A gentle market upswing

A gentle acceleration of the hardening dynamicTowards the end of last year we released a supplement to our 2018 Review1 in which we described conditions in the Upstream insurance market as basically flat. We explained that the continued presence of abundant capacity, together with an essentially benign loss record, was being balanced by the drive for underwriting profitability, especially in Lloyd’s, following poor overall underwriting results in other classes. However, nothing stands still for long in the Energy insurance markets and we can now sense a small but noticeable change in the overall underwriting environment in the Upstream sector. Despite all the macro factors – capacity, losses, overall underwriting profitability - still pointing to favourable market conditions, we must instead report that the market has, almost imperceptibly, moved closer towards a harder trading environment for buyers.

Why? Why should this be the case? What has happened during the last few months to enable insurers to tilt the balance of market dynamics further in their favour? How long will this last, and what can buyers do to offset this overall hardening trend?

As ever, let’s start by examining the overall trends and then see how the market has fragmented in recent months to leave a complex landscape for buyers and their brokers to navigate through in 2019.

Another increase…and no withdrawals As many readers will undoubtedly be aware, the history of the Upstream market in the 21st century has been dominated by the extraordinary increase in overall underwriting capacity levels. Since the immediate aftermath of the tragic events of 9/11 – and a minor blip following the hurricanes of 2005 - the market capacity trajectory has been remorselessly upward. Although the rate of increase has tailed off somewhat in recent years, there has been no sign of any decrease in capacity, nor indeed of any significant underwriter withdrawals from this class.

As a result, Figure 2 still shows another record overall capacity level for 2019, with just over US$8 billion now in play. And as we have said many times before in this Review, until more attractive havens for capital materialise, we don’t think that there will be any significant reduction in this figure in the immediate future. Moreover, our maximum realistic capacity figure, which indicates the capacity level that may be available in practice from the market for a given programme, remains at US$6.5 billion as it was for 2018.

But how much of this is truly available? So on the face of it, all seems well from a buyer perspective. However, these overall figures only tell part of the story. First of all, this level of capacity will only be available to the most well-known and trusted buyers with assets in recognised and familiar locations such as the North Sea. Secondly, we are finding that insurers are now under much less pressure to underwrite for premium income and so no longer feel that they have to participate on every programme they are offered; they are therefore deploying their maximum capacity on fewer and fewer occasions. Thirdly, all manner of other underwriting considerations will in reality limit available capacity still further – type of operation, location, claims record, loyalty to exiting leadership and so on. And as we shall see as we explore the different areas of the portfolio in more detail, insurers are taking a different approach to other regions and sub-classes of business.

Favourable loss record enters its third year From a catastrophic loss perspective, there is no doubt that the Upstream market continues to benefit from a remarkable run free of major disasters. Indeed, Figure 3 shows that the last three years have produced only one major disaster of note, being a significant loss offshore West Africa in 2016 that unusually involved a large Loss of Production Income loss. Aside from this, the record has really been extremely favourable from an underwriting perspective; indeed, so far in 2018 our database has only recorded two losses in excess of US$50 million. Even if further losses that have been incurred last year but have yet to find their way onto our database are taken into account, there is very little chance of them making any significant difference to the overall benign scenario.

