Undercurrents of change

Introduction – what lurks beneath? Anyone who has learned to surf or is familiar with beach safety may remember an important lesson: the most dangerous rip currents lie beneath the flat water.

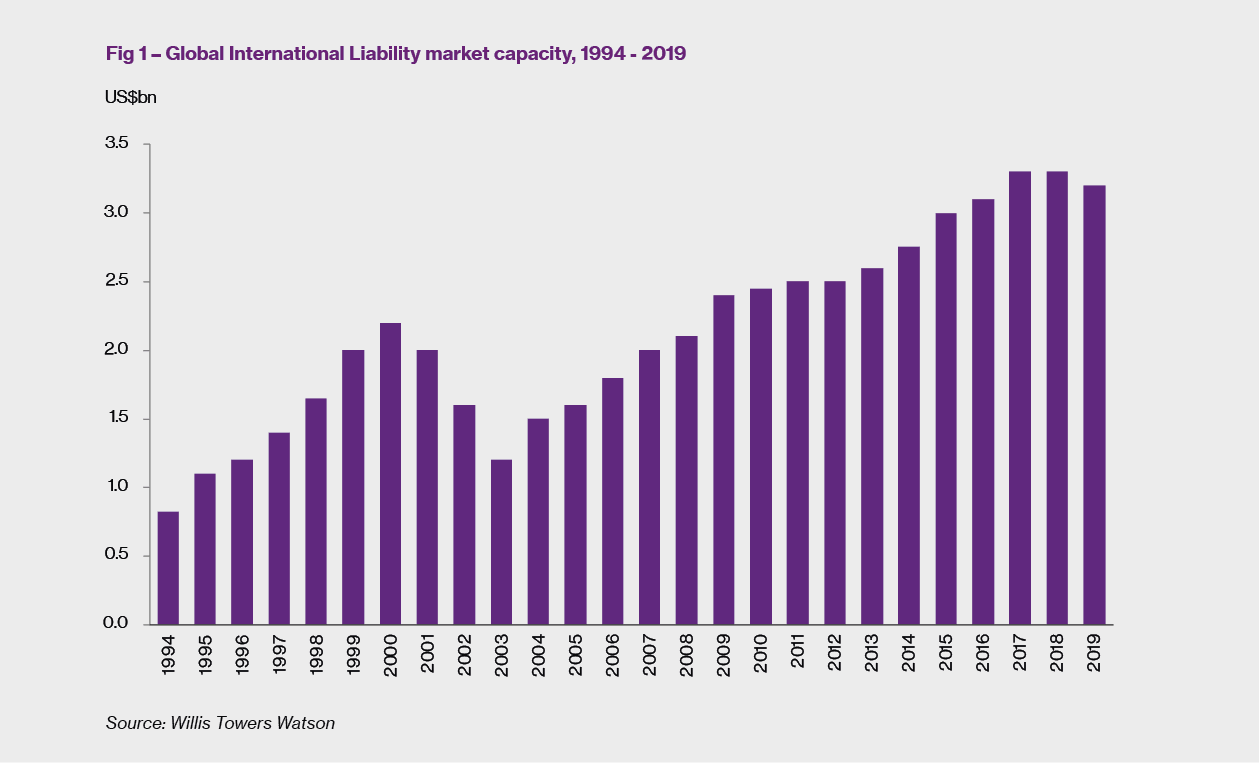

This is a particularly fitting analogy for the current state of the Liability market: superficially all is calm (as per Figure 1) - global Liability market capacity remains virtually unchanged at US$3.2 bn and there were no dramatic changes to treaty reinsurance costs at Q1 2019.

Five undercurrents to beware of in 2019 The reality is somewhat different. Beneath this relatively calm exterior, there are five undercurrents driving a strong change to underwriter sentiment:

A sea change in market conditions? The net result of all these elements is a tangible hardening of conditions in the Lloyd’s and London company market. Single digit percentage increases are the norm for renewals; for risks that are considered to be sub-standard, have poor loss ratios or are in a particularly risk exposed activity class (such as midstream/pipelines, electricity transmission in arid regions and tailings dams of a certain construction type) the renewal increases can be significantly larger. The positive news is that much greater focus is now placed on risk quality, consistency and strength of client relationship. Buyers that can differentiate themselves by providing quality information, demonstrating good risk management practice and leveraging their long term relationships are able to obtain more preferential renewal terms that their peers.

