Have risk managers caught up?

Private Equity (PE) executives are looking differently at oil and gas assets. Have their risk managers caught up?

If there is one industry that can benefit from the ever-increasing mergers and acquisitions (M&A) activity, it is surely oil and gas (O&G). Though demand for hydrocarbons continues to grow, the increasing competitiveness of renewables, along with rising global awareness of climate change, is putting the longevity of O&G companies’ traditional business models under question. On the supply side, mature basins like the North Sea offer efficiency opportunities to nimbler players, unencumbered by the rigid one-size-fits all operating models deployed by larger firms, which were designed for a very different era of hydrocarbon production. For their part, larger majors and supermajors are happy to relinquish ownership of these assets, having achieved the returns promised on investment capital years, if not decades, ago.

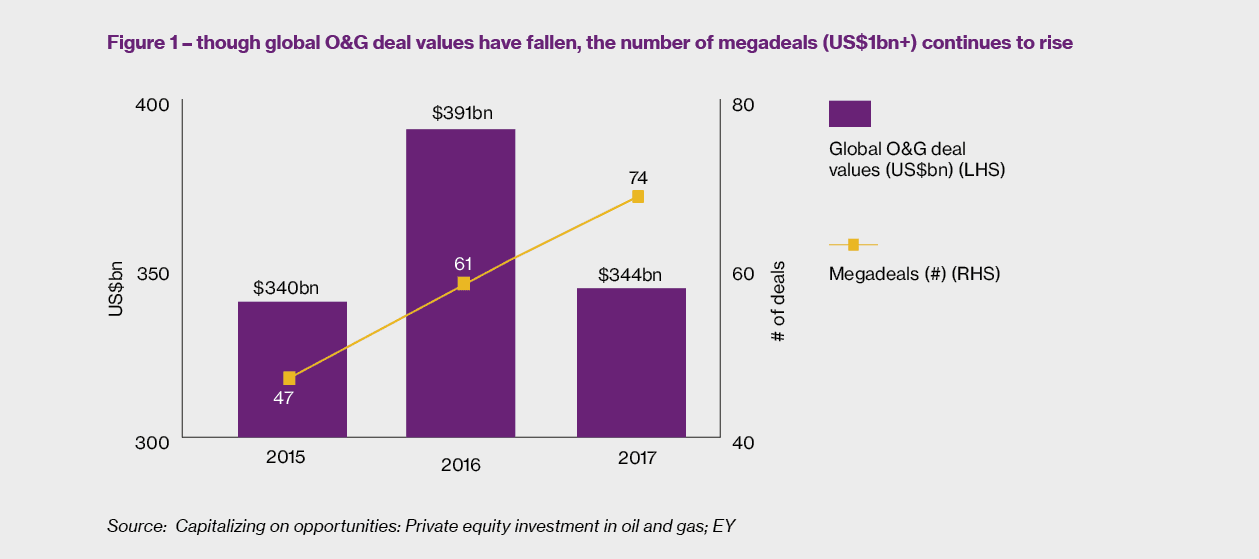

It is no wonder, then, that deal activity in O&G globally continues to remain healthy. Although global deals are down in 2017 from the prior year when measured by both volume and value, a flight to quality is beginning to emerge. The number of megadeals has continued to increase every year since 2014. 47 assets valued at greater than US$1bn changed hands in 2015. By 2017, this had increased to 74 assets1.