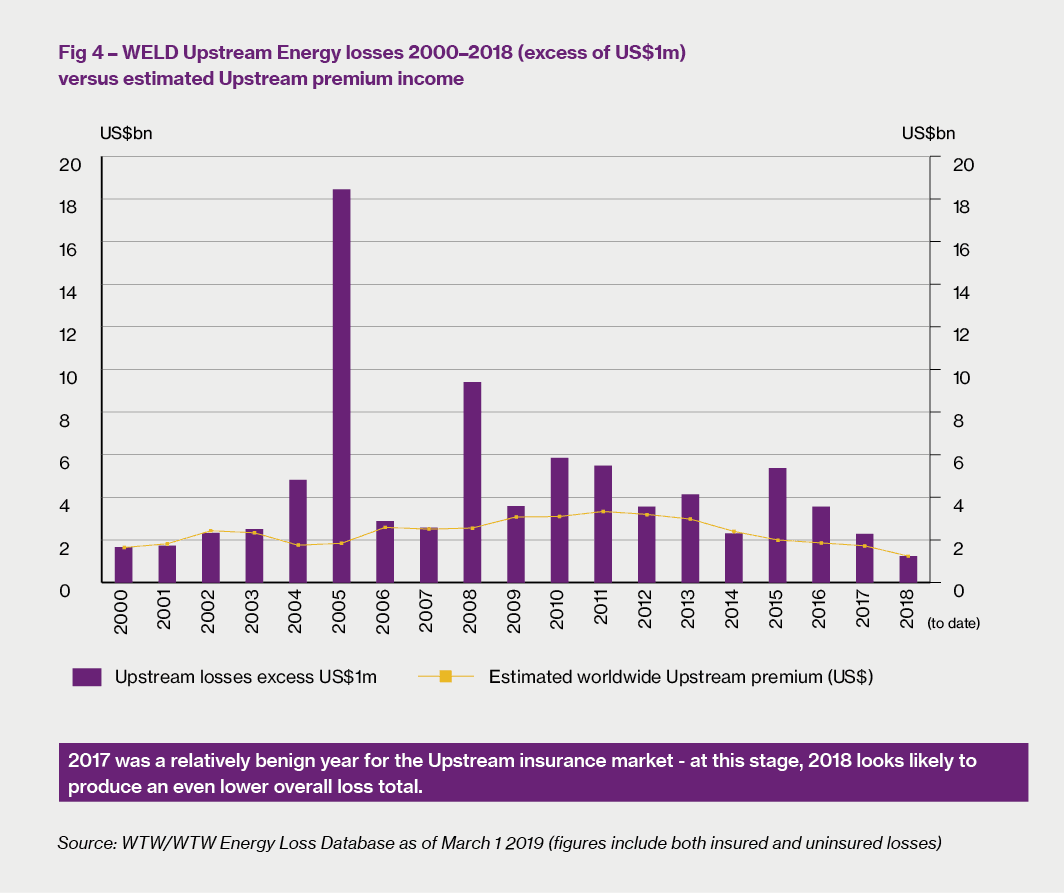

Overall total at record low Furthermore, Figure 4 shows that the benign nature of the recent Upstream market loss record is not just confined to the catastrophe arena. Although we must take into account the potential for our database figures for 2018 to deteriorate further, we can see from this chart that the overall 2018 total excess of US$1 million is currently the lowest we have ever recorded for this class. It really is remarkable to consider that only four years ago our database was recording losses in excess of US$5 billion; to date, we only have just over US$1 billion recorded for 2018. And while the estimated premium pool continues to decline, the fact remains that at present it seems to be still sufficiently robust to keep the overall portfolio profitable. In summary then everything seems to be pointing in the right direction for Upstream insurers. So why are we talking about a gentle hardening in overall rates? Let’s take a look at some of the factors on the other side of our “see-saw”, as outlined in Figure 1 earlier.

