combination of factors has brought all sections of the mining market – the Direct and Facultative (D&F), major specialists and regional insurers – together in their determination to bring about a significant and permanent market turnaround.

What are the reasons for this turnaround, and what can buyers now expect from a market now buoyed by a renewed confidence that at last market dynamics are finally moving in their favour?

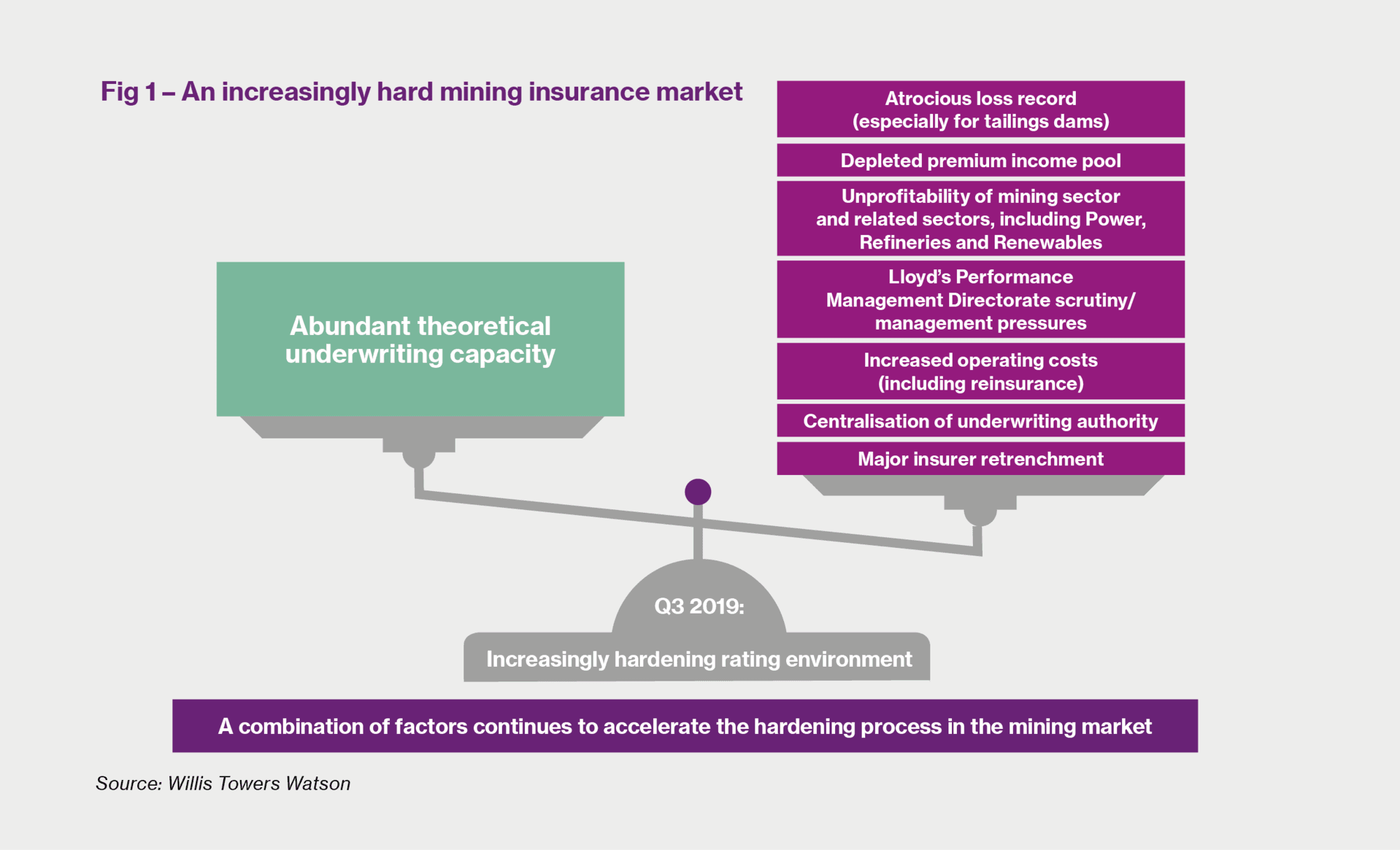

Figure 1 above shows how the balance of power in the international mining insurance markets has now tilted firmly in favour of the insurers. During the course of the last ten years or so, the continued provision of abundant capacity in the global Property & Casualty markets has created an advantageous market environment for buyers and their brokers. With a wide choice of insurers to choose from, each offering increasingly competitive terms to maintain and secure valuable premium income, buyers have been able to press home their advantage, forcing insurers to offer rating levels at way below what they regarded as the “technical” rates at which they could ensure underwriting profitability. Indeed, such has been the competition for some of the most valued business that underwriter “signings” for some placements (i.e. the different between their written and singed lines) have reached as far as 30% in some instances. However, as we alluded to last year, that rosy position for buyers has now turned around. Indeed, following the tentative rating rises achieved this time last year, underwriters are becoming increasingly confident of securing further increases as 2019 has progressed. Our schematic in Figure 1 on the previous page shows a combination of factors that has now changed the balance of power in the market. Let’s look at them each in turn.