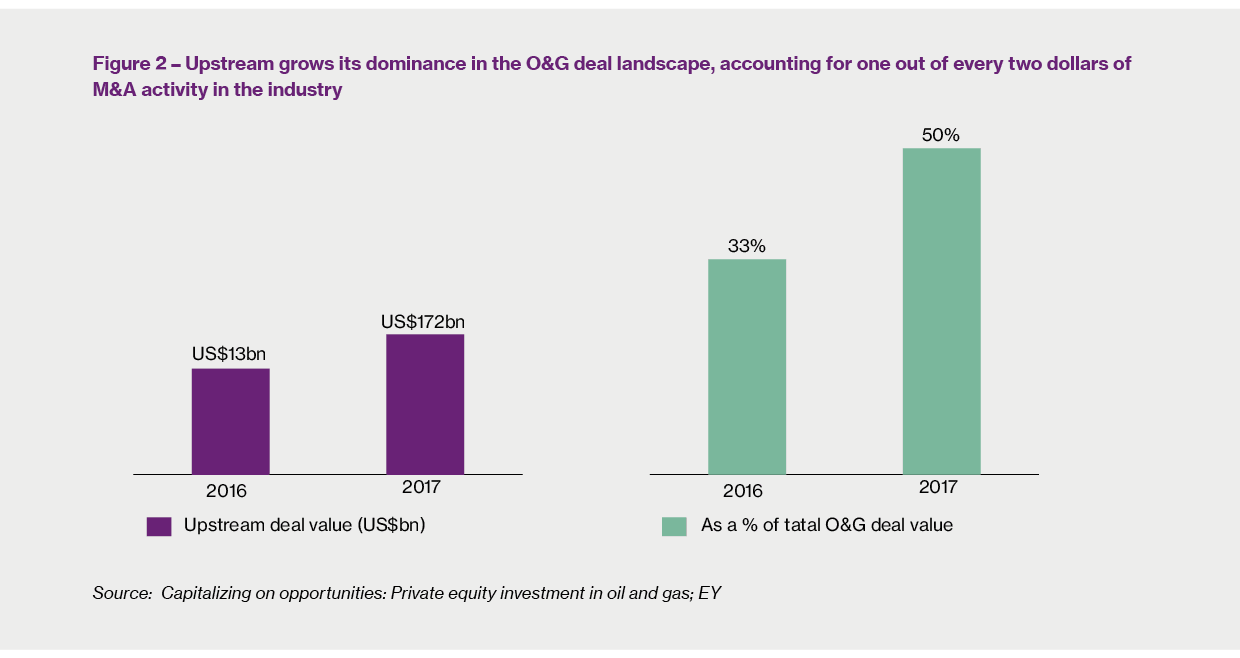

The Upstream sector has benefitted the most from this trend. Deal values climbed 30% over the previous year to US$172bn in 2017, representing 50% of global O&G deal activity, up from 33% in 2016.

Who’s investing? The investors driving this trend can broadly be divided into three camps:

It is this third category that PE investment in O&G falls into. Scarcely does a week go by without news of PE interest in O&G assets, mostly around the shale developments concentrated in the Permian basin of the United States, or the late-life fields in the North Sea. Deals such as Siccar Point’s acquisition of OMV’s North Sea assets2, or Diamondback Energy’s US$9.2bn purchase of US shale competitor Energen3, are becoming ever more common. But the PE industry has been here before; between 2007 and 2015, PE averaged 70 O&G deals a year4. In that era, the industry saw two levers of value creation. Initially, the returns to be made as a provider of capital to finance exploration-led growth, and latterly as oil prices nosedived and valuations reached eye-wateringly low levels, the enterprise value gains from an eventual price rebound.

The example of NGP Some investment strategies have reflected this thinking, such as that of Natural Gas Partners (NGP), an Irving, Texas-based O&G investment firm, with 360+ transactions to its name5. NGP has equity commitments of close to US$16bn across its first eleven funds (with Fund XI closing at US$5.3bn in 20156), and is reported to have raised over US$4bn of its US$5.3bn target for its twelfth fund7. Many other investments over this period, however, have not been as successful. EnerVest, a Houston-based O&G investor, saw its US$2bn O&G-focused funds collapse in 2017 when it was unable to fully meet obligations for the debt underpinning the funds’ investments8.

With a mixed record of big discoveries backed by PE capital, and a set of underlying fundamentals which are likely to mean that oil prices do not reach the heights they scaled between 2011 and 2013, what is the PE industry doing differently to unlock value from the current investment wave?