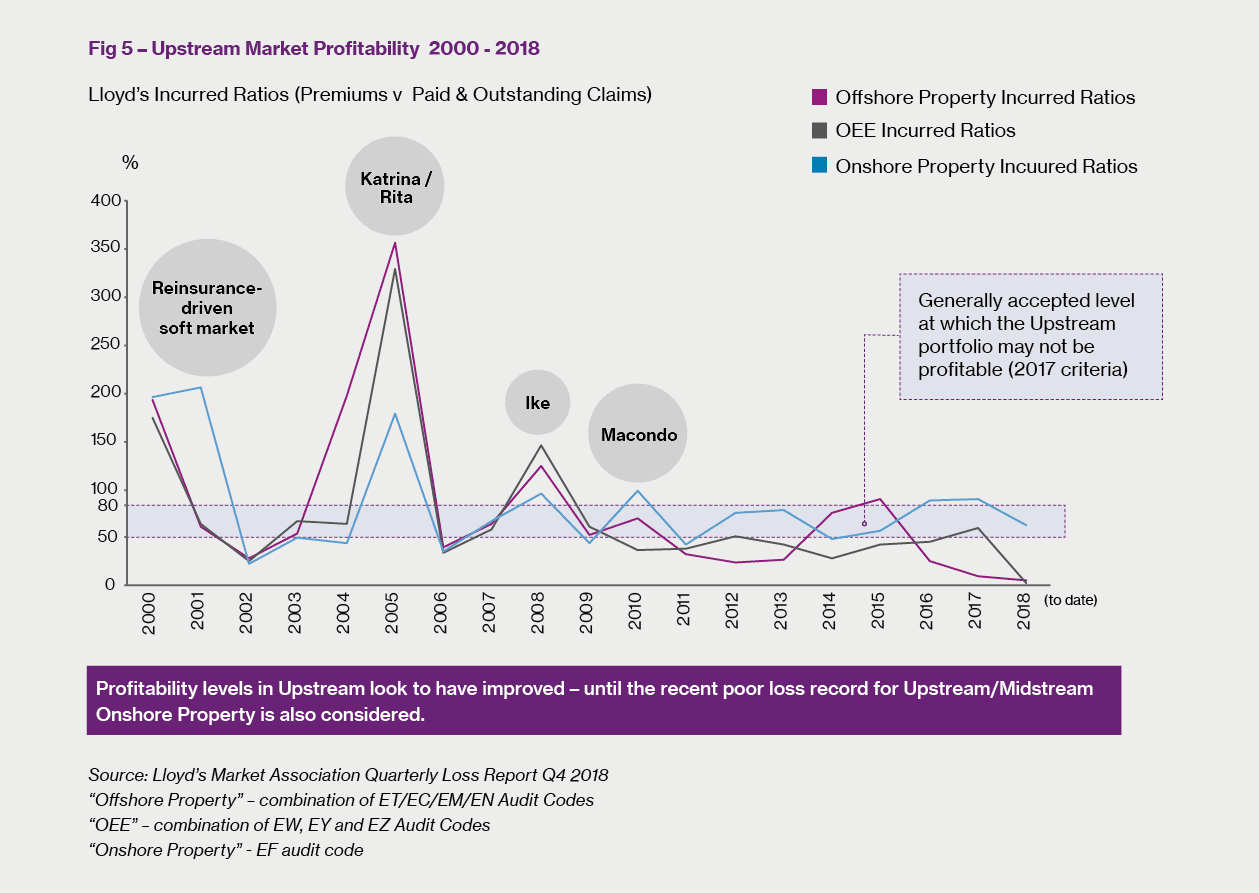

Profitability: positive news impacted by Onshore portfolio and operating costs Figure 5 shows Lloyd’s Incurred Ratios (Premiums Received versus Paid and Outstanding Claims) for the Upstream portfolio over the last 18 years. In order to take into account operating and reinsurance costs, to make a true profit we believe that insurers must generally record Incurred Ratios below 50% to guarantee an underwriting profit, and in any event be at least under 80%. This is why we have shaded the area between 50% and 80% in purple on our chart:

If we look back over the last five years or so (the figures for 2018 are still too immature at this point in time to be germane) we can see that:

So although it is correct that the Upstream portfolio as a whole has been making money from insurers in recent years, it can now be seen that this is by no means the case across the board. Meanwhile, we understand from our conversations in the market that operating costs as a percentage of their overall premium income are continuing to rise; so with so little premium coming into the market (see Figure 4 earlier) it can be seen that securing an overall underwriting profit is perhaps not quite so straight-forward as it might first appear. And all the while, Upstream underwriters continue to feel the scrutiny of their managers and senior Lloyd’s executives, as their business plans come under renewed scrutiny and the pressure to “hold the line” on rating levels intensifies.