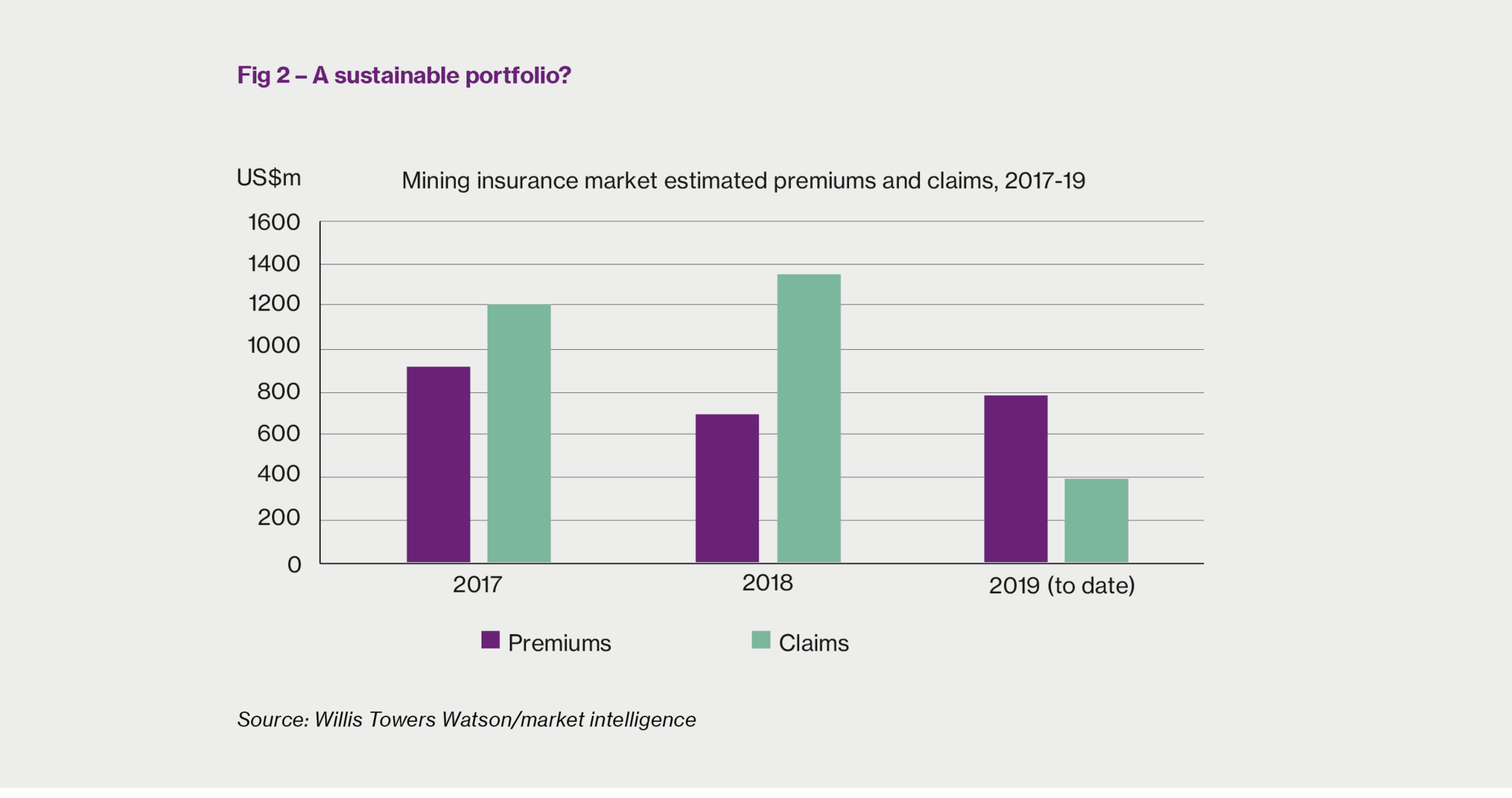

Premiums and claims – not a pretty picture Gathering precise data for the global mining portfolio is not an easy matter, as mining business is written not only in various regions of the world but also as part of a combined Heavy Industry/General Property portfolio. However, from our conversations with insurers and our own data we can determine a reasonable estimate of the total premiums and claims relating to the industry, and this is represented in Figure 2 above. Given that we are only just over halfway through 2019 at the time of writing, it’s not perhaps surprising that the claims reported to date only represent about 50% of the premium income. But if we look at the last two full years, a different picture emerges. In particular, 2018 is looking as if the market has sustained approximately US$1.3billion in claims, set against an estimated global premium income of approximately US$800 million, while 2017 is not looking much better.

So in terms of straightforward results alone, there has been plenty of incentive for insurers to increase their resolve to press for rating increases.

