The Australian market has seen a continuation of hardening conditions during the first half of 2020. Rate increases continue to accelerate to address premium adequacy across the mining portfolio as insurers seek to return to underwriting profitability.

Enforcement of underwriting guidelines In addition to this rating environment; coverage terms and conditions are being reviewed and certain coverages being tightened by insurers. There are additional levels of rigour in the review of individual mining operations with the enforcement of underwriting guidelines and multiple levels of internal approval required before capacity is offered. This has resulted in certain markets restricting line size or electing not to participate if they are unable to achieve the premium levels or terms and conditions that they require. Existing lines reviewed While capacity remains stable, insurers are reviewing their deployment to each risk; the exception being the continued constriction of capacity for thermal coal operations, with further insurer withdrawal from this area of the mining industry. Profitable hydropower portfolio For hydropower plants in China, total installed capacity was 310GW until Aug 2019, with no new large size hydropower projects being built in China during 2019. The Hydropower insurance portfolio’s profit was good in 2019, including the underwriting of both operational and construction phases with no large losses sustained.

Submission requirements Given the level of scrutiny of information in the current market environment renewal processes must start earlier than in past years and detailed submissions are required to achieve best results and demonstrate risk quality to insurers. The submission information now expected include:

Stephen MacDermott is Broking Director, Property and Casualty, Willis Towers Watson Brisbane. Stephen.MacDermott@WillisTowersWatson.com