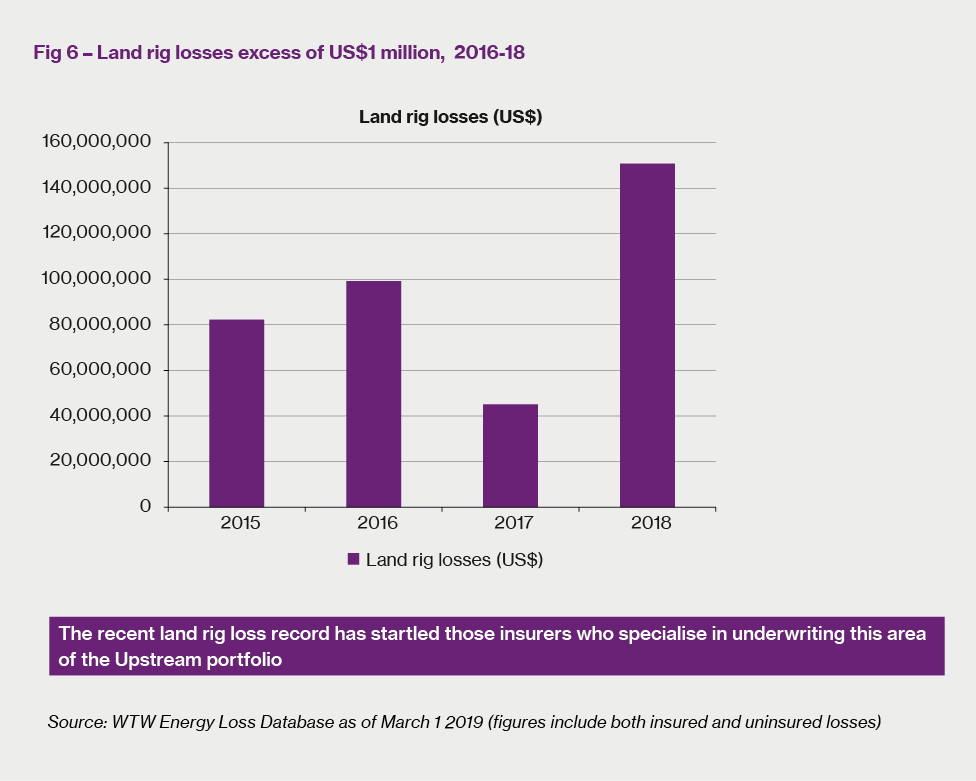

Land rigs: a blot on the Upstream risk landscape In many ways, land rigs are something of an anomaly in the Upstream market. By definition they operate onshore; their values are small by Upstream asset level standards; losses tend to be low level and frequent rather than high level and catastrophic. But they have always been an integral part of the Upstream portfolio and several Upstream leaders have taken a long term view that, written in bulk and under insurer facilities, money can be made over time. However, Figure 6 shows that 2018 has been a particularly bad year for land rig losses, with nearly US$150 million dollars’ worth of losses excess of US$1 million reported to our database to date. It is our understanding that the recent upturn in E&P activity has increased utilisation rates, especially in the US, which may well account for this recent upsurge in loss activity.

Whole Onshore E&P book affected Be that as it may, it is our experience that the Upstream insurers in London that have been impacted by this development have taken a strong position on this particular line of business and are currently imposing more significant rating increases on land rigs and other associated areas of the Upstream portfolio such as Onshore Extra Expense (OEE) and Onshore Pipelines. For such small underwriting limits, it might be thought that other markets around the world might be able to step in and provide London with some competition; however unlike other lines of business London remains pre-eminent in the Upstream arena. Furthermore, we understand that a great deal of the Facultative Reinsurance (Fac R/I) capacity that has supported this portfolio in the past has now withdrawn following these recent losses, and another leader who used to play a major role in this class of business has recently indicated that they will no longer participate in this class without certain minimum premium stipulations. As a result, some brokers have found it difficult to drop existing leaders from their underwriting facilities and replace them with more competitive insurers. As a result, buyers have in the main had little choice other than to accept the rating increases demanded by the leaders. Concentration of underwriting leadership expertise At the same time as the pressure mounts on the Upstream portfolio London continues to dominate this sector; indeed to emphasise the point, in recent months we have seen several major insurers withdraw underwriting resources from cities around the world and redeploy them back to London at the same time as some prominent regional insurers have recently withdrawn from the market.