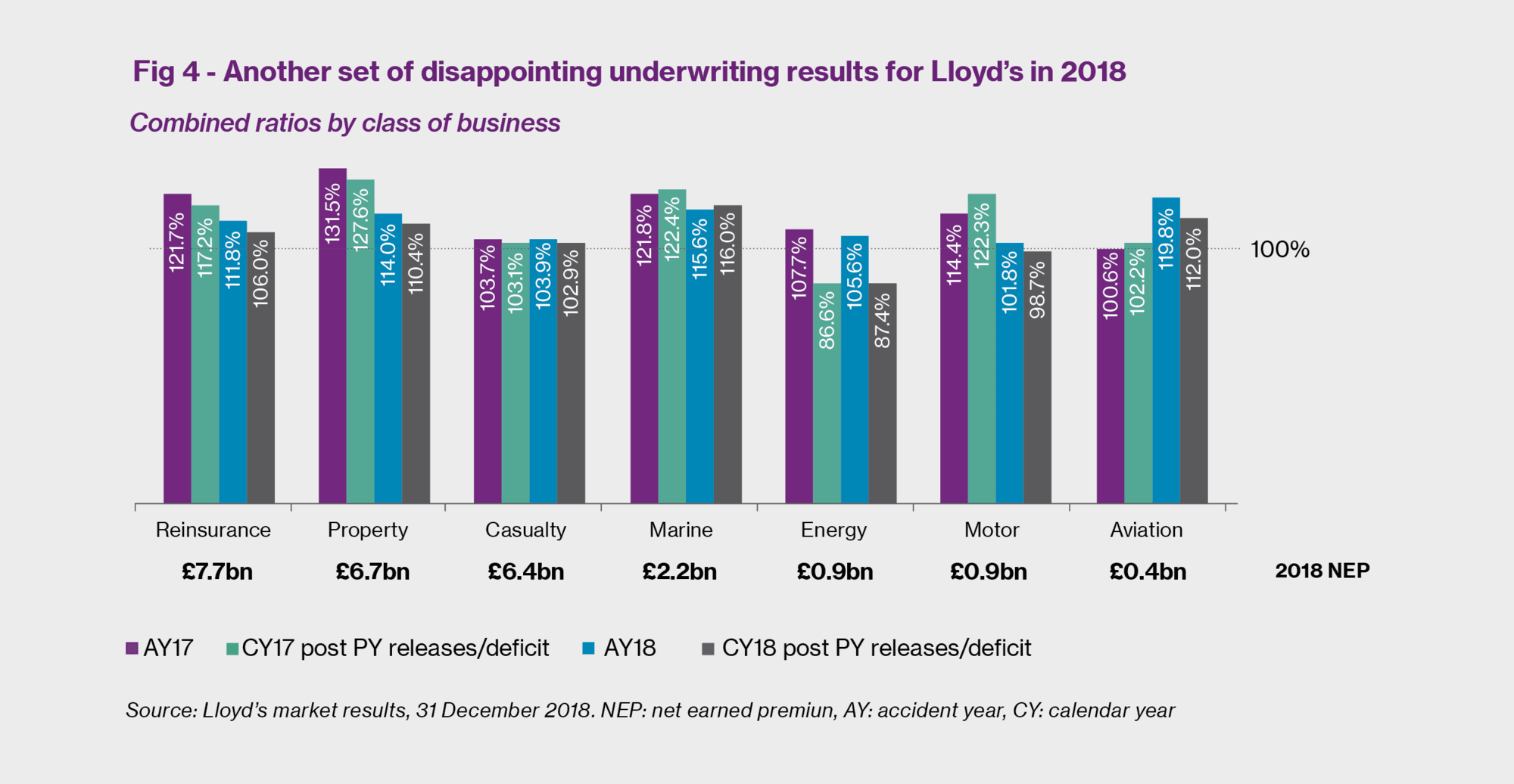

The Lloyd’s Decile 10 initiative But the mining loss record has not been the only driver for change over the course of the last 12 months; these results are reflected elsewhere in the Heavy Industry portfolio. Figure 4 above shows that the Mining portfolio in Lloyd’s of London is only one part of an overall negative picture for major Property risks of this type, including power, refinery and renewable assets. With a Combined Ratio (CR) of 110% for Property, and other classes also falling into unprofitable territory, only Energy (dominated by Upstream) recorded a favourable CR for 2018.

The recent Decile 10 initiative instigated by Lloyd’s management, prompted largely as a result of these figures, has ensured that a significant section of the Direct and Facultative (D&F) market has had no choice: either offer more improved terms from an insurer’s perspective or have your portfolio closed down by senior management.

Increased reinsurance costs Moreover, the availability of reinsurance protection for some D&F insurers has become increasingly restricted as this sector has become more unattractive to some significant Reinsurance markets from a strategic perspective. So with the reinsurance market as a whole tightening up, some insurers have now reviewed their mining portfolio and decided to withdraw from this sector completely, while others have been more circumspect and elected merely to cut back on their participation in this class.

Specialist mining market retrenchment But of course, it’s not just the D&F market that has been affected by the change in market atmosphere. The specialist mining market, including the likes of AIG, IMIU, Munich Re, SCOR, Swiss Re and Zurich, have conducted their own analyses of the mining portfolio and adjusted their own strategies accordingly. One major insurer has recently merged its retail and facultative operations into a single underwriting operation and we expect others to follow suit in the near future. This retrenchment has often resulted in the closure of regional offices around the world.