The answer lies in operating efficiencies. The low price era has forced firms to brutally optimise their cost base, but PE firms believe that there’s more to be done. Views from the industry bear this out.

A global survey of upstream operators, released by Wood Mackenzie in October 2016, a year in which oil prices to date had averaged below US$43/barrel, reported that cost reductions of 16% - 24% were achieved by the industry in 2015-16 and a further 3% - 7% in 2016-17 were expected. But the same survey revealed that most operators thought that only 7% - 14% of these savings were structural and sustainable in the long run9. PE firms reckon they can bring their formidable talent for looking afresh at operating models to seek fundamental value transformation to bear on their newly acquired O&G investments.

The risks involved But managing oil and gas operations is an unusually risky undertaking. If we look beyond the obvious risks to health and safety from volatile hydrocarbons, we will find that a number of other, equally critical risks with similarly far-reaching consequences are lurking, such as:

Product contamination, or deviation from tight specifications in the case of LNG, could set off a chain reaction of outages further downstream leading to damages and even litigation.

And all of this is before we consider the risks associated with the fundamental transformation of operating models that PE firms will need to enact in order to build sustainable operational value.

Operating risk management: still a work in progress for PE companies Managing operating risk is, with some notable exceptions, still an area of development for PE firms. The industry does a superb job at identifying, assessing, quantifying and mitigating financial risks. Working closely with the management of the companies that they acquire, PE executives also usually stay closely connected to the way key business risks are being managed, such as competitive threats, demographic changes in key markets, evolving perception of the brand and reputation, changing consumer behaviour and so on.

But the risk implications of an O&G asset’s maintenance strategy, shutdown plan, supplier & contracting strategy, workforce plan and other aspects of managing operating risk are usually left up to management. And while management may have the best of intentions, this approach typically results in the status quo of risk being managed for a gradually depleting natural resource with a reasonably predictable production profile, rather than a cash-generating asset in need of fundamental change to maximise its worth within its defined lifetime.