Furthermore, unlike in previous years we do not detect any appetite from the following market to challenge the existing Upstream leadership or indeed to take advantage of the recent market upturn to compete more vigorously for increased premium income and market share. There is no doubt that the new underwriting climate, prompted by the Lloyd’s Decile 10 initiative2, has encouraged underwriters to take a more conservative line than in the past.

Greater confidence to hold out for rating increases As a result, the established market leaders seem now much more confident in pressing for rating increases across the board, irrespective of risk quality. While there has been some talk in the market about some of the major composite insurers taking a higher leadership profile, to date we have not seen this actually materialising in the form of serious competition to the existing leadership, most of which is based in Lloyd’s.

Chinese market emerges as a major player in region However, the one area of the world where this dynamic generally does not seem to apply is in China, where we have seen the local insurance market recently go from strength to strength, backed by strong reinsurance treaties into the London market. These insurers are restricted by their reinsurance treaties to underwriting Chinese business only; what will be interesting in the future is the extent to which they will continue to rely on international reinsurance protection as capital levels increase and individual insurer self-confidence continues to grow.

It is very difficult to be specific on the extent of the overall rating upswing, but in very general terms we can divide the portfolio into three distinct areas:

Offshore Construction - premium income opportunities but challenges remain Upstream insurers have of course welcomed the recent oil price increases over the last two years or so and in particular the way in which these price increases have triggered a new round of offshore construction projects around the world, bringing much needed premium income. However, the recent influx of new projects has not been without its challenges; the Lloyd’s Incurred Ratio for Offshore Construction has recently nudged 30%3, bringing it worrying close to loss-making levels. Furthermore, the share of this portfolio taken by the commercial insurance market has continued to reduce, as increased captive participations across the various co-venturers has often meant that the only share available to the market has been that of the leading underwriter. As a result, the potential for volatility in this sector of the market has definitely increased, with some leaders offering terms at significantly higher levels than were the norm only a few years ago.

What’s more, a large proportion of the new projects feature significant subsea tiebacks and other underwater assets – technology which has proved to lead to underwriting losses in the past. No wonder some insurers continue to look on this part of the portfolio with a degree of trepidation, and should a major project require the participation of the majority of the Upstream market, the buyers concerned should continue to expect to be offered robust terms, especially given the sector’s recent loss record.

Gulf of Mexico windstorm - a static market, but a loss may change everything Once again, despite an active hurricane season in the Gulf of Mexico, it appears that the sector of the Upstream market that underwrites Gulf of Mexico windstorm (Gulf Wind) has escaped paying any major losses in 2018. As some readers of this Review will recall, coverage and capacity for these risks has been limited by overall aggregate for many years, particularly since the impact of hurricane Ike in 2008. As a result, the same insurers that have written this portfolio for many years continue to do so, while those who have not built up a book of Gulf Wind business continue to avoid it. We could speculate that Upstream insurers are reluctant in this underwriting climate to start writing this book without the benefit of any back year premium to then be immediately faced with the consequences of having to pay for a major loss.

So buyers could expect a relatively stable market in 2019. That being said, should 2019 actually produce a major Gulf Wind loss, we think buyers can expect an interesting market dynamic as the existing market finds its efforts to impose rating increases in the wake of the loss limited by the arrival of fresh competition from other parts of the Upstream market. We would anticipate that several insurers who do not currently participate in Gulf Wind programmes may be keen to take advantage of the loss and the opportunity of taking a share of the resulting premium increases. That being said, Gulf Wind protection remains a notoriously volatile product and predicting the extent of any change in rating levels in the aftermath of a major loss is by no means an easy task.