Oceans apart It must be recognised that the rate of change varies in the differing regional Liability markets. In the Continental European market, conditions remain relatively benign whereas in Australia and Canada there are definite signs of similar hardening pressures as exhibited by the UK based markets. Whilst domestic buyers who purchase modest limits based outside these regions may be relatively unaffected by the above conditions, any major energy or natural resources industry client requiring substantial limits will need to be aware of these drivers and the changing market conditions. Navigating the tide At every Q4 renewal season over the past few years there has been speculation about a potential hardening market, fuelled by natural catastrophe results, treaty costs etc. This is the first year that we have seen some tangible change in certain geographic sectors of the global Liability market.

This is not a cause for panic; more a cause for preparation. Many brokers (and indeed underwriters) may have never experienced a changing market. The right broker selection can pay dividends now more than at any other time in terms of having a strategy, knowing the right markets in the right regions, the ability to leverage their long standing relationships and profile the client in the best way. From the provision of Authorisation for Expenditure values, methods of tailings dam construction, contractual exposures and the ability to articulate exposure changes, other than by just revenue, a technical approach to the renewal process has never been more important, as insurers seek greater understanding and justification for their underwriting decisions.

Summary – preparation is key! In summary, for anyone about to venture out into renewal waters: prepare well, pick your timing, have a plan and know your exit strategy. More than ever, a seasoned broker will be an invaluable guide to see you through the turbulence and bring you safely back to shore - without undue cost to life, limb or renewal budget.

Mike Newsom-Davis is Head of Liability, Natural Resources at Willis Towers Watson in London.

1 https://www.lloyds.com/market-resources/market-communications/market-bulletins/market-bulletins (Y5232)

2019 – the market begins to turn The market for Energy Liability in North America, which had generally tried to find a way to correct years of premium softening and middling results in 2018, looks to be finding its way to do so in 2019. 2018’s catastrophe losses to the market were not as pronounced as in previous years, but single events focused insurers on the ability for the class to sour insurers’ expected results. Insured exposures to the risks in the energy and natural resources industries continue to dominate Liability renewal discussions and outcomes. The market pushed very hard for renewal increases at the end of 2018 and at the start of the new year. Flat to single digit percentage increases were seen for clients with clean records and static exposure change, driven by:

Even buyers with reduced or reducing exposures could find the process not as might be expected, and insurer’s clients with losses will see harder renewals. Other than rate and premium increases, one may feel as if this is a repeat of the renewal process for a number of years; and there is not much evidence to refute this. Non-capacity risks will fare better than those requiring larger limits. Capacity - is $25m the new $50m? Realistic Excess Liability capacity has shrunk as we have moved further into 2019; we believe this equates to about 10% less than that available in 2018. This arises out of certain insures:

This has been seen especially where total capacity is reduced from participants in merged or acquired transactions. We note that these actions apply to Liability markets considering North American Energy in Europe, Lloyd’s and Bermuda, as well as to domestic North American markets. Developments in Lloyd’s affecting the North American market We have mentioned elsewhere in this Liability chapter the action Lloyd’s has taken in the overall and granular performance review of its syndicates2. The attention given by Lloyd’s to the poor underwriting results from certain segments has been embraced by a broader range of insurers, reaching as far as North America. In particular, we observe that some have curtailed or stopped underwriting Canadian Upstream and Midstream Energy Liability business (predominantly in western Canada), yet we also hear of other insurers believing that the hardening market conditions there presents an opportunity.

Loss experience While the North American loss experience within the Liability market was not marked by numerous high impact events in 2018, the number of initially smaller losses seems to be increasing in quantity and size, hastening the erosion of underwriting results. However, large catastrophic losses in 2018 have impacted initially a broad number of Liability underwriters, magnifying the perceived inadequacy of rating and pricing, particularly in this class. Underwriters continue to monitor Energy exposures relating to pipelines, rail, increased onshore drilling and the concomitant commercial automobile usage. The risks of most concern appear to be those arising from the trimming of sustaining capital expenditures as well as delayed maintenance and turnarounds and of course the risk of loss from cyber failure/attack. Buyers have to present what each is doing with respect to environmental governance, clearly outlining their approach to sustainability. Liability insurers will now inevitably focus on the buyer’s discipline in this area.