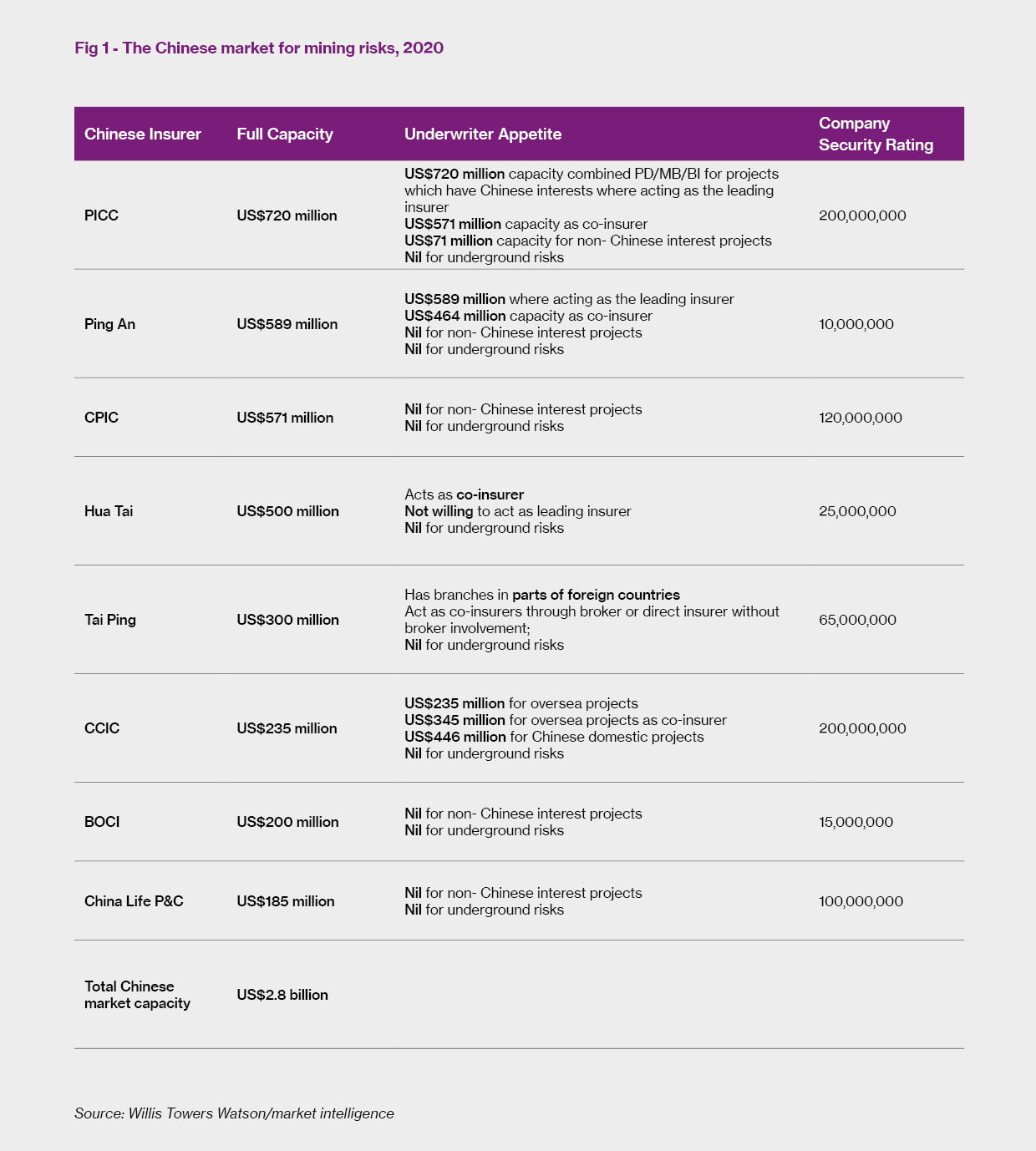

One Belt, One Road – Chinese insurers remain positive With the rapid development of Chinese enterprises purchasing overseas mining projects, most Chinese insurers are adopting a positive attitude to such business and expanding their capacity to take more market share. Most Chinese insurers pay a great deal of attention to mining business that has a Chinese interest, where Chinese enterprise ownership exceeds 50% or where it has management control for the project. For those projects which have no Chinese interest, most insurers refuse to write the share on a Primary basis but will consider writing a small line on an Excess basis. PICC is the major insurer that is willing to write non-Chinese interest mining business and others such as Tai Ping will follow. But most other insurers such as Ping An will refuse to participate on that basis.

No cover for underground risks, limited for Liability business Most Chinese insurers refuse to cover underground risks, no matter whether the project is located in China or overseas. Therefore, if there is a need to place underground risks, Chinese miners need to continue to rely on the London and the other international markets. Furthermore, most Chinese insurers have no capacity for Liability lines, including Primary General Liability, Excess and Umbrella. At present, we continue to refer Liability risks to the international / London markets to deliver placement solutions. Environmental Liability restricted to domestic projects For Environmental Liability risks, the Chinese market also refuses to consider overseas mining projects. However, most of the time for domestic mining projects, under from local government, the market players will combine and adopt an integration insurance model to take the risks. Furthermore, it can be deemed as compulsory environmental insurance in some special areas such as Shanxi and the Hebei province, where most mining projects are located. However, the limits of liability are very small (below US$1 million) as the co-insurers are not willing to write a higher limit. Using net retentions Recently we identified a new trend which is now ongoing in the Chinese market; even for those projects without Treaty support, Chinese insurers are still willing to write part of risk, relying on using their net retention to participate in the placement. Therefore, total capacity seems to be larger than before, so that the actual capacity is now equal to their Treaty amount plus their net retention. However, in actual practice insurers will not offer their full capacity, as they may be restricted by a number of factors.

Client perspectives From a client perspective, we found that most senior management pay attention to the following issues:

Fiona Pei is a mining specialist working for Willis Towers Watson in Beijing. Fiona.Pei@WillisTowersWatson.com

In South Africa, Emerald remains the main lead market with Hollard occasionally taking this position. Following markets such as Axxis, Old Mutual Insure and Inniu have been joined by Transition, Sintelum and Partner Risk. Property The South African Mining Property market continues to see an acceleration in rating increases, which is expected to continue to the end of 2020. Loss ratios exceeding 100% have forced underwriters to drive profitability; programmes below technical pricing or losing key capacity are seeing largest rate corrections, with coal risks experiencing 40%+ increases. Other commodities with average to above average risk quality are seeing pricing increases ranging from flat to +20%. Capital remains available, although insurers are reducing overall line sizes and repositioning deployed lines based on profitability, so capacity is available - at a price. The proportion of programmes with split placements has increased; worryingly, some underwriters are insisting on differential wordings. Underwriters continue to take a more critical look at exposures, restricting many coverage terms previously offered, such as coverage tightening on Extended Premises/Contingent Business Interruption extensions and are seeking confirmation that values at risk are up-to-date. Meanwhile, Silent Cyber and Contagious Diseases exclusions are being introduced, with Insurers adopting a non-negotiable position on exclusion wordings. Liability The Liability market in South Africa is hardening, particularly Excess Umbrella Layers. All Medical Malpractice cover, other than First Aid, is being deleted from combined programmes. Mining concerns with extensive medical facilities have been hit with a “double whammy” of significant increases combined with the cost of stand-alone Medical Malpractice that was previously included in the Liability premium.

Capacity remains available, although insurers are reducing overall line size and repositioning deployed lines. Some insurers are reducing capacity on offer regardless of pricing, while others are pushing for co-insurance rather than layering; hardly an ideal scenario for buyers. Underwriters continue to take a more critical look at exposures, restricting many coverage terms previously offered. Cyber and Contagious Diseases exclusions are being introduced, with insurers being non-negotiable on wording of exclusion, while the majority of local markets will not provide cover for tailings dams. Directors & Officers Liability South African D&O markets are seeking increases even on clean risks, with a minimum of 10% which can extend to beyond 60%. All insurers request primary prices before pricing excess; it is understood that the driver for this level of increase is often a combination of global reinsurers and the insurer’s parent company. Some insurers have begun implementing deductibles for side B, D and C where in the past no such deductible was applicable. Silent Cyber and Contagious Diseases exclusions are also being introduced. Excess layer insurers are sometimes not willing to follow form, and are imposing their own restrictions for their participation. Insurers are also implementing capacity reduction strategies, particularly on North America & Australian dual-listed entities, and even more so where there is an ADR exposure. Pressure has also been experienced on so-called “undesirable” business, e.g. Coal, while as reported elsewhere in this Review, global market appetite has shrunk as the market has hardened, which in turn is filtering through to the South African market.

Adrian Read is Industry Specialist Leader: Natural Resources, Willis Towers Watson South Africa. Adrian.Read@WillisTowersWatson.com