As we suggested in our October 2020 Update, there is still little comfort to be had form a buyer perspective from the International Liability insurance market. While it is true to say that the Property markets are hardening but still not truly hard, the International Liability market is indeed just that. If the definition of a truly hard market is one where capacity above a certain limit is unavailable at any price, then this really is where our market are as we move further into 2021. To understand why we are now experiencing these unprecedented conditions, we should examine current capacity, loss levels, underwriting results and litigation trends before determining how buyers should respond.

In addition to the hard market, the last 18 months has seen increasing pressure on buyers’ ESG procedures which has in effect added constantly developing and unquantifiable influencing factor on the International Liability market. Announcements by Zurich in July 2019, and subsequently by Lloyd’s in December 2020, have made firm commitments that certain industries will not be supported by insurers, namely coal and oil sands, which has had a profound effect on the capacity available to drive competition. Consequently, these industries are seeing more significant increases.

For the last three years, even theoretical – i.e. the amount that insurers publish themselves – capacity has been gently reducing, from US$3.2 billion in 2018 to US$3.0 billion today. However, in this market that is by no means the end of the story. The theoretical amounts on offer from the market bear little if no relation to the amount of capacity available in practice, as Figure 1 on the previous page demonstrates. While in the Property markets the realistic capacity is at least 50% of the theoretical, in our markets this figure stands at 33%, with even less available for most Energy programmes.

There is of course little doubt that major energy companies often require Liability overall programme limits well in excess of this figure, but we must advise that achieving any higher limits is nigh on impossible in this market, without resorting to alternative risk financing solutions. Furthermore, the withdrawal of some Liability markets has been compounded by the restrictions in average line size that have been deployed per risk by many insurers