Legal developments arising from Joint Venture losses In 2019, the market will have to deal with the recent Texas Supreme Court decision regarding the treatment of defence costs incurred in connection with a loss sustained arising from a Joint Venture3. Pertaining to the April 20, 2010 Deepwater Horizon disaster, the Court maintained that while the Excess Liability wordings available to one of the joint venture partners involved with the operations of the Macondo field did scale the limit/amount of liability payments payable from insurers, the same expected scaling did not apply to certain defence expenses incurred by that partner (see Anadarko Petroleum Corporation v Houston Casualty Company, et al.). The case is understandably complex, but even now insurer expectations are that the wording is meant to scale the applicable limit for all indemnity and defence. Insurers are loathe to admit their wording could be taken any way other than scaling all recoveries; this decision will likely precipitate a review, with the outcome a change to the London market wording or a completely new Liability form/policy for energy risks. The reaction may also involve changes within wordings pertaining to other lines of coverage.

Increased M&A activity While 2018 closed with incumbent insurers no longer willing to offer discounts unless there was a clear reduction in exposure, the threatened market reaction to a background of historic low rates, combined with an acknowledgement of the scale of losses from the 2017 hurricane season and certain shipyard accounts, was seen in some, but by no means all, lines of business. This continuing pressure on profit margins led to an increase in M&A activity during 2018, with AIG, Axa, Hartford, Axis and China Re all making headline acquisitions. Withdrawals prompted by Lloyd’s PMD Lloyd’s PMD ensured that the 2019 business plans of all syndicates were strenuously analysed. In order to be given permission to trade in 2019, many managing agents chose to either exit from or shrink certain Marine lines, including the Standard Syndicate, AmTrust, Barbican and Advent.

More turmoil ahead – but are rating increases justified? As we move into 2019, while the market would like to give the appearance of being leaner and fitter, RSA’s announcement that they are placing their Logistics and Port & Terminal portfolio into run-off4 indicates that there is some potential turmoil ahead. But even with a background of continuing low investment returns, increasing exposures and loss costs (such as those related to removal of wrecks), we believe that rate increases for well-performing Liability placements are still hard to justify. Despite this, we believe that most of the Marine portfolio will see some level of increase in 2019.

Renewals for Port/Terminal Property and associated exposures will, more than ever, be influenced by location, record and quality of risk management - all things being equal:

David Clarke is an Executive Vice President for Willis Towers Watson’s Liability practice based in New York.

2 https://www.lloyds.com/market-resources/market-communications/market-bulletins/market-bulletins (Y5232) 3 Anadarko Petroleum Corporation v Houston Casualty Company, et al. 4 https://www.rsabroker.com/system/files/Ports%20%26%20Terminals%20Solutions%20Fact%20sheet.pdf

The global EIL market in 2019 remains a niche sector across the world. London is the main centre for underwriting of such risks outside of the USA, while additionally there are well developed markets in Australia and the EU. Capacity continues to be readily available within the EIL sector, with 16 insurers now offering EIL products alongside conventional lines (Casualty/Property/Marine/ Financial Lines). £250m of capacity is readily available in the London market. Recent Brazil tragedy highlights potential environmental risk for energy companies Environmental incidents are continuing to occur around the world; many remain uninsured if they are caused by gradual pollution or are as a result of legacy issues. The human tragedy following the recent dam failure in Brazil overshadows the clean-up obligations that will follow this disaster. It also highlights an urgent need for business around the globe to consider how legacy liabilities can affect future business performance. Per- and Polyfluoroalkyl Substances (PFAS) are becoming a pollutant of concern and we are expecting to see this excluded from future placements as the negative effects of this compound are investigated further. Market news Recent developments in the EIL market in London can be summarised as follows:

Evolving legislation around the world EIL is still the niche sector it has been for the past 30 years but we are seeing legislation evolve at an increasing rate in recent years:

James Alexander is Environmental Practice Leader for Willis Towers Watson responsible for developing the practice in London.