The most significant change in underwriting philosophy in this market has come from AIG; while in the past their strategy has been characterised by writing a significant - or even 100% - share of a given portion of the programme, we have now seen AIG cutting back heavily on such participations. Where this has not been anticipated by buyers and their brokers, it has led to some serious placement challenges, with brokers often having to supplement lost capacity with underwriting support from insurers at very different terms than had been negotiated the previous year. This has proved to be particularly challenging on excess of loss placements further up in the program which traditionally attract less premium income; while the more primary quota-share layers have usually had the benefit of a low signings “cushion” to offset any withdrawal of capacity, this has been much less the case for these higher placements.

Meanwhile, other specialist mining insurers have focused their attention on other specific underwriting issues, including tailings dams, underground exposures, Contingent Business Interruption, port blockage and critical natural catastrophe exposures. Indeed, some programmes would appear to have been significantly re-underwritten rather than simply having rating increases imposed on them.

The result of this retrenchment has generally forced buyers to consider alternative sources of underwriting capacity, allowing opportunistic insurers to provide replacement cover – at a price.

Centralisation of underwriting authority and the flight to quality As ever in a hardening market situation, we are finding that insurers are increasingly focusing on programmes featuring both quality risk management and significant premium income. Indeed, we can now say that a significant differentiation is now being made towards those buyers who have shown loyalty to a particular set of leading underwriters during the soft market years as opposed to these buyers for whom price has always been the strongest determinant in their purchasing strategy.

