A traumatised and challenging market

A traumatised and challenging market In our “Winds of Change” market update that we published in October 20181 we showed how the Downstream market was reacting to a range of different factors that were producing real and significant change in this market. It’s worth repeating these factors again as we move further into 2019 as they are not only all still in play but if anything have become even more pronounced following the January 1 renewal season.

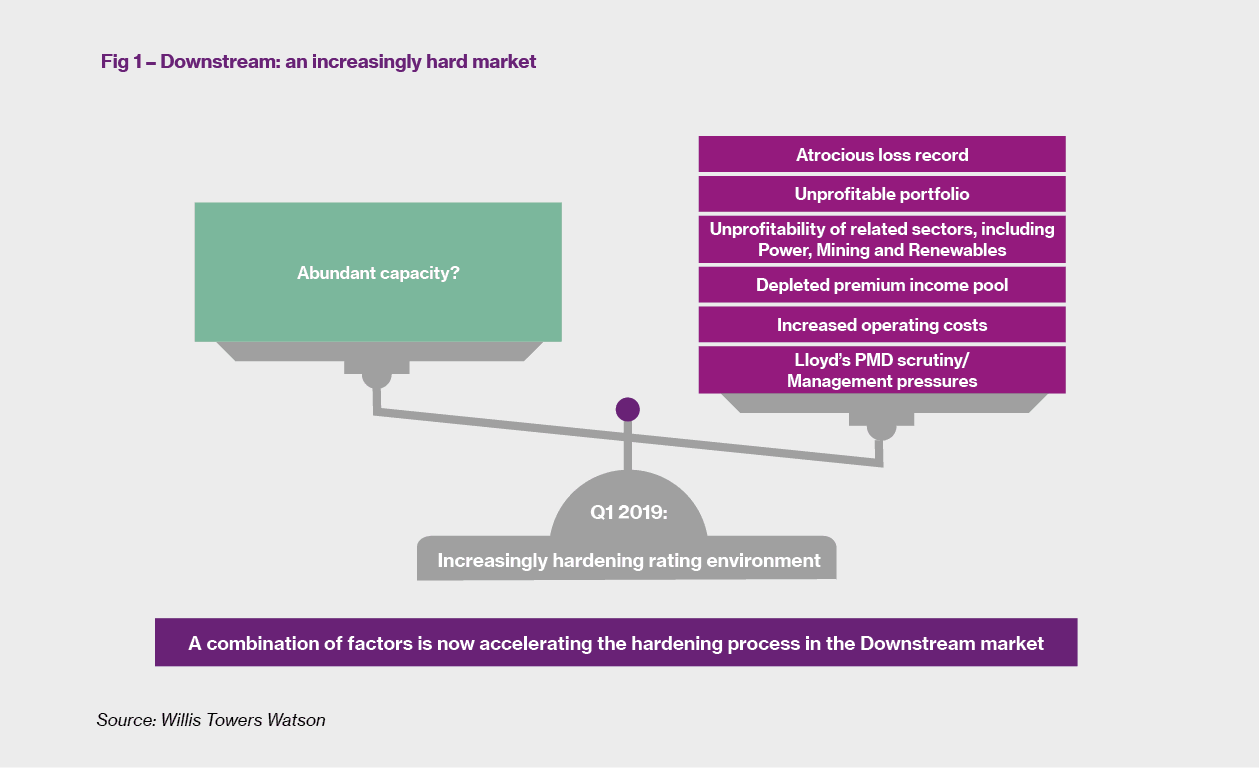

As demonstrated in Figure 1, we have seen an increasingly hard market developing. The abundant market capacity that has oversaturated this market with excess supply for many years now has been offset by a “perfect storm” of other factors – an atrocious loss record, a depleted premium income pool and increased operating costs, not to mention negative underwriting results from other parts of the Heavy Industry Property portfolio, coupled with the rigorous attentions of the Lloyd’s PMD and indeed their own management.

So why has the situation for buyers deteriorated still further since October 2018? How are programmes being impacted? And, perhaps more importantly, how can buyers offset the worst effects of the hardening process in this market to negotiate optimum terms and conditions?