Cyber – two into one won’t go! The Upstream insurance market’s attempt to formulate a market-wide, effective risk transfer vehicle for cyber risk continues, albeit at a pace that perhaps some buyers are finding somewhat frustrating. As this Review went to press, a new cyber policy wording was being reviewed by the London Joint Rig Committee, although we understand that progress to date has been slow. The root of the challenge is in finding a way to combine Berkley/AXA XL’s CABBE policy form, which is designed for a single targeted insured event and provides a limit up to the single largest scheduled asset, with other market products from insurers such as QBE, Munich Re and Brit, which provide cover for a multiple Insured cyber-attack with a sub-limit. The difficulty is that so many insurers have different agendas when it comes to cyber risk; some have invested a great deal of time and money in employing specialists to underwrite their portfolio, and quite understandably do not wish to see years of investment be compromised by a composite product which does not reflect their own outlook.

Meanwhile some buyers have had little option but to purchase the limited amount of cover on offer – particularly those energy companies who are members of Oil Insurance Limited (OIL) who require the knowledge that their excess of OIL “wraparound” cover includes some form of cyber protection, given that the OIL form is silent on this issue.

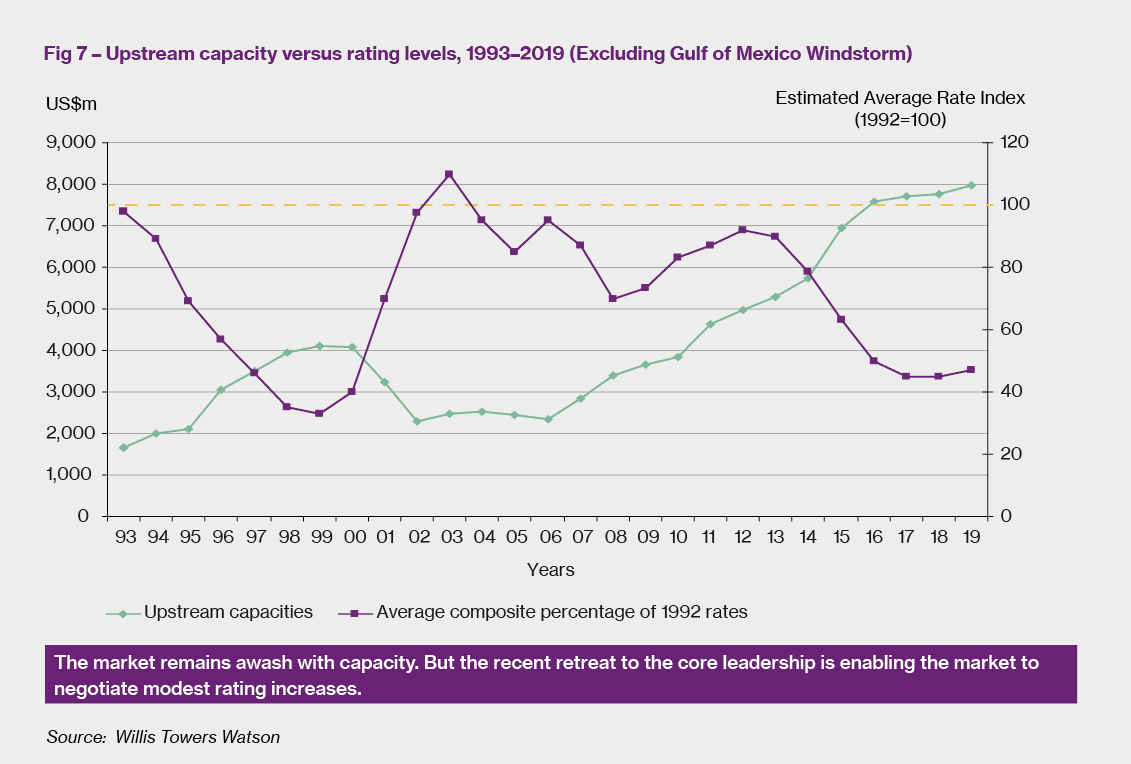

So what can buyers expect from the Upstream market as we head further into 2019? Our chart outlined in Figure 7 shows the correlation (or sometime lack of correlation) between official underwriting capacity and average rating levels over 26 years since we began keeping the data. In very general terms it shows that as underwriting capacity has significantly increased since 2006 to its present record high, prices have generally reduced, following the economic laws of supply and demand.