Another facet of an increasingly hardening market has been the increased centralisation of underwriting authority as insurers consolidate their portfolios and tighten their overall underwriting discipline. Especially among the major insurers from the specialist mining market, we are seeing a gradual withdrawal from certain regions and a tightening of underwriting control from the centre, whether that centre be located in London, Western Europe or North America. Moreover, any differentiation between insurers operating in this sector between those operating on a gross line basis (i.e. providing capacity on the back of reinsurance purchase) and those on a net line basis (i.e. underwriting without the benefit of reinsurance) is fast disappearing as at least one major (re)insurer is now augmenting their net line capacity with additional reinsurance purchase.

Withdrawal from certain territories At the same time, specialist insurers are differentiating against operations in certain territories. For example, following the destabilisation of the political situation in natural resource rich nations in central and southern Africa, insurers are showing a marked reluctance to continue to offer cover for mining projects whose viability is threatened by political unrest. Notwithstanding the political situation, insurers are also taking a dim view of both the loss record and the quality of risk management in some countries; this somewhat sudden change in underwriting direction has, in some cases, caught both buyers and their brokers off guard, requiring them to re-evaluate their marketing strategies and access insurers that has hitherto not been considered to be deployed on their programmes. Other territories such as Russia have also proved to be challenging, with AIG again significantly reducing their share on key programmes. However, an increased participation by local insurers has generally ensured that Russian programmes have managed to be placed without any significant negative impact.

Large global miners equally impacted The very large global mining companies would, on the face of it, have even more leverage with the insurance market, given the degree of premium income and global spread of risk that they offer. However, even they have found the new underwriting climate something of a challenge. For these major buyers, it has not been so much the rating increases which have been the challenge; it is also insurers’ relentless focus on the coverage provided in terms of retention structure and pricing caps. As a result, it would seem that they are likely in the future to retain an even greater proportion of their risk internally as they continue to develop their captive capabilities.