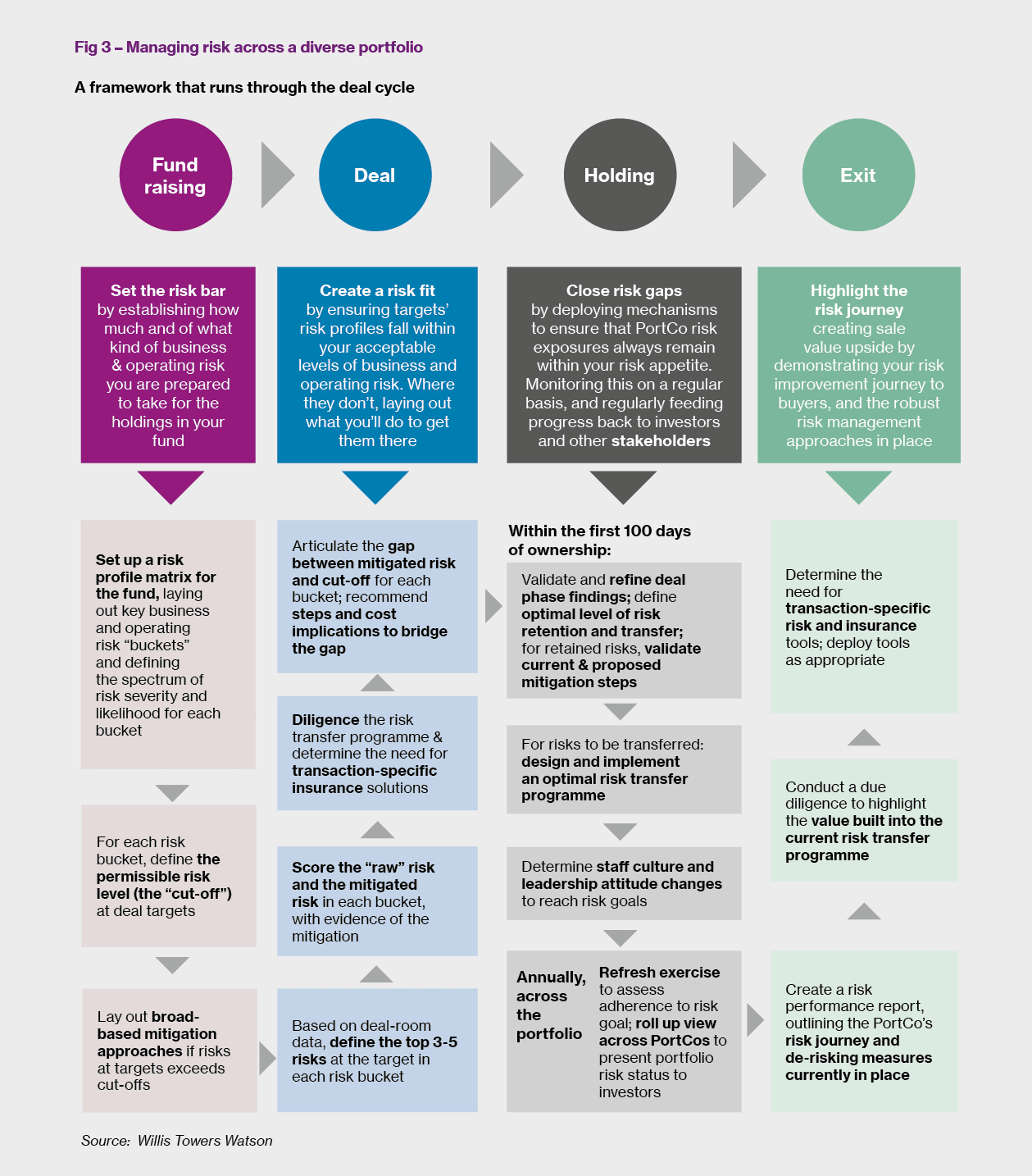

Taking a leaf out of the financial risk management process What should the PE industry do to look at operating risk differently? To find the answer, the industry doesn’t need to look very far beyond the way it manages financial risk. Risks to achieving Internal Rate of Return (IRR) targets, risks of breaching debt covenants, risks of being able to meet interest coverage ratios – these are identified and planned for, measured using a consistent set of indicators, revisited with regularity, and reviewed holistically across the portfolio. Material movement on these risk measures are reported to investors, successes in meeting milestones are publicised, and failures investigated. In short, financial risks are managed across the deal cycle, from fundraising to exit. A similar fundraising-to-exit approach to operating risk would encompass four characteristics, as outlined in Figure 3 on the following page:

Fundraising stage Start with setting the risk bar at fundraising. PE firms have a lot to say to investors about what makes them stand out when raising capital. Having a perspective on how they’ll manage critical risks in operations, especially when it comes to deploying that capital into asset-heavy O&G investments, can add to the arsenal of differentiators. But a point of view itself is insufficient, and must be backed up by a tangible and measurable methodology.

PE firms must start with defining their operating risk appetite - setting up a risk profile matrix for the fund, laying out key operating risk “buckets” and defining the spectrum of risk severity and likelihood for each bucket. For each risk bucket, they would then define the permissible risk level (the “cut-off”) at deal targets on a numerical scale. And finally, they would lay out broad-based mitigation approaches if operating risks at target investments exceeded cut-offs.

What would a generic risk profile matrix for an O&G focused fund look like? Some of the key risk buckets would likely be geopolitical, cyber, environmental and terrorism. Depending on the fund’s geographic focus, the appetite for geopolitical risk might be medium to high (say 5, on a 10-point scale).