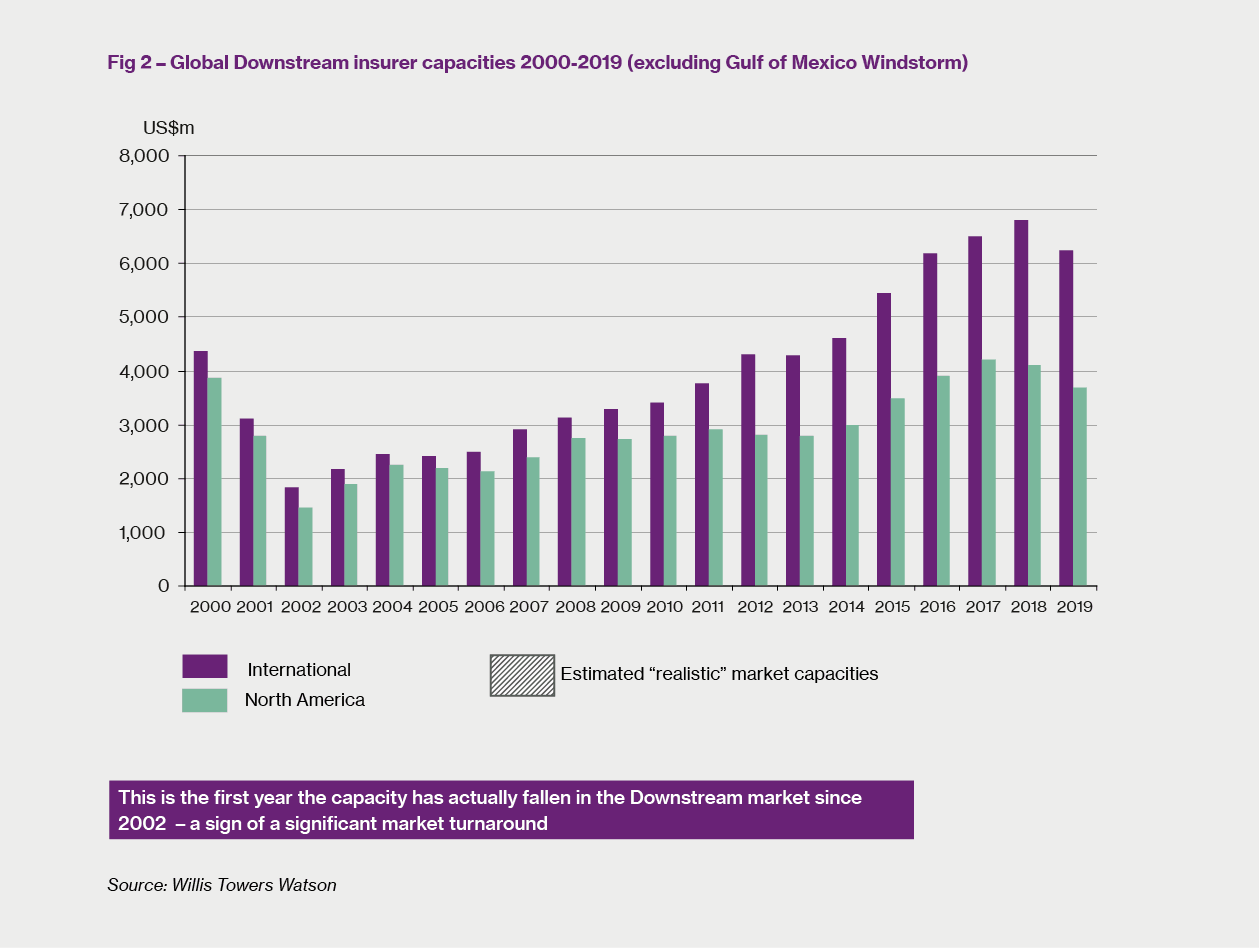

A glance at our Downstream capacity chart for 2019 (Figure 2) shows why conditions have become so challenging in this market. For the first time since 2002, in the immediate aftermath of the 9/11 tragedy, overall theoretical underwriting capacity (as provided to us by the market) is actually down – to just over US$6 billion for International business and just under US$4 billion for US business.

Major insurers pull in their horns The reason for this contraction lies not so much in any major market withdrawals, but more in the fact that some major insurers have decided to abandon the strategy of offering (at least in theory) significant capacity way in excess of what their competitors can offer and instead are refocusing to offer a more realistic amount. In any event, we found that during the period when they were offering this inflated capacity the number of times it was actually deployed were very few indeed. These insurers are still able to offer a significant line; however, because their focus is now on underwriting profitability rather than premium income generation there is no need for them to advertise a higher capacity level to generate increased sales. So while in the past a certain major insurer might have offered, for example, a 25% line on some less-favoured programme simply to secure the associated premium income, without this business driver this line is likely to be scaled back to say 15% in 2019.