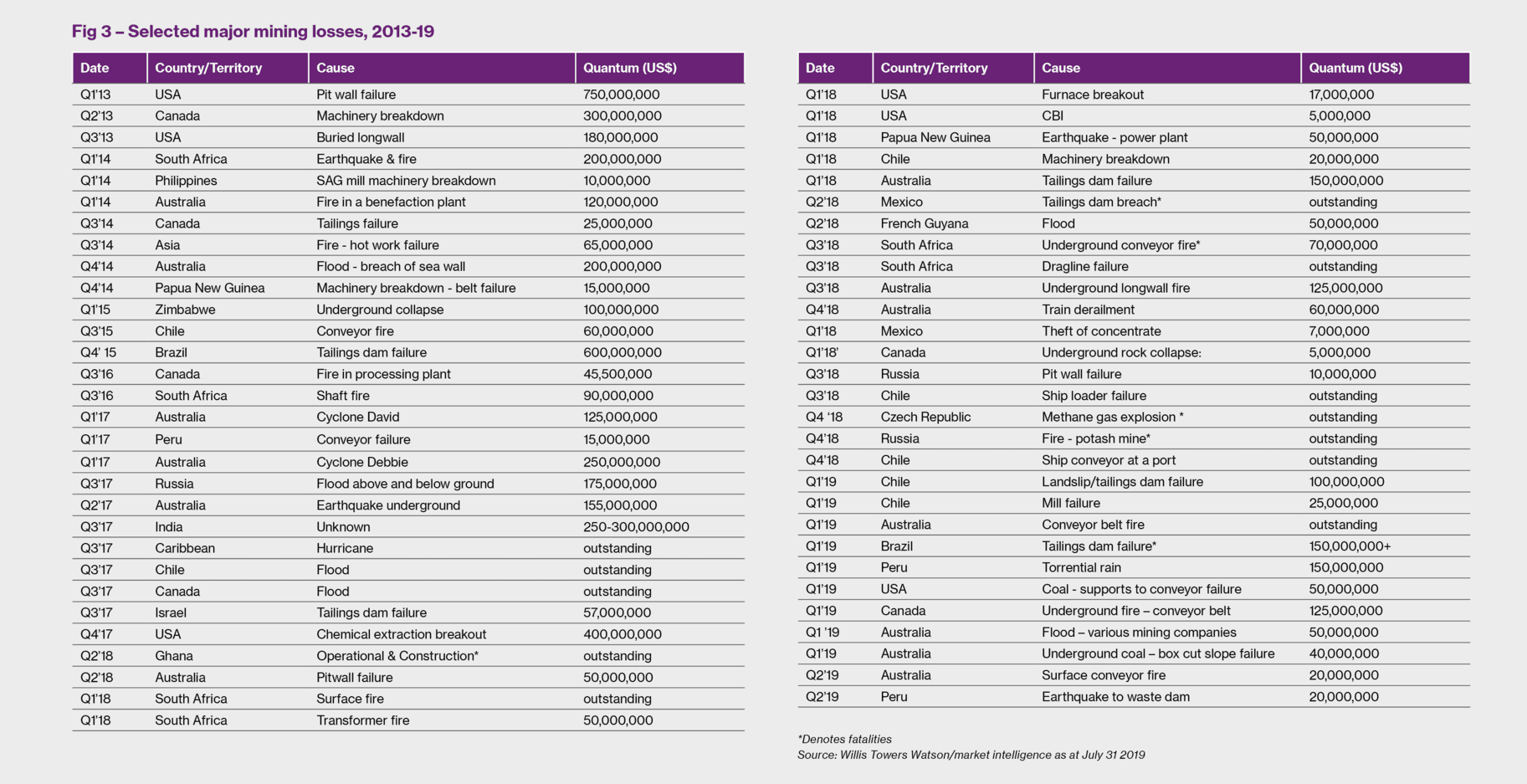

Tailings dams – the market imposes restrictive cover Of course, given the recent tragedy at the Brumadinho mine in Brazil, it’s not at all surprising that the issue of tailings dams continues to be the most contentious issue in today’s mining insurance market. Brokers and their clients now have precious little choice but to accept insurers’ tailings dam clauses, which defines what is and what is not covered by the policy in the event of a tailings dam loss. To begin with, insurers are now insisting on a declaration of values at inception and imposing an aggregate limit in the event of a loss by means of a non-stacking clause. This effectively prevents buyers from recovering secondary or tertiary damage to their own property further downstream from any tailings dam collapse as the aggregate limit imposed by insurers is likely to take into account only the value of the tailings dam itself. This of course means that in several instances it is likely that tailings dam owners will be faced with some uninsured exposure in the event of another major collapse on the scale of Brumadinho or Samarco a few years ago.

In any event, the significant programme limits enjoyed by some buyers at the height of the soft insurance market two or three years ago are very likely to become a thing of the past, if they have not done so already. Indeed, it is becoming increasingly clear that some mining companies will be shortly looking at gaps in coverage for this particular exposure – if they are not doing so already.

Conclusion: three pieces of advice So what advice can we give to mining insurance buyers, given this hardening market outlook? It’s true that this is not yet a truly hard market - there is still too much capital in play in the global (re)insurance markets for that. However, there is no doubt that those buyers (and their brokers) that were ill-prepared for the turnaround in the market over the last 12 months have either ended up with significantly more expensive insurance or with gaps in cover - and possibly an unattractive combination of the two.

Despite this, with proper planning and with the right long-term approach, much of the last minute “panic buying” that we have seen in the market over the last few months can be avoided. There are three pieces of perennial advice that in all but the rarest of cases should be taken to minimise the effects of the hardening market:

One thing is abundantly clear – those buyers who are forced to approach insurers with whom they have not been doing business for a number of years can expect a determined stance and perhaps some radically different terms than they might have expected in the past.

Chris Neame is Senior Vice President at Willis Towers Watson Natural Resources in London.

Rupert Bedford is Associate Director, Broking, at Willis Towers Watson Natural Resources in London.

Pascal Calmels is Executive Director at Willis Towers Watson Natural Resources in London.

Andrew Wheeler is a mining specialist and Client Relationship Director at Willis Towers Watson in London.

While the Mining Liability market was already showing signs of hardening as we entered 2019, it’s clear that the Brumadinho dam collapse on 25 January 2019 marked a notable change in underwriting appetite for the mining sector.