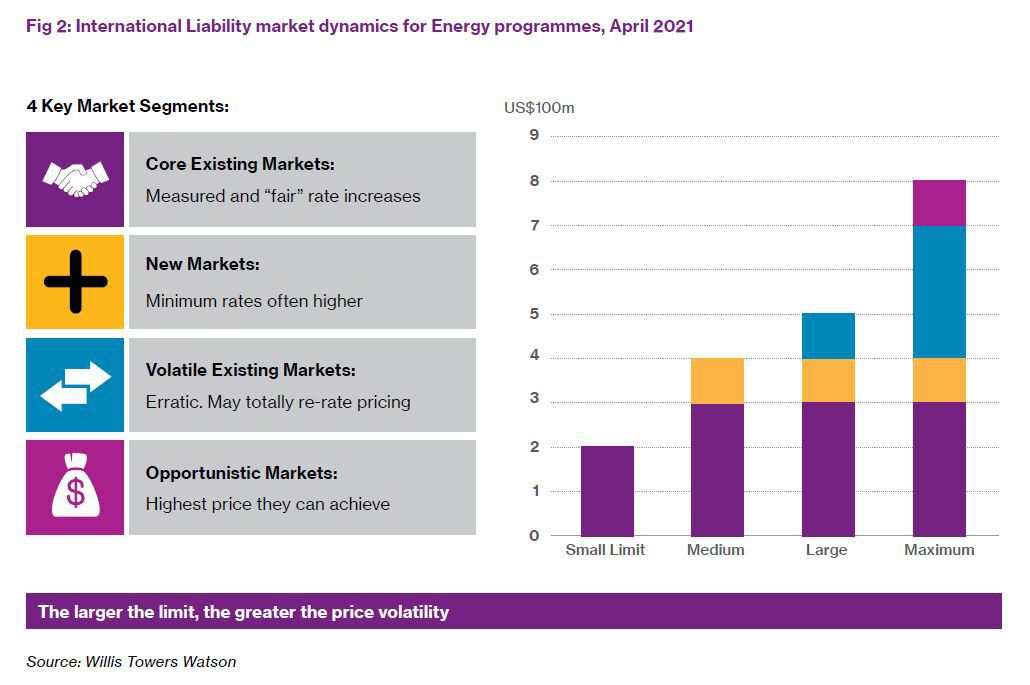

This scarcity of available realistic capacity has enabled some new, volatile and openly opportunistic insurers to target this market to secure increasingly favourable terms from their perspective from buyers that are keen to secure whatever additional cover they can. This dynamic is reflected in Figure 2 above; the core existing markets, with whom buyers share established long-term relationships, can now only offer as little as US$300 million in total – no more than a minimum working limit for most energy company programmes. Added to these long-term players are some recent entrants to the market, offering another US$100 million of capacity. So perhaps a total of US$400 million can be accessed, bearing in mind that the minimum rates required from these markets are often more stringent than the existing insurers’ terms.

However, above this figure buyers are now having to access more challenging markets. First of all, they are now having to approach insurers whom they would have probably been able to avoid during the previous hard market - insurers who are not encumbered by the programme’s previous history and whose pricing can, to put it politely, appear somewhat volatile. Unfortunately, from a buyer perspective, the amount of capacity on offer from these volatile insurers will exponentially increase, depending on the required limit. Finally, we have now the true opportunists – those who are now sensing an opportunity to obtain highly preferential terms from those buyers who have no choice but to accept their terms.

Furthermore, those buyers operating in those energy industry sectors highlighted as part of the increased focus on ESG –such as the Canadian oil sands– are now being affected more than others. Economically viable capacity for buyers whose sole focus is the oil sands sector is now at around US$ 200 million in London, whereas 18 months ago it would have been closer to US$500 million. A number of insurers in Bermuda can help in achieving the limits required, but at higher premiums and more restrictive terms.

Buyers may be wondering why insurers have adopted an increasingly cautious approach to this part of their portfolio. First of all, let’s take a look at recent underwriting results.

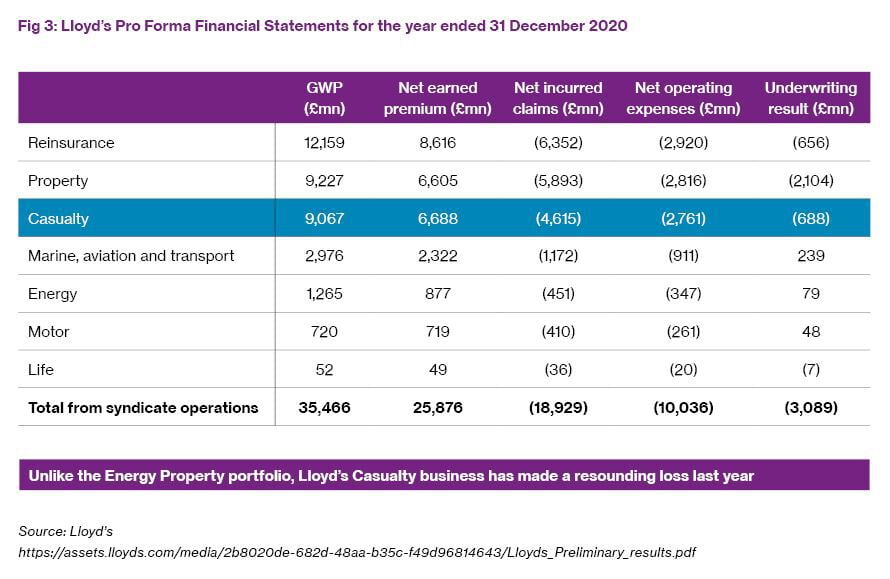

Although Lloyd’s represents only a part of the overall global Liability capacity available, their results do provide a realistic indication of the state of the overall portfolio. Figure 3 above shows that while Energy (Property) has produced a positive overall underwriting result for the first half of 2020, the overall Liability (Casualty) result (across all lines of business) has resulted in a £386 million loss; to put this figure in perspective, the corresponding result for H1 2018 was a £40 million profit1. There can be no doubt that a similar underwriting loss for Liability/Casualty has been experienced in the composite company market.