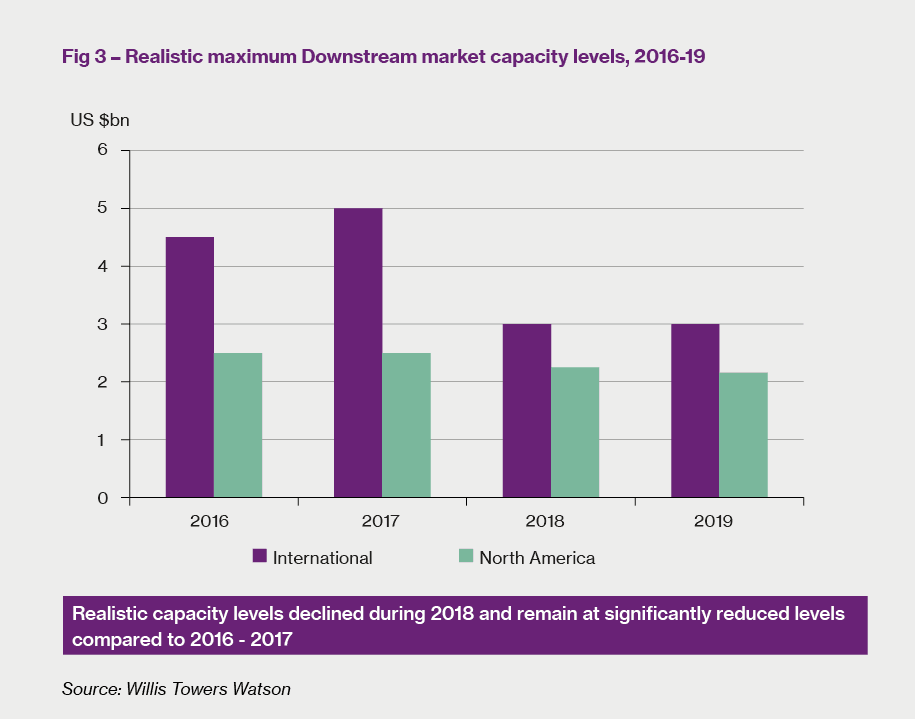

Realistic capacity without regional markets remains at US$3 billion As a result of this market contraction, we believe that in general terms the maximum realistic market capacity for any one programme has remained at US$3 billion for International business and US$2 billion for US business, as stated in our October 2018 update (see Figure 3). However, one statistic does not cover the full range of potential outcomes in this market; available capacity does indeed depend on how much local market interest can be generated for a given programme.

Regional markets boost available capacity So while buyers based in regions such as the Middle East and the Asia Pacific region can take advantage of being able to access additional local market capacity, the same cannot be said for regions such as Western Europe where no such domestic market exists. For example, we are aware of several Australian LNG buyers that purchase capacity in excess of US$4 billion which they access by approaching regional insurers based in Singapore; the same capacity is not available to European refiners.

More capacity always available – at a price Furthermore, additional capacity can always be accessed by the buyer from certain major (re)insurers, even up to the full theoretical market capacity figure. But especially in 2019, this capacity is only available at a price, often an uneconomic one. We think that it would be misleading for us to advertise additional capacity which in all likelihood will prove to be uneconomic to purchase.