If the asset is large and/or onshore, and/or its output forms a material proportion of the inputs into a single country’s power mix, the appetite for cyber risk would be quite low (say 3 on 10). This quantified appetite represents the “raw” risk that a firm would be willing to take on, on behalf of its investors, in its O&G assets, before any controls or risk transfer strategies are put into place.

Deal stage Creating an operating risk fit at the deal stage comes next. Each O&G investment target will have its unique set of risk characteristics, depending on its location, size, design makeup, customer base and other features. With deal-room access comes the ability to scour a target’s operating data in detail, establishing a picture of the top 3 - 5 operating risks within each risk “bucket” of the risk profile matrix. Through deal-room data, PE firms are also able to understand and quantify, at some depth, the extent of mitigation measures in place for these identified risks. And finally, where a gap exists between the score on the fund’s risk appetite for the bucket, and the actual score on the target, plans can be drawn up to close the gap as a part of the first 100 day plan post-acquisition.

What, again, might this look like in practice? Say our fictitious O&G fund with a geopolitical risk appetite of 6/10 has identified 3 key geopolitical risks at an investment target – the risk of outright confiscation of the asset by the jurisdiction’s ruling regime quantified at a 3, the risk of the ruling regime passing onerous taxation legislation specifically targeted at the asset at a risk of 8, and the risk of a physical attack on the asset in the next five years, quantified at a 7. The overall simple average geopolitical risk for the investment, at 6, is higher than the appetite of 5. The fund would put together a plan for the latter 2 of the 3 risks outside of the cut-off, laying out what it would to do bring them back within the cut-off, should the deal be successful. To protect against adverse legislation, the PE firm could transfer the risks to the insurance markets through a specialised tax risk policy. To protect against a terrorist attack, the PE firm could commission a review of the physical features, layout and security arrangement of the sites, combined with specific insurance arrangements to indemnity for the cost of an incident.

Holding stage With transactions having completed, closing the operating risk gaps are needed in the holding stage. This broadly divides into four steps:

Exit stage By this time, a PE firm that embarks on this journey would have demonstrated:

But it doesn’t end there. The exit stage of the deal cycle is all about highlighting the operating risk journey the firm has been on, to create sale value upside. The asset the PE firm is exiting demonstrates arguably far better operating risk management than the one they took over. This must be made apparent in the vendor diligence underpinning the sale process, along with a quantifiable demonstration of the journey that the PE firm has been on to achieve its risk management successes.

Conclusion: standing out from the crowd PE’s interest in O&G is far from over. According to Wood Mackenzie, a further US$13bn of PE capital could find its way into the North Sea, adding to the US$12bn already invested over the past two years10. As the drive to unlock ever more value from these assets intensifies, concerns around the impact on operating risk profiles will remain at the fore. PE firms that are able to demonstrate to investors how they’re protecting value downside through superior operating risk management will stand out from the crowd.

Arif Kamruddin is Director of Strategy and Business Development for Willis Towers Watson’s Global Solutions Group in London.

1 https://www.ey.com/Publication/vwLUAssets/EY-global-oil-and-gas-transactions-review-2016/$FILE/EY-global-oil-and-gas-transactions-review-2016.pdf 2 http://www.siccarpointenergy.co.uk/uploads/20161109_OMV_Press_Release_Final.pdf 3 https://www.naturalgasintel.com/articles/115433-permian-players-diamondback-energen-agree-to-92b-merger 4 Capitalizing on opportunities: Private equity investment in oil and gas; EY 5 & 6 https://ngpenergycapital.com/about-ngp/ 7 https://www.altassets.net/private-equity-news/by-pe-sector/buyout/ngp-said-to-pass-4bn-mark-for-latest-oil-and-gas-fund.html 8 https://www.cnbc.com/2017/07/17/energy-fund-losses-oil-and-gas-investment.html 9 https://www.woodmac.com/news/editorial/upstream-cost-problem/ 10 Private equity leads the changing of the North Sea guard; Financial Times; 13-Feb-19