The overriding result has been a polarisation of the market, as insurers have either looked to reinforce their position as risk transfer providers for mining clients or pulled out of writing mining risks altogether. This dichotomy has effectively led to a quasi-specialist market, formed of insurers still willing to provide capacity for mining exposures.

Most significantly, the latest disasters in the mining sector have put Tailings Storage Facilities (TSFs) under the spotlight.

Three ways in which the market has changed In general, we can categorise the consequences of this development into three key areas:

Current underwriting drivers While Brumadinho can be recognised as the catalyst for change, there are many other factors contributing to the current dynamics of the Mining Liability market. For example, underwriters are analysing which territories are producing the greatest number of losses as well as considering which countries are enforcing the highest operational and maintenance standards. Consequently, there are regional implications to the current underwriting approach and the Law & Jurisdiction of a policy is of greater consideration to underwriters.

The type of dam construction has become a critical underwriting factor, with some markets unwilling to provide cover for TSFs built using the upstream construction method. In conjunction with this, underwriters are still seeking to ensure they understand Insureds’ joint venture operations, contractor management policies and underground mining exposures, as these remain pertinent from an operational point of view.

Reinsurance treaties are also playing a role in driving underwriting appetite and many (if not all) insurers have recently undertaken a thorough review of their mining books and TSF exposures. There is also a much greater emphasis being placed on company reputation. Notwithstanding the above, there is a growing tendency for underwriters to decline to review new mining risks citing a lack of time as insurers look to prioritise their underwriting focus on other target sectors. Moreover, there is a noticeable flight to quality business as the limited premium income available to Lloyd’s underwriters increasingly influences selection.

What does the future hold? In light of the discernible shift in market conditions, the value of long term relationships will become increasingly important for Insureds as those who nurture key underwriting relationships stand a better chance of limiting the effects of the hardening market. It is also likely that the fragmented nature of the current mining market will lead to an increase in differential pricing and therefore ‘split slips’, whilst at the same time, the reduction in market participants is likely to result in the emergence of recognised mining leaders within the market.

The withdrawal of capacity may also result in a renewal season where some Insureds are faced with the prospect of not finding 100% support for their programmes on a like-for-like basis and will need to consider either increasing their self- insured retentions in order to maintain existing limits in addition or reducing their programme limit altogether. Some Insureds may also be faced with the introduction of TSF exclusions on their policies where minimum information and/or risk quality standards cannot be met.

Another consideration for insurance buyers in the mining sector will be the developing mind-set surrounding ethical mining and the consequent withdrawal of capacity for certain coal mining exposures. Whilst this is particularly prevalent amongst the major composite insurers, Lloyd’s of London hinted that it may at some stage adopt a similar position when it confirmed last year that it would start excluding coal from its investment strategy.

A further final consideration is the impact of significantly restricted business plans that Lloyd’s imposed for 2019, as it is likely that syndicates’ ability to write new business will be significantly limited (if not non-existent) by the time we reach the latter stages of the year.

What does this mean for Insureds? The net effect of the above is that insurers are being very selective in the mining risks that they will consider and will only commit capacity where they can evidence internally that an Insured operates excellent risk management and that the chance of a TSF failure is extremely low. The corollary is that insurers are not hesitating to come off risks where best in class risk management cannot be evidenced, as restricted growth targets now mean that below-par mining risks are dispensable accounts from a portfolio perspective.

However, notwithstanding the various challenges and changing dynamics outlined above, the London contingent within the International Liability market still remains well-positioned to provide mining companies with insurance solutions - provided sufficient information can be furnished and adequate risk management demonstrated. However, in light of the palpable shift in market conditions, clients will need to ensure they appoint a broker with specialist Mining Liability market knowledge and experience, as this will be critical if their risk profile is to be adequately differentiated as part of their broke to underwriters. Only then will Insureds be able to obtain the best possible terms from what is ultimately a very challenging market.

Matt Clissitt is a Director at Willis Towers Watson Natural Resources London.

There has been a sharp rise in the number of shareholder lawsuits against public companies, emanating from the US in particular where securities class action filings are at an all-time high, in conjunction with an uptick in investigations. Global regulatory activity and country specific spikes in activity (e.g. Australia) has resulted in insurers experiencing increased claims activity involving fraud, bribery & corruption and concomitant civil, criminal and regulatory activity. In the UK there have been significant losses defending Serious Fraud Office (SFO) related claims - even where directors have been exonerated.