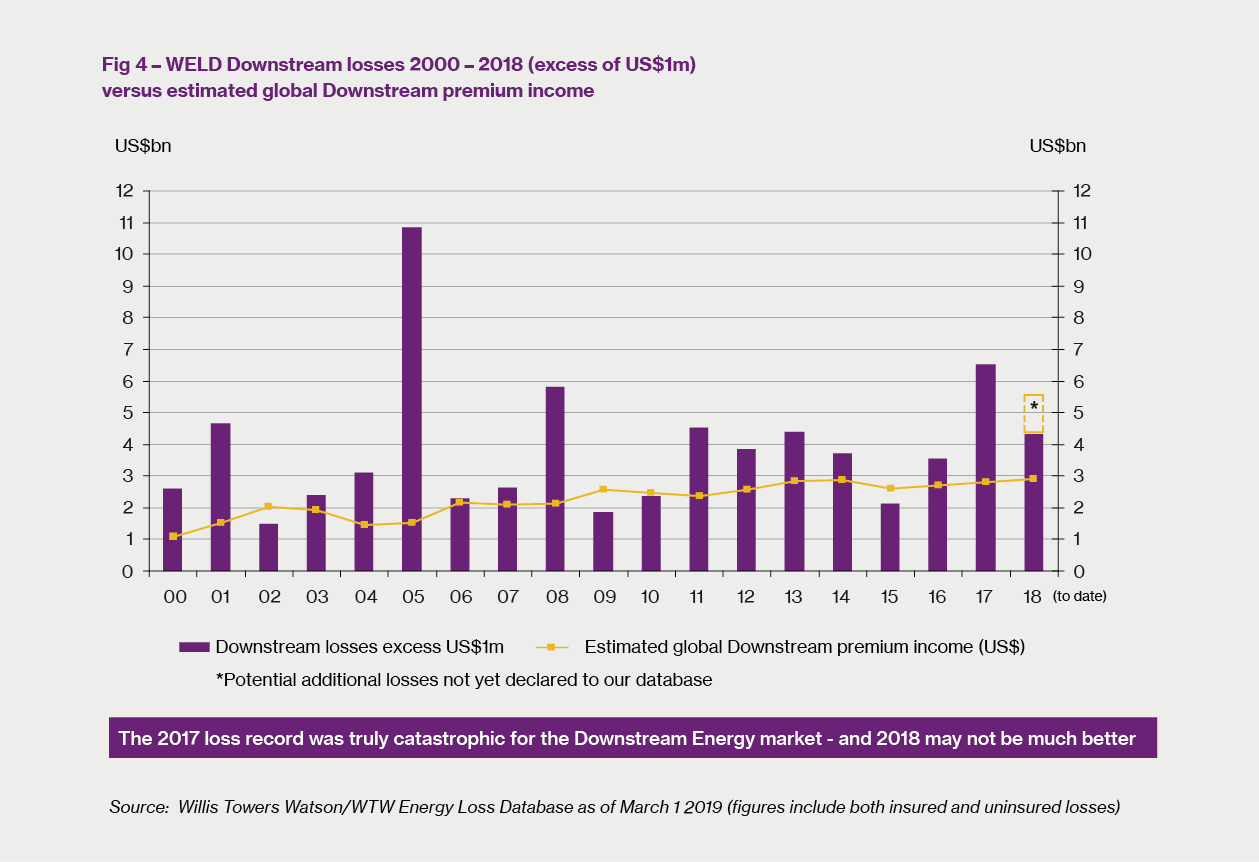

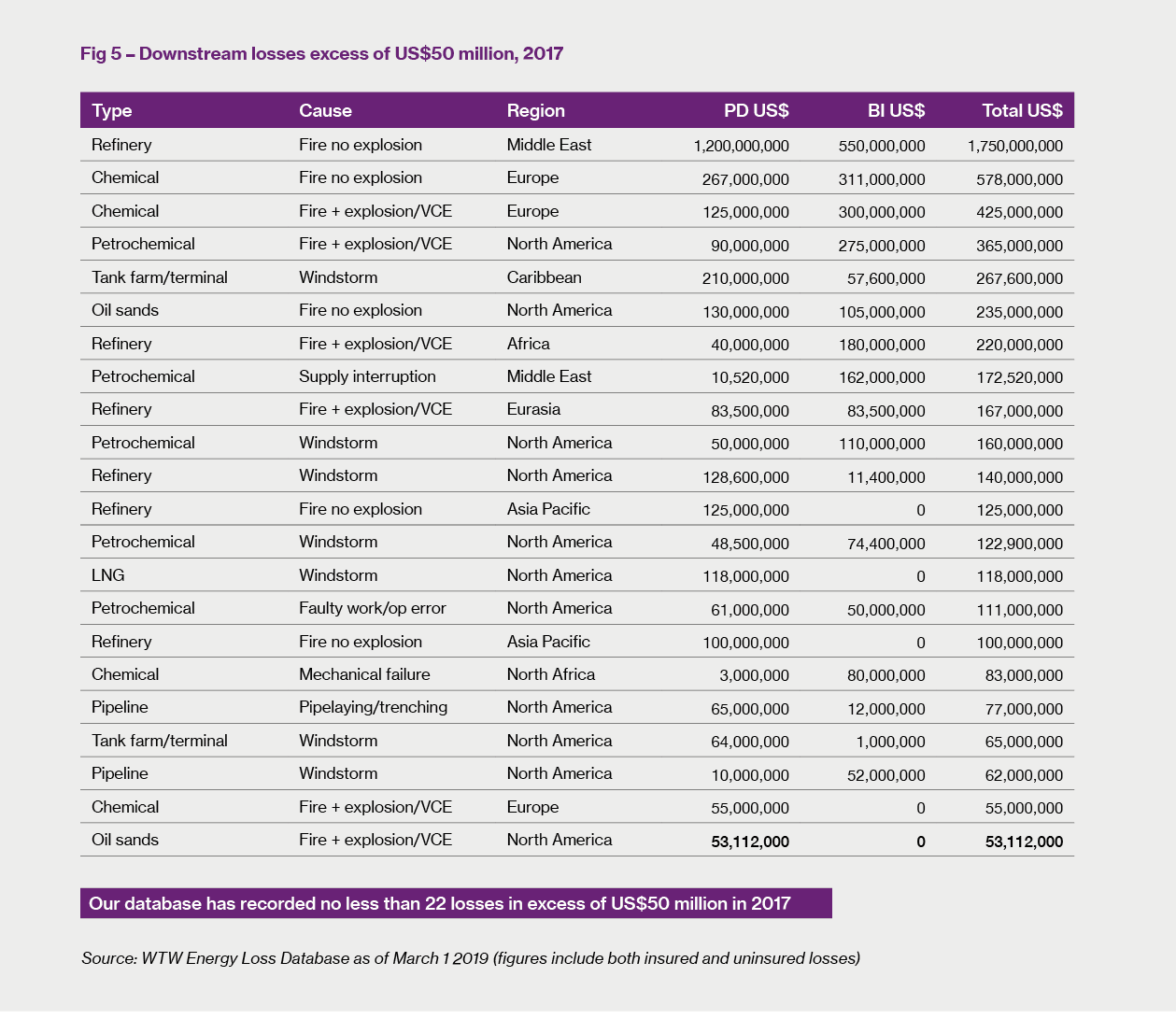

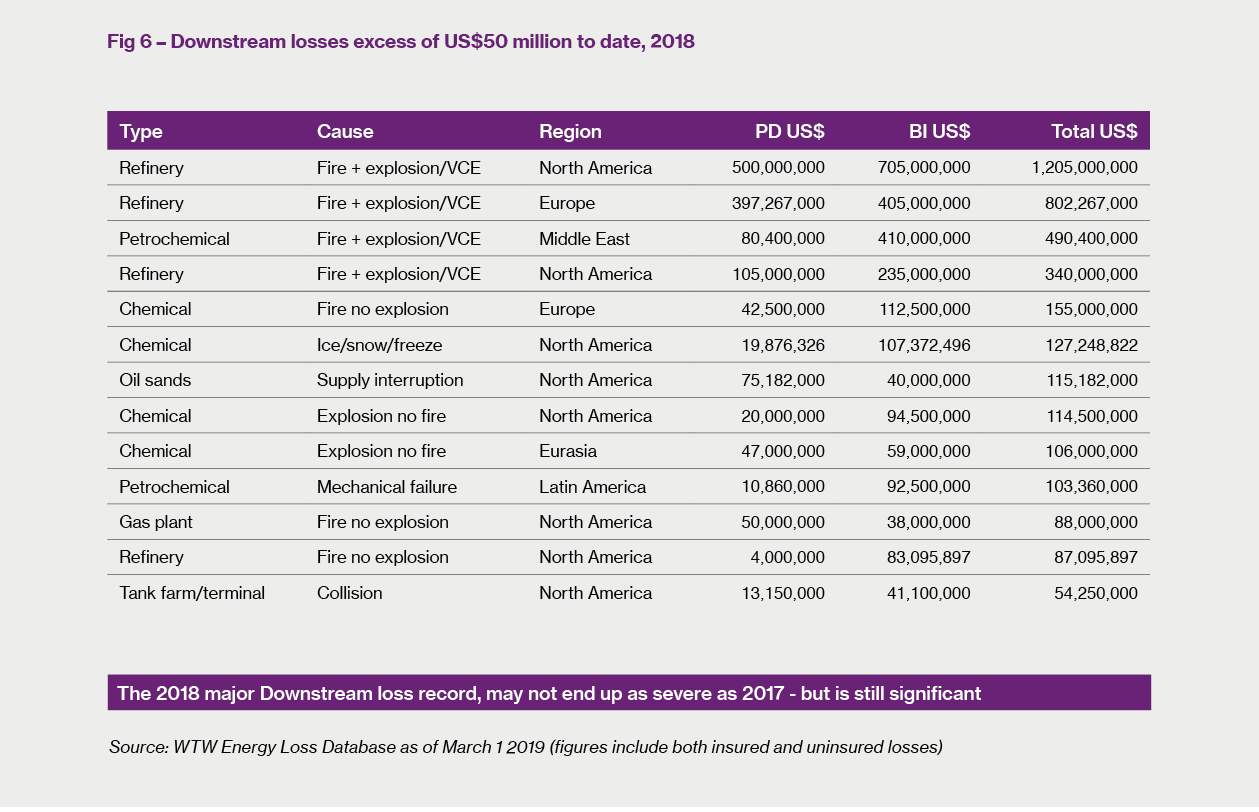

A dreadful 2017 – and 2018 isn’t looking great either As can be seen from Figure 4, the 2017 Downstream loss record has been dreadful – the worst non-hurricane affected year since the turn of the century. It seems that 2018 will be a little better, but not much – at this stage we do not believe that all the losses occurring in 2018 have made their way onto our database, which is why we indicate a contingency for an additional US$1 billion of losses for last year. In any event, the 2018 loss total has already once again exceeded our estimate of the total global premium income for this class.

Figures 5 and 6 outlined on this page and the next show brief descriptions of the major Downstream losses (in excess of US$50 million) for the last two years. Two factors should perhaps be noted: first, the preponderance of North American losses compared to other parts of the world and second, the significant proportion of these losses arising from Business Interruption (BI).

Meanwhile the recent losses reported only a few weeks ago in Darwin, Australia, while likely to fall on the Construction insurance market, will have done nothing to soothe the current Downstream market apprehension.

Regardless of how 2018’s figures will eventually play out, this level of loss activity, when combined with the reduced premium income pool affecting so many lines of business, has generated underwriting losses across the underwriting spectrum. From London to Miami, from New York to Dubai, from Zurich to Singapore the story has been the same – consistent underwriting losses which have brought Downstream portfolios all over the world under increasing scrutiny from regulators and management.