On top of that, the overall underwriting result from Lloyd’s for the first half of 2020 is also a loss of over £1.5 billion.

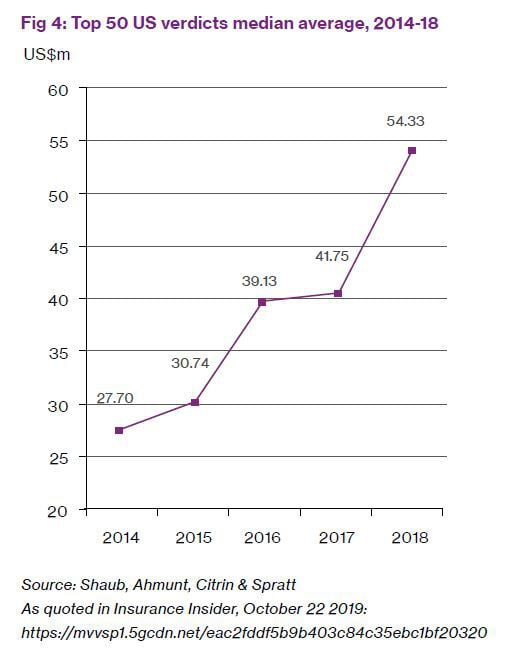

There can be no doubt that one of the key reasons for the losses that have impacted this Portfolio is the advance of social inflation, particularly in the US. We believe that the underlying factors responsible for this are fourfold:

The Natural Resources sector (including Energy) has by no means been immune from the overall deterioration of the global Liability/Casualty portfolio. In particular, we have seen an increase in both frequency and severity of claims in respect of:

Some of the most significant loses have been the aggregate losses following the recent Californian and Australian wildfires, the collapse of certain tailings dams, particularly in Latin America, a gas explosion in the USA, a water utility pipeline rupture in Peru, an oil leak at an offshore platform in Newfoundland and a major oil spill in the Bahamas.

Furthermore, this portfolio will continue to be impacted by the wider implications of overall COVID-19 insured losses. All lines of business will need adjusting to recoup the significant losses expected across multiple lines in the industry, and although International Liability programmes have not yet been directly hit by the obvious losses caused by the pandemic such as Business Interruption, we do expect buyers to receive accusations of COVID-19 infections arising from work environments not fit for purpose.

Faced with such disappointing underwriting results, International Liability insurers are now under strict instructions from senior management to secure as steep a rating increase as possible to offset these recent losses. Indeed, we are now witnessing a wholesale recalibration of existing pricing models, with a focus on rate adequacy and risk profile rather than a percentage change on expiring terms.

Average increases in premium spend for our International Liability portfolio between October 2020 and February 2021 were generally between 25-40%, depending on individual risk profiles and perceived rate adequacy (we have seen well in excess of 50% for some programmes which have not achieved this adequacy) . We have not had any pure Upstream programmes renew during this period as this line of business predominantly renews between April and July but market intelligence suggests that standalone Upstream Liability rates are increasing between 10 and 12.5%, but for those with charterers exposures, where industry losses have been particularly poor, rate increases of 20% or more have been imposed. It is also worth noting that any energy companies buying limits in excess of US$250 million saw reductions in the overall programme limit purchased.

However, this simple overview of rating levels disguises some significant variations in an inconsistent and segmented market. The terms offered usually depend on a number of factors, including:

In general terms, all markets are reviewing coverage terms & conditions, seeking to restrict “exotic”/peripheral coverages such as Cyber, Charterers Liability, Pandemic and Pure Financial Loss.

As well as ensuring rate adequacy, insurers are taking a deep interest in buyers’ ESG credentials, particularly when reviewing oil & gas programmes. Midstream programmes featuring significant pipeline operations are also coming under particular scrutiny. Both Cyber and Drone coverage are generally excluded or written back at a significant additional premium, while Covid-19 exclusion clauses are now universally applied across all policies; indeed, an Insured’s overall pandemic response and its effect on CAPEX, maintenance and turnarounds are all being studied carefully.