Also impacting the D&O insurance market is event-driven litigation, where plaintiff attorneys react to negative news by filing litigation; examples include cyber breaches, plane crashes and tailings dam collapses. When this constant trend of increasing claims activity and rising defence costs and settlement values since 2010 is taken in conjunction with decreasing premiums across the market during the same period, it is not surprising that a hardening insurance market has resulted.

There is a mix of both perennial and topical challenges facing the mining sector when it comes to liability insurance coverage for Directors and Officers:

Capacity changes Generally, there is still an abundance of D&O capacity in the insurance market; however, for mining companies in particular we must advise that there has been a significant reduction for 2019. Overall global ‘technical’ capacity remains just below US$1 billion, although there has been a significant reduction in per risk appetite. Available capacity depends on whether the company is public, private, and if publicly traded, the location of the listing.

Average rate changes In Q2 2019 the D&O rates increases have been most severe for US and Australian publicly traded companies, particularly those who have had losses and/or open claims. The mining industry across the globe has also been afflicted with significant rate increases.

Applying a significantly higher retention can help to mitigate premium increases. Alternative programme structures can also be considered, for example a Side A only programme, i.e. cover for non-indemnifiable loss for insured persons.

Common exclusions and limitations on cover As discussed, the D&O market has hardened considerably over the past year; this has also been manifested by insurers also looking at either excluding or sub-limiting areas of cover they perceive as potentially difficult. Virtually all D&O policies contain bodily injury and death exclusions, on the basis that these exposures ought to be covered by other insurances. An important so called “carve back” to this exclusion (i.e. granting of cover) is for defence costs for directors in respect of a claim made against them. Something which is sometimes more difficult to obtain, however, is the equivalent cover for legal representation expenses in the event of an investigation following an incident giving rise to bodily injury or death. Policies vary widely on the extent of this cover; some contain extensions for so called “corporate manslaughter” but again these need to be treated with caution, not least because in the UK the offence can only be committed by a company and the chances of an individual company director being successfully prosecuted for involuntary manslaughter are small. Also to be taken into consideration are the typical D&O exclusions for property damage and for pollution. In the case of property, insurers impose these on the basis that this insurance cover is provided elsewhere. With pollution, it is more often the case that insurers simply do not have the appetite to cover it all. While these coverage positions are clear, careful thought still needs to be given to the question as to how the exclusionary language is applied since there is a real danger that quite legitimate D&O claims will get caught up in the wording of these exclusions. For example, if a company suffers severe reputational damage, or its share price falls following a serious mining accident, it is highly likely that shareholders may seek to bring a securities claim against the company and its directors. Such a claim should be covered under a D&O policy and should not be restricted by the terms of any exclusion or other limiting language; this should be so regardless of whether property damage or pollution (as is highly likely) are also involved. More difficult coverage issues can arise in relation to other follow-on civil and criminal investigations and proceedings.

A focus on tailings dams After a few well-publicised recent disasters in which tailings dams have been implicated, D&O insurers have been seeking additional information and/or imposing additional limitations on cover in respect of tailing operations. Their starting point is that this is an additional “known risk” which they need to underwrite as, for example, trading in crypto currencies might be for a financial services company seeking D&O insurance. One of the challenges here is to identify precisely what tailings are for this purpose. Insurers are responding in varied ways to this new issue. Some are asking Insureds to complete detailed supplementary questionnaires; others are seeking to impose blanket exclusions or limitations, including a significant increase in the self-insured retention payable in the event of a tailings incident. To complicate matters further, any additional tailings related restrictions on cover have to be blended into and made consistent with the existing web of restrictions for pollution, bodily injury etc. referred to above.

Outlook Given the overall hard market conditions, it seems likely that coverage challenges of the kind summarised above will continue to feature in the renewals of D&O programmes for mining companies for some time. That being said, there is a strong case for seeking expert input and assistance from advisers specialising in this sector of the insurance market.

Mark Wakefield is D&O Practice Leader, FINEX Global at Willis Towers Watson.