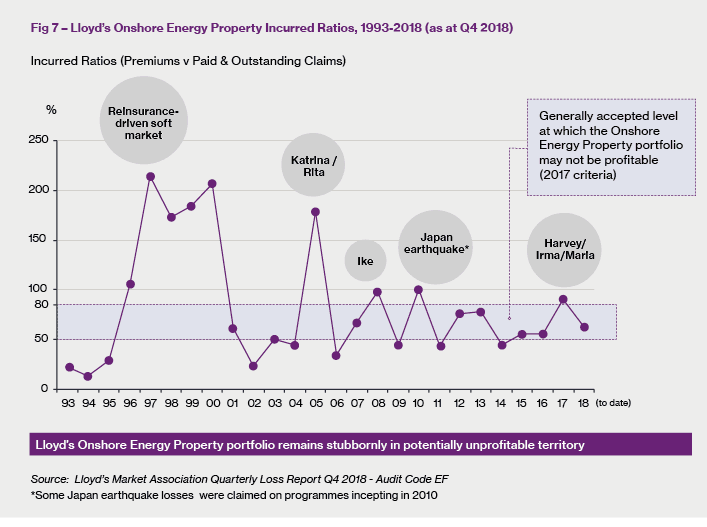

Figure 7 overleaf shows only Lloyd’s figures, but there can be no doubt that the recent Incurred Ratios (premium income versus paid and outstanding losses) displayed in this chart are not only indicative of this class across the board, but may have also been exceeded by insurance company results elsewhere. 2017’s Incurred Ratio of 90+% has now been followed by 2018’s 60%, a figure which also signals another underwriting loss for the Lloyd’s Downstream portfolio.

No wonder underwriters are in an unforgiving mood, worrying about the effect that poor underwriting results for the last three years might have on the long term future of their own portfolios. Rating adequacy is therefore now their overriding priority, with double digit rating increases now the norm.

Management pressures raise the bar Encouraged by the first rating increases that they had ever negotiated towards the end of 2018, insurer management reaction has now been to encourage their underwriters to push for even higher percentage rating increases, as well as scaling back on unprofitable business.

This development has recently led to one extraordinary situation recently where one insurer’s opportunistic renewal price for a primary US$500 million limit was actually in excess of the full quota share price which the previous year’s programme had been placed at. Furthermore, we are seeing a marked willingness from several insurers to walk away from business if their own terms cannot be agreed; in the previous softening era this was generally something that they were very reluctant to do in view of the loss of premium income that this would involve.

Insurers differentiate in favour of quality business Of course, it is simplistic to talk about a simple percentage increase that is now applying across the whole Downstream portfolio. Although in general terms rating increases are at least in double digit territory, there are always exceptions to the rule, especially when it comes to the market’s appetite for well-regarded business.

For example, we recently renewed one major Physical Damange (PD) only programme that had been heavily over-subscribed in the previous year for a smaller percentage increase than the norm, for the simple reason that its over-subscription in 2018 demonstrated that the rating increase could be limited to single digit territory. While the terms offered by the leader were below their underwriting rating threshold, we saw several insurers actively consider this programme for the simple reason that they liked the risk and its associated premium income.

Loss impacted programmes may be in serious trouble On the other hand, we are aware of some loss-impacted programmes that are finding it difficult to secure any interest at all from the market as insurers seek to scale back to their core business. As we mentioned in the Upstream section of this Review, those buyers that had sought out the best price in the previous softening market with scant regard to insurer loyalty are finding today’s market conditions particularly challenging. We understand that in some extreme cases these buyers are having to settle for increases of as much as 100%.

The broker’s challenge – putting it all together In this complicated underwriting environment, with insurers taking increasingly independent lines on rating levels, producing an overall “blended” rate is becoming increasingly challenging for brokers. With all vestige of a subscription market well and truly erased, brokers are having to use all their intelligence and expertise to access a range of different insurers and ensure that a consistent product is finally offered to the buyer.

A return to individual underwriting In summary, within the overall context of increasing rating levels there are a wide variety of possible outcomes to renewal negotiations. One trend that has been particularly noticeable is the re-emergence of underwriting each piece of business on its own merits, rather than applying a broad brush rating outlook to a variety of different risks within the Downstream portfolio.

Selling capacity for premium income? Furthermore, the Downstream market is now much more aware of the value of each dollar of underwriting capacity. Whereas in the past if brokers needed a small increase in line to get a particular programme home they could simply ask for a small increase from each insurer that was already participating in the programme, in 2019 insurers are quick to insist that either they are happy with their existing line or that any additional participation would have to come at a price.

In previous editions of our Review we have often commented on the variation in underwriting approaches taken by the different regional markets participating in the Downstream portfolio. One of the interesting features of this hardening market has been the increasing centralisation of underwriting authority, as individual underwriters around the world respond to the same management diktats that apply globally as well as regionally.

Regional rating anomalies smoothing out As a result, while every generalisation has its exceptions, we are finding that roughly similar terms can be negotiated for a given programme from insurers across the world. Whereas once a major composite insurer could produce radically different terms in say Miami or Dubai compared to London, now we are finding this to be much less the case.