No wonder several major clients have chosen to self-insure part of their programme or to reduce the overall programme limit rather than be held as a “hostage to fortune”.

Other buyers, for whom the option to self-insure more of their programme is not possible, have had to face the fact that the limit that they would usually buy is either unavailable at any price or to voluntarily buy less limit if they consider the renewal pricing exorbitant and/or uneconomic. Indeed, we have seen at least 10 major programmes forced to accept a reduced insurance programme limit for one reason or another during the last few months.

Although the market was seeing increases in the first quarter of 2020, it hardened at a much more significant pace from May 2020 onwards. There are therefore a number of buyers who were “ahead of the upward curve in 2020” and whose programmes are going to be on insurers’ radar for more significant premium adjustments. Until these renewals have taken place, we really don’t see any let up in the increases that we have seen over the last few months. Given the current market conditions, we must advise buyers to be as fully prepared as possible to meet the current market challenges full on. Until this portfolio returns to profitability - an unlikely scenario in the short term - buyers should expect more of the same as we move further into 2021. Eventually, like all hard markets, this one will pass as more capital decides to invest in this market, supply and competition increase and in time price rises level off. Until then, we will do all we can to prepare our clients for the challenges ahead. We must continue to emphasise that the market positively differentiates those buyers who are long-standing customers, who offer an outstanding risk profile and who understand the level of data required to secure renewal capacity. Sufficient preparation, planning and realistic expectation management, combined with a flexible approach to retention levels, captive utilisation and limit purchased will ensure the best post possible outcome in a rapidly hardening market environment.

Mike Newsom-Davis is Head of Liability, Natural Resources, Willis Towers Watson GB. mike.newsom-davis@willistowerswatson.com

Little can be said about 2020 that would surprise anyone now; for Excess Liability buyers, the impact of the worldwide pandemic only made the 2020 buying process even more stressful and angst-ridden. We saw a classic hard market, one for textbooks and lore. And as we move further into 2021, we are seeing the effects of the dramatic results of the overall experience, and true to expectations, the meteoric rises in premiums and compression of conditions have slowed in early results.

From the standpoint of the Excess Liability marketplace, we now recognise a two-tiered treatment of buyers by insurers, which will likely continue through the year and which deals with differentiation;

While this can be viewed as the way the Excess Liability marketplace works for the industry, the impact of the hard market from a premium perspective is now moderating when it comes to the first tier.

The hard market in 2020 moved through the year in relentless fashion; buyers saw increasingly difficult repercussions with respect to realistic available capacity. By the middle of the year, underwriters seem to bring on another round of program limit curtailment, further exacerbated by premium income levels, which tend to alter the ability of many insurers to entertain new business or limits for programs with even the strongest buyer-insurer relationships.

Renewal results last year showed increases in the lower half of double-digit territory; however, higher-positioned Excess Liability layers saw increases approaching as much as 100%. For difficult risks, the market was demanding even higher increases, and buyers were faced with the decision of whether or not to spend the money to accommodate insurers’ demands. North American buyers were faced with alternate methods to replace lost or “nonsensical” underwriting capacity, including increased retentions within a program structure, captive insurance use and reducing the total limit purchased. On the latter issue, some buyers could only muster limits of less than half of that provided by their expiring programs. And to rub salt into the wound, insurers seemingly used any opportunity to predict more of the same for 2021.

The driving force, as it has been for the previous two to three years, was the losses hitting the underwriters’ ledgers, both attritionally and spectacularly. We are now accustomed to insurers describing their individual impact of “nuclear” events, not all of which belong to the natural resources realm; however, effecting the same underwriters who also write the energy liability renewals. 2020 had its fair share of catastrophic events and natural catastrophes.

