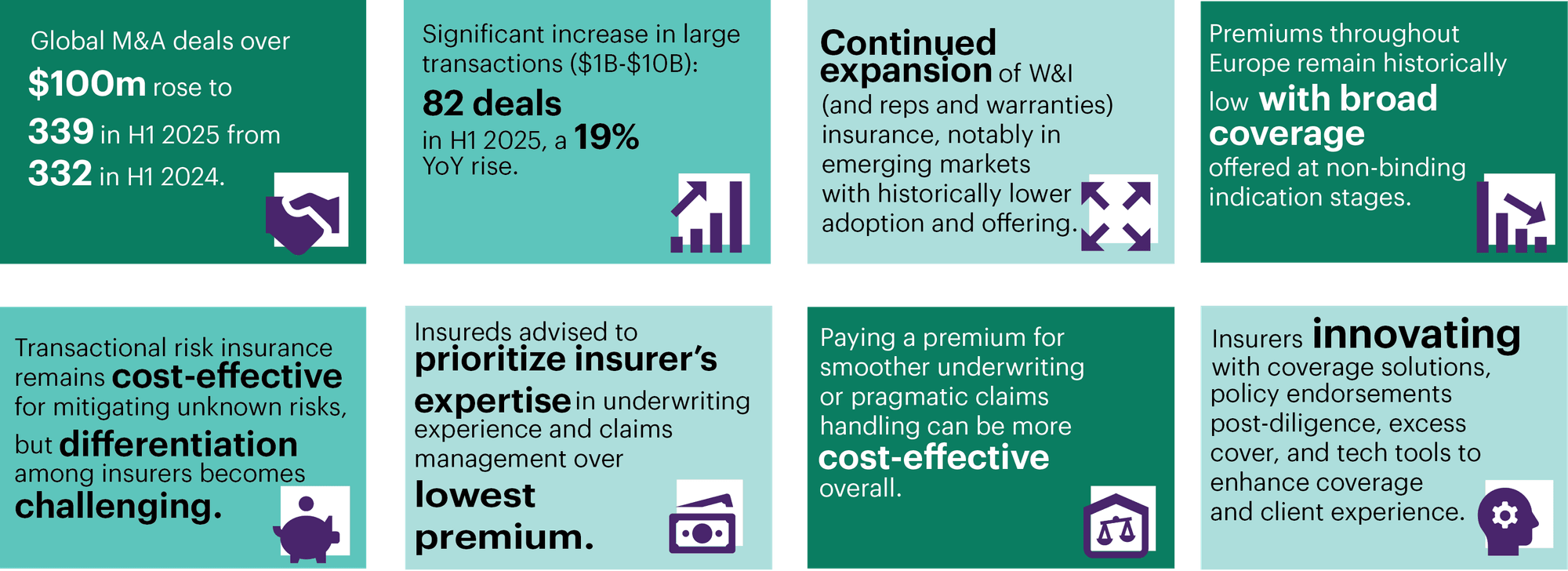

With premium rates at an “all-time low” and contemplated coverage at non-binding indication stage often already fulsome, insureds should look to their broker and explore with them the downstream impact of the key metrics which are often overlooked; namely underwriting experience and claims processes. After all, it may be more beneficial and indeed cost effective for the insured party to pay a slightly larger premium for a smoother underwriting process or forego a “nice to have” aspect of cover, for a pragmatic insurer who demonstrates efficiencies in underwriting and exercises a commercial approach when dealing with claims.

That said, this does not mean their position is quite as opaque as it might first seem. Underwriters are continuously innovating and engaging with detail in order to try and find a way to provide cover. After all, insurers want to insure risks. Whether it be boxing of warranties, endorsing policies following additional, post-inception diligence being conducted, providing excess cover in respect of underlying operational insurance policies or utilising technology to help derive comfort in respect of certain categories of warranty, insurers are focused on delivering a smooth insurance experience and robust policy.