A more centralised market? Indeed in some regions such as the Middle East, we have seen a much more severe centralisation of underwriting authority, as some insurers have recalled their Downstream operations to London while others, such as Qatar Re, have ceased trading altogether. While any withdrawal of underwriting expertise is not yet in evidence in other major Downstream markets such as North America and Singapore, we are still finding that insurers in these markets are now producing terms which are relatively consistent with those offered by their London counterparts.

The major exception to this development is China where, as we reference elsewhere in the Review, the local insurance market continues to build its capability and to challenge the international markets competitively for Chinese business.

BI losses nearly half the total Figure 8 on the previous page shows the proportionate split of Downstream losses reported to our database over the last four years between PD and BI losses. It shows overall insured and uninsured losses, totalling approximately US$15.6 billion, against an estimated global four year premium pool of approximately US$8 billion. It can be seen that BI losses amount to nearly 50% of the total incurred – an alarming proportion of overall losses, given the extent to which BI is insured in the commercial insurance market (the insurance mutual OIL has always excluded BI from its risk transfer product).

Insurers on the hook – with no way out Given the rapid recovery of commodity prices evident during the last three years or so, it’s easy to see why insurers are worried. At present, coverage for BI is provided for a specific indemnity period, typically 36 months, excess of a waiting period, typically 60 days. In the event of a loss, insurers agree to reimburse the buyer for the actual loss sustained up to the time limit stipulated by the policy, regardless of quantum.

Sheer quantum of losses has rocked the market What has alarmed the insurance market in recent years is that the actual losses sustained by the buyers (and successfully claimed under their insurance policies) have often been much greater than may have originally been envisaged, perhaps in part due to the rapid (and possibly unexpected) recent increase in commodity prices. As a result, the sheer quantum of BI losses has come as something of a shock, compounding the gloomy atmosphere in the market and attracting the urgent attention of senior insurer management. The result of the impact of these BI losses is therefore likely to be an even greater pricing upswing than for the PD element of the programme.

The insurers’ solution - Actual Declared Value (ADV)? What might the market consider doing to dilute this upswing? One possible solution would be for future programmes to be placed on an ADV basis. Under an ADV policy, the buyer would calculate the overall annual revenue derived from the asset in question, taking into account the seasonal variations which are an inevitable feature of downstream energy operations. That annual number is then divided by 365 to produce an average daily indemnity amount. A reasonable margin – say 20% - is then applied, providing a reasonable degree of leeway and thereby reducing the possibility of under-insurance on the part of the buyer.

Providing certainty for the insurer… On this basis, the insurer is in a much more confident position - they will know that no matter what the actual indemnity value is at the time of loss, there is a maximum dollar limit in place in the policy which cannot be exceeded. As a result, the insurer will be more confident in providing cover while the buyer would be provided with sufficient BI cover at a reasonable price.

…but uncertainty for the buyer! Of course, this sounds wonderful in theory. But this solution would hardly be welcomed by the buyers. The big disadvantage from their perspective is that if their BI calculations are incorrect, then even a 20% leeway from the erroneous figure would not enable them to be indemnified correctly. It is difficult to suggest that any buyer would voluntarily submit to insuring on an ADV basis – unless they were sufficiently confident that the average BI daily indemnity declared at inception was accurate.

The reality is that a great many buyers, especially those that have not sustained losses recently, are unlikely to have the means or the wherewithal to transform their data collection recording methodology to the degree required to ensure pinpoint accuracy in the event of a loss.

The broker’s solution – better underwriting information from the outset! Like so many aspects of life at the end of this decade, data is increasingly king. Those buyers who have the ability (maybe with the help of their risk advisors or their engineers) to produce state of the art underwriting information, particularly with regard to their BI exposure, are likely to reap the benefit of limiting the current rating upswing, as well as ensuring that they will be properly indemnified in the event of a loss - without the need for punitive solutions such as ADV being imposed on them by the insurance market.

Might there be a knock-on effect on Contingent Business Interuption (CBI)? Be that as it may, given the current market conditions it is clear that pressure will continue to be brought to bear by insurers to reduce sub-limits for critical additional coverages such as CBI. One further advantage of conducting a detailed business interruption analysis as referenced above may therefore be that sufficient data is produced to persuade insurers to maintain existing sub-limits – or even increase them.