The return of the “false equilibrium” But now, once again as in the period 2008-14, we are seeing the recurrence of the phenomenon known as the “false equilibrium” – increasing prices at a time of increasing underwriting capacity. Having flattened out in 2017, the gentle market hardening is defying the laws of gravity once more. The last time this occurred was when a series of underwriting losses, beginning with hurricane Ike in 2008 and continuing during the next few years with major losses such as the Deepwater Horizon tragedy in 2010 and the Gryphon A loss in 2011, coincided with a period of a limited number of Upstream leaders. Now we are seeing the same thing again, but this time the pretext is more general – the new underwriting mood in London has been prompted by the need for underwriting discipline across the board as the Lloyd’s Decile 10 initiative makes its impact felt across Upstream just as much as any other line of business. With leading underwriters under such public scrutiny, and with realistic alternatives few and far between, it is hardly surprising that a combination of insurer management and the Lloyd’s PMD has been able to prevent any rating reductions being applied to almost every programme4. Of course there are exceptions and there is no doubt that by restructuring programmes and by persuading insurers to take into account additional premium income coming into the market, there will be some programmes that will defy the market norm. But in our view they will be few and far between.

Not yet a truly hard market Having said that, in our opinion this is still not a truly hard market. Bearing in mind today’s capacity levels, we are a long way from a scenario whereby a buyer and its broker have to shop around for cover at differing terms. And from our chart it should be clear that the current modest upswing in rating levels still only brings the market back to where we were three years ago, where rates were as low as they had been for the past 16 years or so.

How should buyers best navigate what is a complex Upstream market environment? There is no doubt that striking the optimum deal with a resolute market in 2019 will present an interesting challenge, whether a buyer’s programme is regarded comparatively favourably by the market or whether it is negatively impacted by a poor claims record or risk profile. For most buyers, the choice will come down to a simple decision. Those who enjoy casinos will be familiar with the options available to the blackjack player – to stick or to twist. A similar dilemma awaits risk managers who want to be delivered with optimum terms.

Twist – but will this pay off in the long term? The first option is to “twist.” Often the choice for so many buyers, particularly National Oil Companies (NOCs) that need to externally validate that they have chosen the most competitive approach, this involves continuing to tender their programme on a regular basis to defy attempts by the market to insist on rate rises. In a softening market, this is often a wise choice as there are plenty of willing alternatives ready to augment their premium income stream with fresh business. However, in this underwriting climate this approach may not produce the results promised by the tender process. And if the programme subsequently fails or is subject to a major loss, the potential for a significant rating upswing is very tangible.

Stick – but will loyalty be rewarded? The second is less exciting on the face of it, and that is to “stick”. Those buyers who have forged long term relationships with leading insurers whom they regard as key strategic risk partners may take the view that they would prefer to stick with the insurers that know them best and whom they view as bona fide stakeholders in their business. In these circumstances, they believe that their relationships will protect them in the event of a major market upswing and capacity withdrawal. Of course, should this not materialise then it might be possible to argue that such an approach prevents these conservative buyers from securing optimum terms.

Which approach will prove to be right? Of course, that will depend on a myriad of factors. But one thing’s for certain – navigating this unusual market environment will not be easy. Given this market’s inherent volatility, it remains very finely balanced, and it would not take a significant derterioration of the loss record to instigate a much more pronounced rating upswing.

With the market as a whole fracturing into different segments, and taking different views on different sectors of the portfolio, buyers are going to need all the help they can get to maximise their position as insurers’ resolve is put to the test later in the year.

Richard Burge is Head of Broking for Upstream at Willis Towers Watson in London.

1 https://www.willistowerswatson.com/en/insights/2018/11/energy-market-review-november-2018-update-winds-of-change 2 https://www.lloyds.com/market-resources/market-communications/market-bulletins/market-bulletins (Y5232) 3 Source: Lloyd’s Market Association Quarterly Loss Report Q4 2018 EC Audit Code 4 https://www.lloyds.com/market-resources/market-communications/market-bulletins/market-bulletins (Y5232)