We expect the results of Excess Liability renewals in 2021 to be just as difficult as the 2020 outcomes; however the process is not likely to “confound and astonish” much as it did in 2020. In North America, renewals have shown only a few signs of letting up from the pace of increases seen in the second half of 2020; this is most likely to be prominent within the primary and lead excess placements, where the market has few leaders and none new appearing on the horizon. We believe insurers such as Chubb (Westchester), Liberty (Ironshore), Starr, Allianz and Everest will continue to support Energy Liability, and we reiterate that increases in rating in this area are not anticipated to abate at least through the first half of 2021. Zurich may support certain classes, as will AIG, while Upstream Liability will continue to be supported by Markel, Berkley and Travelers.

What increases are expected? Notably early in the year, certain markets have been up front with brokers and clients on their expectations for 2021, including Aegis, OCIL and AXA XL. Others are looking to be opportunistic - at times predatory -with regard to certain business. Capacity continues to be meted out sparingly, with income levels for insurers up dramatically compared to the tellingly reduced capacity offered. More often than not, line sizes are bound for US$10-15 million; under fewer and fewer scenarios will insurers offer as much as US$25 million.

Furthermore, insurers with the ability to deploy up to US$50 million or more acknowledge the commanding position they enjoy, and this is shown in their pricing. We expect anywhere between 20-35% increases for capacity that can offer up to US$50 million, with this escalation dropping off somewhat for the higher excess placements. As we experienced in 2020, it takes very little for the incremental year-over-year percentages to move beyond what we have stated.

As expected, the Liability prices and rates in play through 2020 and expected in 2021 have brought in new investments. However, this capacity is expected to play within the current commercial levels and will not be enough to start driving premiums down. We expect extra capacity for certain classes of business to emerge from Bermuda-based Arcadian, Ark and Vantage Risk among others, with Aspen’s Bermuda operations possibly expanding its remit to include the Energy portfolio. New Lloyd’s syndicate Inigo, together with the expanding ERS and Sirius, have committed Excess Liability expertise to certain classes of natural resources business. However, capacity for contractor business has all but withdrawn from the Energy Liability sector in London.

The “minimum” price per million benchmark has moved from circa US$4,000 to approaching US$6-7,000, and this may move even higher. The percentage increase that originates in the renewal of higher excess layers then finds its way through into lower layers, where the impact of the increases is magnified for these programs.

Policy conditions continue to be reviewed at each renewal; we expect, given the renewal of reinsurances at the end of 2020/start of 2021, that broader communicable disease/pandemic exclusions will be increasingly required, particularly so for capacity from London/Europe and Bermuda. London capacity will also deal with cyber exposure, looking to tighten any writeback previously afforded. We continue to see a sustained review of policies’ pollution exclusions, scrutinizing time element parameters, named perils and treatment of waste operations as well as their understanding of the specific exposure to wildfire.

It is also noted that insurers are coming under public pressure from shareholders and stakeholders to address their overall portfolio of business when it comes to supporting buyers in certain energy industry segments. Continued emphasis will be placed on buyers’ ESG commitments and on their operational sustainability progress and goals.

As we move further into in 2021, the renewal process will again be stressful for buyers, underwriters and brokers. Most buyers will likely be running through their second virtual renewals, and another year of visits and facility/asset tours. Buyers should plan on off-cycle discussions with core insurers, determining the impact of shrinking capacity and moving attachment points, retentions, stress points on coverage and conditions and cost expectations. The role of analytics as a tool to assist in the renewal process is now prominent and is being used to assess various options for setting excess points, layer costs and structuring, limits and advanced benchmarking.

With very few exceptions, multi-year contracts, or ones longer than annual terms, are not being offered, at least not without the opportunity to re-rate and assess at anniversary date.

Renewal information should include payroll, general liability information, well counts and footages, drilling details, cyber exposure (protection and practices), refinery throughput and turnaround schedules. It should also specify third party surroundings around any facility, pipeline and gathering system information, including integrity details, regulatory reports, rail exposure, specific auto fleet details (including use of autonomous vehicles) and capital expenditures. Regarding capital expenditures, buyers should expect questions on where the impact of any cuts being made will be felt.