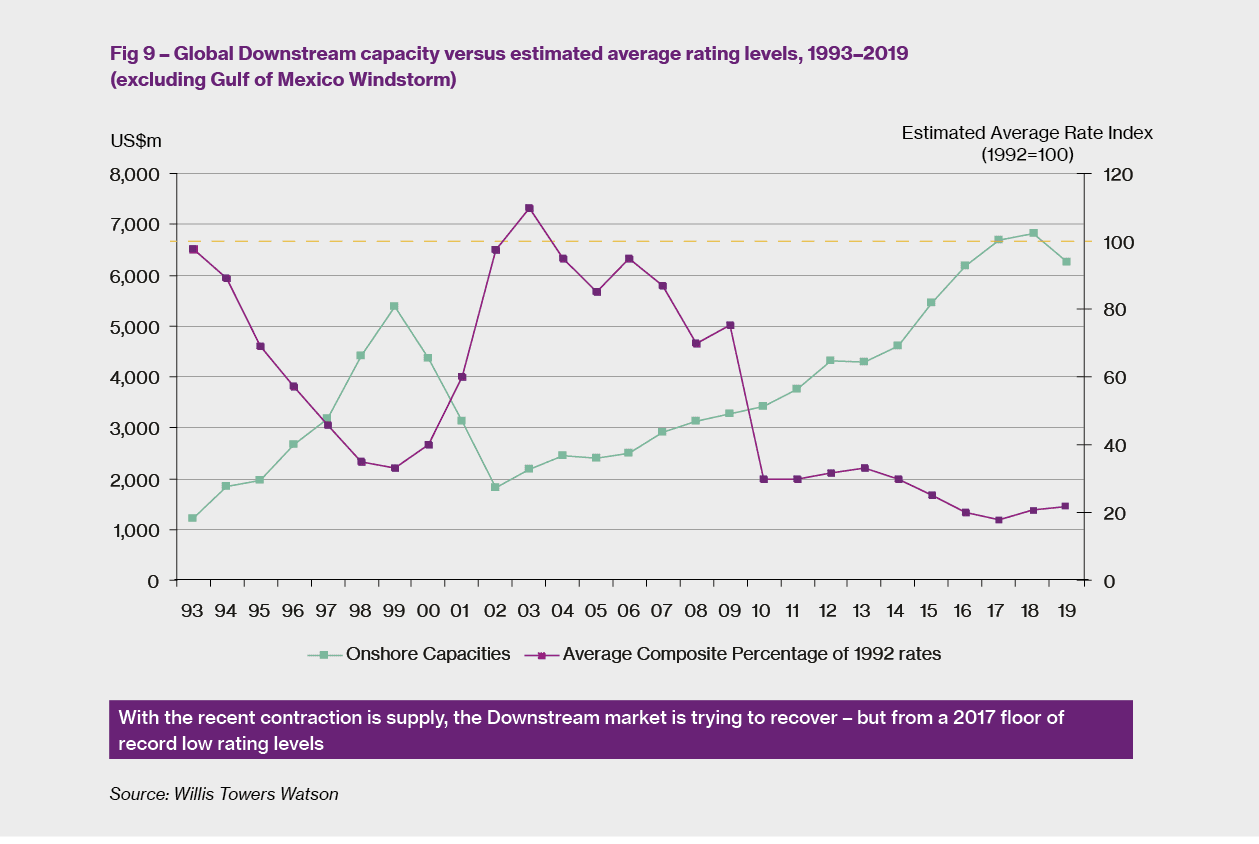

Our final chart (Figure 9) shows the correlation between supply (total theoretical underwriting capacity) and average Downstream market rating levels over a 26 year period. It can be seen that usually prices drop as supply increases, but in by no means a uniform fashion. What is also clear is that the Downstream market is as historically volatile as its Upstream counterpart, although this has smoothed out significantly during the course of this decade as capacity has remorselessly increased year by year. Is this upswing really significant? That is, until now. As we described at the beginning of this chapter, capacity levels are finally declining and rating levels are increasing. As a result, we are seeing a fresh dynamic on this chart – but what will this mean for the buyer?

Perhaps not as much as the insurance market would like to think. Our chart indeed shows that rating levels have increased – but if we read across from 2019 back to 1999, we see that the rates of twenty years ago – a the bottom of what was then considered to be one of the softest insurance markets of all time – were still some 30% higher than they are today. The modest rating increases imposed by the market today may be welcomed by the insurance community, but in the very long term they hardly amount to a significant volte–face in overall insurance market dynamics.

No return to past volatility Our own view is that the recent decline in overall underwriting capacity levels is not set to increase significantly. The Downstream market can still offer at least US$3 billion to most buyers, sometimes more with the help of regional capacity (see Figure 3 earlier). While it is true that the onward softening process of the last 10 years has finally been brought to a close, the Downstream insurance market still offers buyers excellent value for money.

One strategy which may prevent this from being the case in the future would be for buyers to carry on searching for optimum terms without regard for developing better and more detailed underwriting information or developing sound business relationships with key insurers. These insurers will no doubt be hoping that the actions taken to date will enable them to be still standing as we move into 2020. And if they are, then they will still be holding the advantage at this critical stage of the underwriting cycle.

Steve Gillespie is Head of Downstream broking at Willis Towers Watson Natural Resources in London.

1 https://www.willistowerswatson.com/en/insights/2018/11/energy-market-review-november-2018-update-winds-of-change