The Marine Liability market will continue hardening during the remainder of 2021, following several new large market losses and the significant deterioration of existing claims. General pricing increases in the region of 10–15% are to be expected for renewal business, even for programs with clean loss records; however, higher increases are required on programs which have adverse loss records or that are considered to be under-priced at current rating levels. Pricing allowances are only being considered on programs with significant material reductions in exposure levels, when pricing levels are already considered to be adequate. Buyers should expect increased risk scrutiny (including a strong focus on risk management), pressure on capacity and longer lead times during the renewal process.

The London Marine market hardened considerably over the past two years, caused by continuing deterioration in profitability levels over the past 5–10 years. Despite corrective action taken over the past 24 months, many insurers are still showing loss positions. This is partly due to the poor performance of the P&I and Charterers Liability Reinsurance portfolio, which has suffered significant losses and continued back-year deterioration.

Remarketing options remain limited on programs where more complex exposures are covered and/or where higher limits are purchased. Programs with high limits are also facing increased scrutiny in terms of their structure, with re-layering required on placements with long “stretches”, as well needing to demonstrate pricing adequacy and technical rating in order to secure full market support. In the Ports and Terminals sector, Property risk underwriting is being scrutinised more closely. The pricing of Property and Handling Equipment cover in catastrophe risk areas has come under particular pressure, with higher than average increases being applied. Bulk liquid terminals have produced several large market losses during 2019 and 2020 which have resulted in a contraction in underwriting appetite, together with more rigorous reviews of underwriting information, for this type of operation.

David Clarke is an Executive Vice President for Willis Towers Watson’s Liability practice based in New York. David.Clarke@WillisTowersWatson.com

Unlike several other related classes, the Environmental market has remained relatively stable over the past year with just a small uptick in renewal rates, averaging between 5–10%. Dependent on attachment point and exposure, some buyers are even enjoying renewals at the same rates as last year.

The gradual pollution cover that our market offers is increasingly in demand to provide balance sheet protection; these transactional programmes surrounding mergers and acquisitions or disposals are extremely effective deal facilitators, unblocking impasses in sales negotiations where the seller wants a clean exit from an environmentally distressed business but the buyer is reluctant to take on responsibility for unknown historic risks that are difficult to quantify financially. Venture capitalists, banks and lawyers increasingly see the deals available in the Environmental Liability market as a valuable tool to ensure a deal moves ahead by transferring these risks to an insurer for a one-off premium payment for a policy of 7-10 years’ duration.

Environmental coverage and capacity continue to evolve as a result of the market’s heightened awareness of increased exposures, legal liability and regulatory risk. The risk of biodiversity damage and complementary or compensatory remediation costs attached to rectifying this is increasingly a big-ticket item that the market can provide protection against.

The market’s appetite for Energy risks remain fairly broad, even to the extent of still being able to provide cover for TMFs (Tailings Management Facilities). Particularly for Energy environmental risks, London remains the main centre for underwriting outside the USA, with developing markets emerging in Australia and the EU supporting rest of world placements.

Generally, Environmental programmes dovetail around the Energy Liability programme to provide seamless pollution protection for pollution from any cause, whether that be sudden & accidental or gradual. As the Energy Liability market hardens and contracts, we also continue to use the Environmental Liability market to provide additional sudden & accidental cover at the top end of Energy Liability programmes, or occasionally to infill gaps mid-programme. The Environmental market can write onshore and offshore risks quite comfortably and USD200 – 300 million + limits are readily available in this sector.

The niche products mentioned in last year’s review continue to be in demand:

Joanna Newson is Director, Environmental Practice, Willis Towers Watson London. Jo.Newson@WillisTowersWatson.com

1 https://www.lloyds.com/investor-relations/financial-performance/financial-results/interim-report-2018